多国经济严重停滞,全面经济衰退即将来临?

在过去十年里,多年来的低息借款推动了美国投机性投资和无利可图的商业模式的兴起,顽固的通货膨胀迫使美联储在2022年以前所未有的速度大举加息。如今,在这个借贷成本上升、放贷机构更加谨慎的新时代——再加上经济增长放缓和对经济衰退的担忧——美国经济中曾经炙手可热的细分领域出现冻结。

首次公开募股(IPO)市场基本上已经关闭;科技公司正在裁员并暂停招聘;房地产市场在经历了多年的迅猛增长后正在经历“重置”;随着私募市场估值暴跌,风险投资领域已大幅放缓。

不过,尽管关键领域出现了冻结,而且华尔街一直在预测末日的到来,但随着劳动力市场的恢复,整体经济仍在继续增长。去年第四季度,美国国内生产总值(GDP)年增长率为2.9%,超过了分析师的预期。12月,失业率降至3.5%,接近疫情前的低点。

然而,许多经济学家预测,这种情况今年将发生变化。摩根士丹利(Morgan Stanley)首席经济学家埃伦·森特纳(Ellen Zentner)本周表示,第一季度美国国内生产总值年增长率将降至0.2%,富国银行(Wells Fargo)则预计美国国内生产总值年增长率将降至0.4%。一些首席执行官、亿万富翁投资者和投资银行认为,全面经济衰退即将到来。

目前还不清楚,在利率上升的重压下,关键领域冻结是最终会走向破裂——引发经济衰退——还是会从深度冻结状态解冻——实现缓慢的正增长。但信贷市场可能会给出答案。

财富管理公司Wealth Enhancement Group的首席投资和业务发展官吉姆•卡恩(Jim Cahn)在接受《财富》杂志采访时表示:“当信贷市场出现回撤,你无法为交易或投资获得融资时,就是经济陷入冻结状态的时候。信贷作为秘密武器,可以推动经济增长。自400年前工业革命初期信贷市场形成以来,它一直是经济增长的动力。”

经济中正在冻结和已经冻结的细分领域

新时代的高利率、通货膨胀和对经济衰退的担忧,导致美国经济各领域在过去一年里急剧放缓。

风险投资

例如,风险投资领域,在整个疫情期间实现强劲发展。2021年,全球风险投资筹资量达到创纪录的6810亿美元,是2019年的两倍多。

PitchBook分析师亚历克斯·沃菲尔(Alex Warfel)在上周五的一份说明中解释说:“2020年和2021年,廉价资本助长了不惜一切代价追求增长的心态,害怕错失良机(FOMO)也造成投资者兴趣激增,导致人们大规模投资处于各个融资阶段的初创公司。”

但根据Crunchbase的数据,2022年,随着利率上升,风险投资下降了35%,至4450亿美元。沃菲尔表示,“初创公司能够获得天价估值和有利融资机会”的日子已经一去不复返了,风险投资领域的情绪已经“崩溃”,资本已经枯竭。在他看来,根据PitchBook的数据,第四季度,美国初创公司所需的资金估计超过了已提供的428亿美元。

专注于金融科技的风险投资和私募股权公司Fin Capital的创始人洛根•阿林(Logan Allin)在接受《财富》杂志采访时表示,他认为风险投资领域要到2024年才能完全复苏,部分原因是信贷紧缩。他认为对于科技初创公司来说,2023年可能是极具挑战性的一年。

他说:“我们的观点是,2023年将继续是极度痛苦的一年,实际上从科技领域的私募市场和公共股权的角度来看,2023年将比2022年更痛苦。”

阿林补充说,市场的急剧下滑应该给那些在疫情期间养成不负责任的习惯、未能对投资进行适当尽职调查的风险投资人“敲响了警钟”。他举了现已倒闭的加密货币交易所FTX的例子,萨姆·班克曼-弗里德对尽职调查“不予理会”,是因为他们无法通过根据基本的“检查清单”进行的尽职调查,他们还不允许独立审计员查看他们的财务状况。但其他风险投资家甚至没有查看他们的账目就向该公司投资了数百万美元。

他说:“他们要求提供财务数据,而FTX的团队却给他们发送Excel电子表格。这实在是太荒谬了。”

但现在,随着利率上升和许多规模较小的风投公司退出市场,阿林认为市场将回归到更为严格的投资方式。

他说:“我认为风险投资环境将变得更健康、更可持续,因为我们投资的估值和市盈率更合理,能够让公司以更好的方式实现估值并获得利润。这是真正的回归基本面的过程,并重新聚焦尽职调查。”

首次公开募股

当美国的利率接近零,消费者在疫情期间从刺激计划中获得大量现金时,首次公开募股市场经历了与风险投资领域类似的激增。

仅在2021年,美国就有创纪录的1033家新上市公司。但根据安永的《2022年全球首次公开募股市场趋势报告》,在利率上升、标准普尔500指数下跌约20%的情况下,2022年的首次公开募股数量减少了50%。在美洲,这种下降更为明显,去年首次公开募股数量较2021年下降了86%,同期总融资额下降了96%。

“整个2022年,交易活动和交易量急剧下降。首次公开募股市场完全关闭。”阿林说。“公共市场对任何公司都毫无兴趣,即使是那些可能盈利的公司。”

阿林说,他认为今年“首次公开募股市场”只有“一线机会”,而且只有那些能够证明自己赚钱能力的公司才有机会上市。

他说:“否则,这些公司的估值将大幅下降,就像去年或2021年上市的任何一家公司一样。我们仍然面临通货膨胀、高利率、地缘政治不确定性和巨大的波动性,无法为首次公开募股创造一个温暖的市场环境。”

房地产

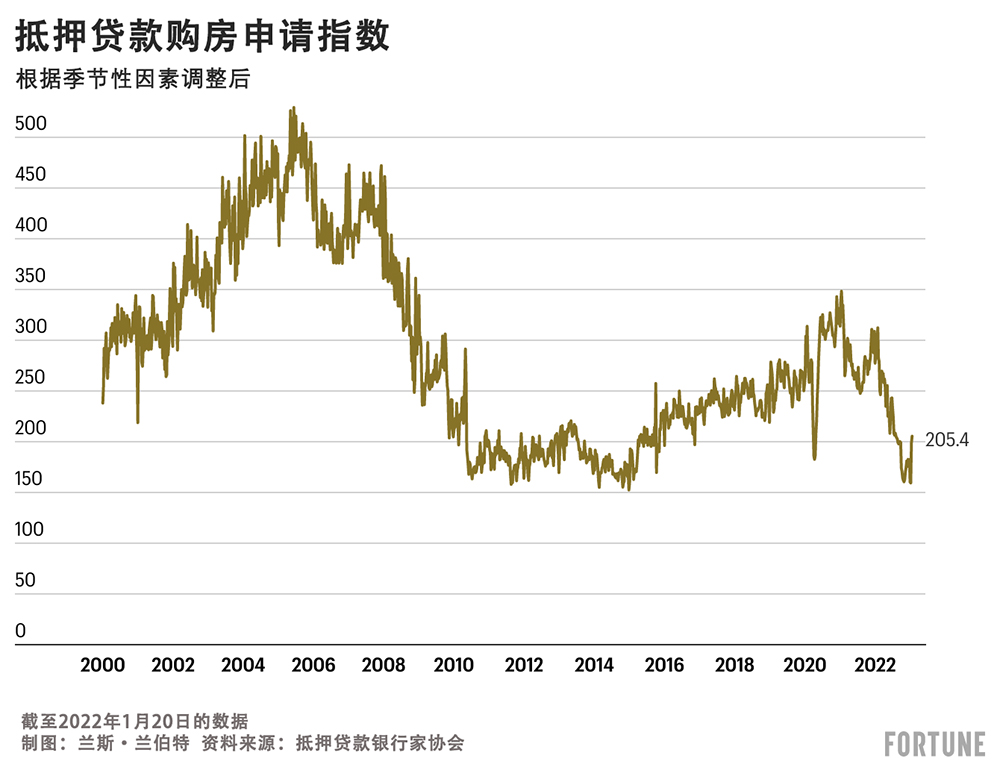

由于低利率和居家办公趋势推动了房地产市场的繁荣,从2020年第二季度到去年第三季度,美国房价飙升了45%以上。但利率上升已将30年期固定抵押贷款利率(美国最常见的抵押贷款类型)从2020年2月的3.45%推高至今天的6.1%出头。

更高的借贷成本和高房价导致负担能力下降,房地产市场出现重大“重置”。上周,抵押贷款购房申请较上年同期下降39%。

投资管理公司Infrastructure Capital Advisors创始人兼首席执行官杰伊•哈特菲尔德(Jay Hatfield)表示,不仅仅是潜在的房主被拒之门外,机构房地产投资者也感受到了利率上升带来的痛苦。他在接受《财富》杂志采访时表示,高利率和对经济衰退的担忧导致银行贷款“枯竭”,这使得收购新房产和/或房地产行业的公司面临严峻挑战。

他说:“现在有一小部分私人贷款仍在进行,但贷款条件太苛刻了,无法再进行杠杆收购(LBO)。杠杆收购指的是一家公司试图用借来的钱收购另一家公司。还有像黑石集团(Blackstone)这样曾是买家的公司。他们现在更可能成为卖家而不是买家。因此,并购活动已经终结了。”

Wealth Enhancement Group的卡恩说,放贷机构不仅提出了更高的利率,而且他们在放贷前也进行了更多的核保——或者说研究和风险评估——以避免违约风险。他指出,这是另一个例子,表明目前某些经济领域的冻结完全是对“信贷市场状况的反映”。

他强调说:“在2021年以及18个月之前,人们以最快的速度地向任何领域大肆投资,因为现金太多了,但在2022年,信贷市场基本上冻结了。这就是为什么你会看到这些行业陷入冻结状态。”

冻结的经济即将崩溃?

经济会慢慢解冻并避免衰退,还是利率上升和高通胀造成的裂缝即将破裂?这取决于你问谁。

卡恩说,他的“预感”是,我们将在“2023年下半年的某个时候”陷入经济衰退。“我认为也许要到2024年,我们才能恢复正常。”他说。

他并不是唯一一个对前景持悲观态度的人。许多顶级投资银行预测,今年将出现“温和的经济衰退”,一些预测者认为,“严重的经济衰退”甚至“另一种类型的大萧条”可能即将到来。

“从经济和宏观角度来看,我们肯定会进入一个越来越艰难的时期,那可能是大写‘R’型衰退或小写‘R’型衰退,但无论是哪种衰退,情况都会很糟糕。”阿林说。

虽然许多专家认为经济衰退即将到来,但也有人认为,这次衰退不会像过去的经济衰退那样具有毁灭性,到2023年底和2024年,冻结的经济领域将开始解冻。Infrastructure Capital Advisors的哈特菲尔德表示,到今年下半年,“首次公开募股市场将恢复正常状态,并购和股市也将复苏。”

他认为,“后疫情的顺风”使劳动力市场保持健康状态——特别是服务行业,在疫情期间,许多企业难以招聘到员工——如果没有大规模裁员使得消费者支出大幅下滑,经济不太可能出现严重衰退。他还指出,尽管去年利率飙升,但住房库存接近历史最低点,他认为这将使房地产领域全年都实现解冻。

他表示:“不过,我们需要美联储暂停[加息],美国的国内生产总值可能会出现一两个季度的负增长,但不会陷入严重的经济衰退。”(财富中文网)

译者:中慧言-王芳

在过去十年里,多年来的低息借款推动了美国投机性投资和无利可图的商业模式的兴起,顽固的通货膨胀迫使美联储在2022年以前所未有的速度大举加息。如今,在这个借贷成本上升、放贷机构更加谨慎的新时代——再加上经济增长放缓和对经济衰退的担忧——美国经济中曾经炙手可热的细分领域出现冻结。

首次公开募股(IPO)市场基本上已经关闭;科技公司正在裁员并暂停招聘;房地产市场在经历了多年的迅猛增长后正在经历“重置”;随着私募市场估值暴跌,风险投资领域已大幅放缓。

不过,尽管关键领域出现了冻结,而且华尔街一直在预测末日的到来,但随着劳动力市场的恢复,整体经济仍在继续增长。去年第四季度,美国国内生产总值(GDP)年增长率为2.9%,超过了分析师的预期。12月,失业率降至3.5%,接近疫情前的低点。

然而,许多经济学家预测,这种情况今年将发生变化。摩根士丹利(Morgan Stanley)首席经济学家埃伦·森特纳(Ellen Zentner)本周表示,第一季度美国国内生产总值年增长率将降至0.2%,富国银行(Wells Fargo)则预计美国国内生产总值年增长率将降至0.4%。一些首席执行官、亿万富翁投资者和投资银行认为,全面经济衰退即将到来。

目前还不清楚,在利率上升的重压下,关键领域冻结是最终会走向破裂——引发经济衰退——还是会从深度冻结状态解冻——实现缓慢的正增长。但信贷市场可能会给出答案。

财富管理公司Wealth Enhancement Group的首席投资和业务发展官吉姆•卡恩(Jim Cahn)在接受《财富》杂志采访时表示:“当信贷市场出现回撤,你无法为交易或投资获得融资时,就是经济陷入冻结状态的时候。信贷作为秘密武器,可以推动经济增长。自400年前工业革命初期信贷市场形成以来,它一直是经济增长的动力。”

经济中正在冻结和已经冻结的细分领域

新时代的高利率、通货膨胀和对经济衰退的担忧,导致美国经济各领域在过去一年里急剧放缓。

风险投资

例如,风险投资领域,在整个疫情期间实现强劲发展。2021年,全球风险投资筹资量达到创纪录的6810亿美元,是2019年的两倍多。

PitchBook分析师亚历克斯·沃菲尔(Alex Warfel)在上周五的一份说明中解释说:“2020年和2021年,廉价资本助长了不惜一切代价追求增长的心态,害怕错失良机(FOMO)也造成投资者兴趣激增,导致人们大规模投资处于各个融资阶段的初创公司。”

但根据Crunchbase的数据,2022年,随着利率上升,风险投资下降了35%,至4450亿美元。沃菲尔表示,“初创公司能够获得天价估值和有利融资机会”的日子已经一去不复返了,风险投资领域的情绪已经“崩溃”,资本已经枯竭。在他看来,根据PitchBook的数据,第四季度,美国初创公司所需的资金估计超过了已提供的428亿美元。

专注于金融科技的风险投资和私募股权公司Fin Capital的创始人洛根•阿林(Logan Allin)在接受《财富》杂志采访时表示,他认为风险投资领域要到2024年才能完全复苏,部分原因是信贷紧缩。他认为对于科技初创公司来说,2023年可能是极具挑战性的一年。

他说:“我们的观点是,2023年将继续是极度痛苦的一年,实际上从科技领域的私募市场和公共股权的角度来看,2023年将比2022年更痛苦。”

阿林补充说,市场的急剧下滑应该给那些在疫情期间养成不负责任的习惯、未能对投资进行适当尽职调查的风险投资人“敲响了警钟”。他举了现已倒闭的加密货币交易所FTX的例子,萨姆·班克曼-弗里德对尽职调查“不予理会”,是因为他们无法通过根据基本的“检查清单”进行的尽职调查,他们还不允许独立审计员查看他们的财务状况。但其他风险投资家甚至没有查看他们的账目就向该公司投资了数百万美元。

他说:“他们要求提供财务数据,而FTX的团队却给他们发送Excel电子表格。这实在是太荒谬了。”

但现在,随着利率上升和许多规模较小的风投公司退出市场,阿林认为市场将回归到更为严格的投资方式。

他说:“我认为风险投资环境将变得更健康、更可持续,因为我们投资的估值和市盈率更合理,能够让公司以更好的方式实现估值并获得利润。这是真正的回归基本面的过程,并重新聚焦尽职调查。”

首次公开募股

当美国的利率接近零,消费者在疫情期间从刺激计划中获得大量现金时,首次公开募股市场经历了与风险投资领域类似的激增。

仅在2021年,美国就有创纪录的1033家新上市公司。但根据安永的《2022年全球首次公开募股市场趋势报告》,在利率上升、标准普尔500指数下跌约20%的情况下,2022年的首次公开募股数量减少了50%。在美洲,这种下降更为明显,去年首次公开募股数量较2021年下降了86%,同期总融资额下降了96%。

“整个2022年,交易活动和交易量急剧下降。首次公开募股市场完全关闭。”阿林说。“公共市场对任何公司都毫无兴趣,即使是那些可能盈利的公司。”

阿林说,他认为今年“首次公开募股市场”只有“一线机会”,而且只有那些能够证明自己赚钱能力的公司才有机会上市。

他说:“否则,这些公司的估值将大幅下降,就像去年或2021年上市的任何一家公司一样。我们仍然面临通货膨胀、高利率、地缘政治不确定性和巨大的波动性,无法为首次公开募股创造一个温暖的市场环境。”

房地产

由于低利率和居家办公趋势推动了房地产市场的繁荣,从2020年第二季度到去年第三季度,美国房价飙升了45%以上。但利率上升已将30年期固定抵押贷款利率(美国最常见的抵押贷款类型)从2020年2月的3.45%推高至今天的6.1%出头。

更高的借贷成本和高房价导致负担能力下降,房地产市场出现重大“重置”。上周,抵押贷款购房申请较上年同期下降39%。

投资管理公司Infrastructure Capital Advisors创始人兼首席执行官杰伊•哈特菲尔德(Jay Hatfield)表示,不仅仅是潜在的房主被拒之门外,机构房地产投资者也感受到了利率上升带来的痛苦。他在接受《财富》杂志采访时表示,高利率和对经济衰退的担忧导致银行贷款“枯竭”,这使得收购新房产和/或房地产行业的公司面临严峻挑战。

他说:“现在有一小部分私人贷款仍在进行,但贷款条件太苛刻了,无法再进行杠杆收购(LBO)。杠杆收购指的是一家公司试图用借来的钱收购另一家公司。还有像黑石集团(Blackstone)这样曾是买家的公司。他们现在更可能成为卖家而不是买家。因此,并购活动已经终结了。”

Wealth Enhancement Group的卡恩说,放贷机构不仅提出了更高的利率,而且他们在放贷前也进行了更多的核保——或者说研究和风险评估——以避免违约风险。他指出,这是另一个例子,表明目前某些经济领域的冻结完全是对“信贷市场状况的反映”。

他强调说:“在2021年以及18个月之前,人们以最快的速度地向任何领域大肆投资,因为现金太多了,但在2022年,信贷市场基本上冻结了。这就是为什么你会看到这些行业陷入冻结状态。”

冻结的经济即将崩溃?

经济会慢慢解冻并避免衰退,还是利率上升和高通胀造成的裂缝即将破裂?这取决于你问谁。

卡恩说,他的“预感”是,我们将在“2023年下半年的某个时候”陷入经济衰退。“我认为也许要到2024年,我们才能恢复正常。”他说。

他并不是唯一一个对前景持悲观态度的人。许多顶级投资银行预测,今年将出现“温和的经济衰退”,一些预测者认为,“严重的经济衰退”甚至“另一种类型的大萧条”可能即将到来。

“从经济和宏观角度来看,我们肯定会进入一个越来越艰难的时期,那可能是大写‘R’型衰退或小写‘R’型衰退,但无论是哪种衰退,情况都会很糟糕。”阿林说。

虽然许多专家认为经济衰退即将到来,但也有人认为,这次衰退不会像过去的经济衰退那样具有毁灭性,到2023年底和2024年,冻结的经济领域将开始解冻。Infrastructure Capital Advisors的哈特菲尔德表示,到今年下半年,“首次公开募股市场将恢复正常状态,并购和股市也将复苏。”

他认为,“后疫情的顺风”使劳动力市场保持健康状态——特别是服务行业,在疫情期间,许多企业难以招聘到员工——如果没有大规模裁员使得消费者支出大幅下滑,经济不太可能出现严重衰退。他还指出,尽管去年利率飙升,但住房库存接近历史最低点,他认为这将使房地产领域全年都实现解冻。

他表示:“不过,我们需要美联储暂停[加息],美国的国内生产总值可能会出现一两个季度的负增长,但不会陷入严重的经济衰退。”(财富中文网)

译者:中慧言-王芳

After years of cheap money helped fuel the rise of speculative investing and profitless business models in the U.S. over the past decade, stubborn inflation has forced the Federal Reserve to increase interest rates faster than ever before in 2022. Now, a new era of higher borrowing costs and more cautious lenders—coupled with slowing growth and recession fears—has frozen once-red hot segments of the U.S. economy.

The initial public offering (IPO) market is essentially shut; tech companies are laying off workers and pausing hiring; the housing market is experiencing a “reset” after years of booming growth; and the venture capital (VC) space has slowed dramatically, with private market valuations tumbling.

But despite the freeze in key sectors—and consistent doomsday predictions from Wall Street—the economy as a whole has continued to grow alongside the resilient labor market. In the fourth quarter of last year, U.S. gross domestic product (GDP) rose at a 2.9% annualized rate, topping analysts’ forecasts. And the unemployment rate came in near pre-pandemic lows at 3.5% in December.

Many economists are predicting that will change this year, however. Morgan Stanley’s chief U.S. economist Ellen Zentner said this week that annualized GDP growth will fall to just 0.2% in the first quarter, while Wells Fargo expects a drop to 0.4%. And some CEOs, billionaire investors, and investment banks believe an outright recession is on the way.

It’s still unclear whether key frozen aspects of the economy will eventually crack under the weight of rising interest rates—sparking a recession—or if the deep freeze will thaw—enabling slow, but positive growth. But credit markets could hold the answer.

“When credit markets pull back, and you’re unable to get financing for transactions or for investment, that’s when things freeze,” Jim Cahn, chief investments and business development officer at Wealth Enhancement Group, a wealth management firm, told Fortune. “Credit is the secret. It’s the fuel of growth. And it’s always been the fuel of growth, since the credit markets evolved 400 years ago at the beginning of the industrial revolution.”

The freezing and frozen segments of the economy

A new era of higher interest rates, inflation, and recession fears have led various segments of the U.S. economy to slow dramatically over the past year.

Venture Capital

The VC space, for example, was supercharged throughout the pandemic. In 2021, global VC funding volume reached a record $681 billion, more than double 2019’s figures.

“[A] growth-at-all-cost mindset fueled by cheap capital in 2020 and 2021 and exploding investor interest caused by a fear of missing out (FOMO) led to large investments into startups across all stages,” Alex Warfel, a PitchBook analyst, explained in a Friday note.

But in 2022, with interest rates rising, there was a 35% decline in VC investment to $445 billion, according to Crunchbase. Warfel said the days of “sky-high valuations for startups and easy fundraising opportunities” are gone, sentiment in the VC space has been “crushed,” and capital has dried up. To his point, the estimated amount of capital demanded by U.S. startups outpaced the amount supplied by $42.8 billion in the fourth quarter, according to PitchBook data.

Logan Allin, founder of Fin Capital, a fintech-focused VC and private equity firm, told Fortune that he doesn’t see the VC space recovering fully until 2024 due in part to the credit crunch, and he argued that for tech startups, 2023 could be a particularly challenging year.

“Our view is that 2023 is going to continue to be a year of extremely acute pain, and actually more painful than 2022 from both a private markets and public equity perspective in tech,” he said.

Allin added the sharp downturn in the market should be a “bit of a wake up call” for VC investors who developed irresponsible habits during the pandemic, failing to do proper due diligence for their investments. He gave the example of the now-defunct crypto exchange, FTX, which he “passed on” because they didn’t get past basic “checklist items” in the due diligence process, including not allowing an independent auditor to look at their financials. But other venture capitalists invested millions in the firm without even looking at their books.

“They were asking for financials and the team at FTX was sending them excel spreadsheets,” he said. “It was just absurd.”

But now, with interest rates rising and many lesser VCs going out of business, Allin believes the market will return to a more rigorous investing approach.

“I think it will be a much healthier, more sustainable venture capital environment now, because we’re investing in valuations and multiples that make sense and that allow the company to grow into them in a much better way,” he said. “It’s a true return to fundamentals. It is a refocusing on real diligence.”

IPOs

When U.S. interest rates were near zero and consumers were flush with cash from stimulus checks during the pandemic, the IPO market experienced a similar surge to the VC space.

In 2021 alone there were a record 1,033 new public listings in the U.S. But in 2022—with interest rates rising and the S&P 500 sinking roughly 20%—there was a 50% reduction in the number of IPOs compared, according to EY’s 2022 Global IPO Trends Report. And in the Americas, the drop was even more pronounced, with the number of IPOs falling 86% last year versus 2021, while total proceeds sank 96% over the same period.

“Deal activity and volume came down precipitously throughout 2022. IPOs were completely shuttered,” Allin said. “There was very little public market appetite for anything, even those companies that were potentially profitable.”

This year, Allin said he sees just a “sliver of an IPO window,” and only for firms that can prove their ability to make money.

“Otherwise, they’re going to trade significantly down, as any of the companies that went public last year or in 2021 did,” he said. “We still have inflation, high interest rates, geopolitical uncertainty, and significant volatility, and that does not create a warm market for IPOs.”

Housing

U.S. home prices soared over 45% between the second quarter of 2020 and the third quarter of last year, as low interest rates and work-from-home trends fueled a housing market boom. But rising interest rates have pushed the averaged 30-year fixed mortgage rate—the most common type in the U.S.—from 3.45% in February of 2020 to just over 6.1% today.

The higher borrowing costs and high home prices have led to an affordability crunch and a major “reset” in the housing market. Mortgage purchase applications were down 39% from a year ago last week.

It’s not just prospective homeowners who are feeling shut out—institutional real estate investors are feeling the pain from rising interest rates as well, according to Jay Hatfield, founder and CEO of the investment management firm Infrastructure Capital Advisors. Higher rates and recession fears have caused lending from banks to “dry up,” he told Fortune, making acquiring new properties—and/or companies in the real estate sector—a challenge.

“There’s a little bit of private lending going on, but it’s at terms that are too onerous to do LBOs [leveraged buyouts] anymore,” he said, referring to when one company tries to buy another company using borrowed money. “And then also, the companies that were buyers like Blackstone. They’re more likely to be sellers than buyers now. So M&A activity has dried up.”

Cahn of Wealth Enhancement Group says that lenders are not only offering much higher interest rates, but they’re also doing a lot more underwriting—or research and risk assessment—before lending money to avoid default risk. He noted that it’s another example that the current freeze in some sectors of the economy is all a “reflection of what’s going on in the credit markets.”

“In 2021, and 18 months before, people were just throwing money at anything as fast as they could because there was so much cash, but in 2022, the credit markets basically froze up,” he emphasized. “And that’s why you’re seeing these industries freeze.”

The frozen economy that’s about to crack?

Will the economy slowly thaw out and avoid a recession, or are the cracks caused by rising interest rates and high inflation about to rupture? That depends on who you ask.

Cahn said his “hunch” is that we’ll have a recession “sometime in the back half of 2023. “I think it’s really, you know, maybe 2024, before we’re back in business as usual,” he said.

He’s not the only one with a pessimistic outlook. Many top investment banks are forecasting a “mild recession” this year, and some forecasters have argued that “severe recession” or even “another variant of a Great Depression” could be on the way.

“We’re definitely going to enter into a harder and harder period from an economic and macro standpoint, that may be a capital “R” recession or lowercase “r” recession, but it’s going to be bad,” Allin said.

While many experts believe a recession is on the way, some argue it won’t be as devastating as past downturns, and the frozen sectors of the economy will begin to unfreeze by the end of 2023 and into 2024. Infrastructure Capital Advisors’ Hatfield said that by the second half of this year “we’ll have a more normal IPO market and a recovery M&A and stock market.”

He argued that “post pandemic tailwinds” have kept the labor market healthy—particularly in the services sector where so many businesses struggled to find workers during the pandemic—and without wide-spread layoffs that crush consumer spending, it’s unlikely there will be a serious downturn in the economy. He also noted that despite the rapid rise in interest rates last year, housing inventories are near an all-time low which he believes will allow that sector to unfreeze throughout the year.

“We need the Fed to pause [interest rate hikes] though,” he said. “And we might get a negative quarter or two [of GDP], but we don’t think we’re gonna have a significant recession.”