企业负债屡创新高,信用评级却不断下滑

Larry Light

2019-12-11

一旦企业的现金流在经济衰退中枯竭,大额利息支付迫在眉睫,投资者就要当心了。

文本设置

文本设置

Plus(0条)

Plus(0条)

|

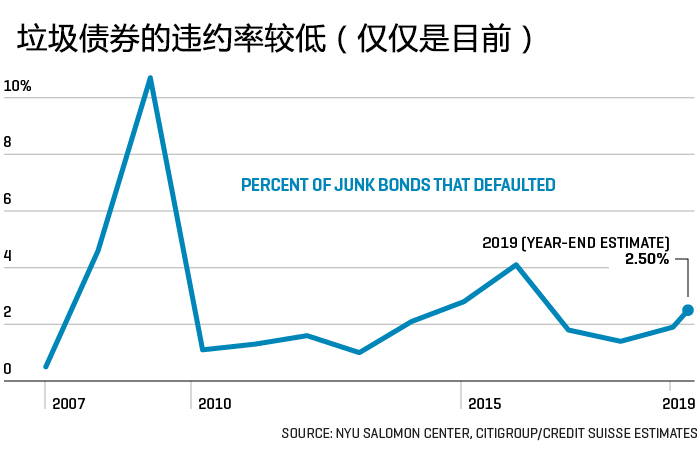

虽然美国股市正在创下历史新高,但还有一个令人担忧的数字也在创下历史新高:企业持有的债务总额,尤其是高风险债务额。 根据圣路易斯联邦储备银行(St. Louis Federal Reserve Bank)的数据,美国企业债务(不包括金融公司)自2008年以来飙升了50%以上,达到约10万亿美元,占国内生产总值的47%,创下历史新高。宽松的资金流动意味着高管们的梦想可能会成真:管理层把借来的低息资金用于新产品发布、收购、股票回购、增加股息——而这些都是当前经济扩张的标志。 对于美国企业来说,近年来大笔举债似乎是理性的,毕竟,真的很便宜!在2008年至2009年可怕的全球金融危机之后,美联储和其他央行放任自流,急不可耐地将利率降至极低水平,以期重振资本主义被击溃的活力。“债务这么便宜,为什么不借呢?”荷兰全球人寿资产管理公司(Aegon Asset Management)的副首席投资官吉姆·谢弗表示。 不过,在此过程中,债务不断增加,信用质量却出现下滑。咨询公司德勤(Deloitte)表示,在从大衰退中复苏的过程里,投资级债券的市场份额降至78.6%,而在前两次复苏中这一比例约为90%。更糟糕的是,银行向高杠杆公司发放的贷款正在增加,而对高风险债券发行人行为的限制(称为契约)如今要宽松得多。 纽约大学斯特恩商学院的荣誉退休教授、纽约大学所罗门中心信贷与固定收益研究项目的主任爱德华·阿尔特曼表示:“若拖欠债务率再次达到峰值,无论发生在什么时候,程度都将十分严重。”他认为,届时产生的痛苦将比正常情况下持续得更久,违约造成的损失将比正常情况下更多。 随着垃圾债务的增加,欧洲太平洋资本公司(Euro Pacific Capital)的首席执行官彼得·希夫在最近的一篇博客文章中写道:“就像一个巨大的纸牌屋,只等着有什么东西碰一碰桌子,把整间屋子全部推倒。” 目前,美国未偿付的高收益债券总额为1.5万亿美元,而2007年为7,000亿美元(经通胀调整后为8,690亿美元)。如果经济衰退来袭,收入和收益就会枯竭,垃圾债券的违约率会飙升到两位数。据阿尔特曼估计,在上一次经济衰退中,高收益债券的违约率飙升至10.7%。在此之前的两次经济衰退中,违约率最高值分别为2002年的12.8%和1991年的10.3%。本次经济复苏期间,在油价暴跌导致收益下降和美国经济增长放缓之后,违约率在2016年一度升至4.1%。 感到疼痛 若危机来袭,问题将主要集中在投资级以下的公司。知名债券研究机构Gimme Credit列出了10家高收益债券发行人,它们的债券表现最有可能表现低于投资者预期,其中包括汽车租赁公司Hertz,到服装品牌Limited Brands(陷入困境的维多利亚的秘密的母公司),再到赌场Mohegan Gaming & Entertainment。 药店连锁来德爱(Rite Aid)也在Gimme Credit的名单上,说明这家公司摇摇欲坠、负债累累。它的杠杆率很高,是安全水平的三倍多:来德爱的长期债务是该公司息税折旧及摊销前利润(EBITDA)的6.8倍。在激烈的竞争中,该连锁店上一个财年和今年前两个季度都出现了亏损。 然而药店不属于周期性行业,因为人们总是需要处方药、牙膏和创可贴,所以来德爱现在的财务状况足以让投资者担心它的未来。它的同店销售增长徘徊在负增长和弱增长之间。过去三年,公司的股价下跌了92%。 当然,没有人能够预测,当经济衰退到来时,一家如今压力重重的公司是否会进入破产保护状态。但是,经济困难的重击可能会让情况变得更糟,因为它增加了公司在债务到期时无法支付利息或返还本金的可能性。 暴风雨前的平静? |

While the stock market is hitting new all-time highs, so is another more alarming statistic: the amount of debt held by corporations, especially the riskiest kind. U.S. corporate debt (excluding financial firms) surged more than 50% since 2008 to around $10 trillion, a record 47% of gross domestic product, according to the St. Louis Federal Reserve Bank. The flow of easy money meant C-suite dreams could come true: Managements used the cut-rate borrowed money for new product launches, acquisitions, stock buybacks, dividend boosts—all the hallmarks of the economy’s current expansion. For Corporate America, heaping on all this corporate debt in recent years seemed rational, after all, it's a bargain! Following the terrifying 2008-09 global financial crisis, an indulgent Federal Reserve and other central banks eagerly pushed interest rates very low, bidding to revive capitalism’s crushed animal spirits. “Debt’s been cheap, so why not do it?” said Jim Schaeffer, deputy chief investment officer of Aegon Asset Management. Along the way, though, the credit quality of that growing debt pile has slipped. During the recovery from the Great Recession, the portion of the market made up of investment grade bonds fell to 78.6%, from around 90% in the previous two recoveries, says consulting firm Deloitte. Making matters worse, bank loans to highly leveraged companies are growing, and restrictions on risky debt issuer behavior, called covenants, are much weaker nowadays. “The magnitude of the next spike in default rates, whenever it occurs, will be severe,” said Edward Altman, professor emeritus at New York University’s Stern School of Business and director of the Credit and Fixed Income Research Program at the NYU Salomon Center. The pain will last longer than is typical, he believes, and more money will be lost than normal through defaults. With more junk debt around, Peter Schiff, CEO of Euro Pacific Capital, wrote in a recent blog post: “This is a giant house of cards just waiting for something to nudge the table and send the whole thing toppling down.” Today, outstanding high-yield bonds in the U.S. total $1.5 trillion, up from $700 billion in 2007 (or $869 billion if inflation-adjusted). When a recession hits, revenues and earnings dry up, and junk default rates tend to surge into double digits. In the last recession, high-yield default levels soared to 10.7%, by Altman’s estimate. For the two downturns before that, they peaked at 12.8% in 2002 and 10.3% in 1991. During the current recovery, defaults temporarily blipped up to 4.1% in 2016, after the oil-price bust lowered earnings and U.S. economic growth. Feeling the pain The trouble, when it hits, will mostly be concentrated in companies with below investment grade designations. Gimme Credit, a well-regarded bond research house, lists 10 high-yield issuers whose bonds are most likely to under-perform for investors. They range from auto renter Hertz to apparel purveyor Limited Brands (parent of struggling Victoria’s Secret) to casino company Mohegan Gaming & Entertainment. Drugstore chain Rite Aid, also on the Gimme Credit's list, is emblematic of a precarious, debt-laden corporation. Its leverage ratio is high, more than three times what’s considered safe: Rite Aid’s long-term debt is 6.8 times the money the company generates in earnings before interest, taxes, depreciation and amortization, or EBITDA. Amid bruising competition, the chain has been in the red for its last fiscal year and the first two quarters in this year. While drugstores aren’t a cyclical industry—people always need prescriptions, toothpaste and Band-Aids—Rite Aid’s financial picture is wobbly enough to make investors worry about its future. Its same-store sales growth shuttles between negative and anemic. Over the last three years, the stock has tumbled 92%. Certainly, no one can predict whether a stressed company today will be in Chapter 11 when the recession arrives. But the hammer blows of a bad economy will probably make things a lot worse, as it increases the likelihood that a company can’t pay interest or return principal when it’s due. Calm before the storm? |

|

垃圾债券市场目前表现平静,因此阿尔特曼和希夫的警告似乎是危言耸听。今年迄今为止,美国垃圾债券的违约率仅为1.9%,远低于3.3%的历史平均水平。对投机性票据的需求是健康的,因为在一个低利率的世界里,它的利率是诱人的。Diamond Hill Capital Management公司固定收益部门的首席投资官比尔·佐克斯表示:“投资者如今不记风险地追逐过高的收益率。” 随着买家哄抬价格,大多数垃圾债券的平均收益率在2019年出现了下降:例如,B级垃圾债券的收益率从1月初的略高于8.45%降至6.0%。(价格和收益率走向相反。)美国银行(Bank of America)的高收益指数今年已经攀升11.6%。 然而,令人不安的是,投资者的信心并没有扩大至垃圾级的最低水平——CCC。投资者正在更糟的情况出现之前抛售这些CCC级债券,其中很多来自境况不佳的能源发行者。这一事态鲜有人注意,但引发了人们的担忧,因为CCC级债券的抛售可能是经济出现某些问题的先兆,而这种问题将会蔓延至其它垃圾债券。 未来不完美 一旦现金流在经济衰退中枯竭,大额利息支付迫在眉睫,就要当心了。那时,一切都可以很快完蛋。小裂缝变成大断裂。许多公司已经意识到自己的债务风险——不管是否属于垃圾债券——都在尽其所能降低杠杆,为金融气候的变化做准备。 评级为垃圾级的来德爱为摆脱沉重的债务负担做出了坚定努力,不过它还有很长的路要走,资源也很紧张。在美国连锁药店中,来德爱不幸屈居第三,仅排在沃博联(Walgreens Boots Alliance)和CVS Health之后。该公司曾经试图与沃尔格林(Walgreens)合并,后来又试图与食品和药品零售商艾伯森(Albertsons)合并,但都以失败告终。为了筹集资金偿还债务,来德爱最终将其近一半的门店出售给了沃尔格林,这进一步影响了未来的收入。 标准普尔(Standard & Poor’s)于今年 4月将来德爱的评级从B降至B-,原因是该公司运营中存在缺陷,在刚刚结束的财年业绩不佳。最近,管理层以39%的折扣回购了价值8,400万美元的债券,并提出以同样的价格再买进1亿美元。来德爱通过循环贷款融通进行支付,这种工具收取的利息明显低于债券支付的利息,为7.7%和6.875%。 这家连锁企业因此遇上了麻烦,这种回购被标普称为“廉价交易”,因为这种操作导致投资者获得的收益减少了。标准普尔因此将来德爱从B-级信用评级下调至SD级(选择性违约)。 来德爱通过一名发言人回应称,这种认定是“临时的,在这类交易中很常见”。标准普尔补充称,一旦该公司的要约完成,它将重新评估该问题。 该公司指出,其债券短期内不会到期,第一批债券的到期时间是2023年。该药店连锁企业在9月下旬举行的第二季度财报电话会议上,新任首席执行官海沃德·多尼根表示:“来德爱需要一个清晰的新战略愿景,以及一条能够推动未来实现有机增长和盈利的执行路径。” 没人知道当经济衰退的寒风吹来时,来德爱和其他类似公司会怎么样。但有一件事情是肯定的:欠的钱总是要还的。(财富中文网) 译者:Agatha |

Amid the junk market’s present calm, admonitions like Altman’s and Schiff’s seem alarmist. Thus far this year, the U.S. junk default rate is a low 1.9%, well beneath the 3.3% historical average. Demand is healthy for speculative paper, since its interest rates are enticing in a low-rate world. “Investors will reach for yield these days,” said Bill Zox, chief investment officer for fixed income at Diamond Hill Capital Management. As buyers bid up prices, most junk bonds have seen their average yields drop in 2019: B-rated junk, for instance, has fallen to 6.0%, from just over 8.45% in early January. (Prices and yields move in opposite directions.) Bank of America’s high-yield index has climbed 11.6% year-to-date. What’s troubling, however, is that investor confidence doesn’t extend to the lowest level of junk, CCC. Investors are dumping the CCCs, much of them from woebegone energy issuers, before something bad happens. This little-noticed development has prompted worry that the CCC selloff might be the harbinger of a malaise that will spread to other junk issues. Future imperfect Once cash flows dry up in a recession and big interest payments loom, look out. Then, everything can go to hell very quickly. Small cracks become major fractures. Aware of their debt exposure, many companies—whether in the junk yard or not¬—are preparing for a change in the financial weather by de-levering as best they can. Junk-rated Rite Aid has made valiant efforts to shed its big debt load, although it has a long way to go and tight resources to get there. Rite Aid has the misfortune of being the distant third in the U.S. drugstore chain realm, behind Walgreens Boots Alliance and CVS Health. Attempts to merge fizzled with Walgreens and later with food and drug retailer Albertsons. To raise cash to retire debt, Rite Aid ended up selling almost half its stores to Walgreens, which had the added effect of crimping revenue going forward. Citing operational shortcomings, Standard & Poor’s in April downgraded Rite Aid to B- from B, following weak results in its just-concluded fiscal year. Recently, management repurchased $84 million worth of bonds at a 39% discount and offered to buy in another $100 million at a similar level. Rite Aid is paying for this via a revolving loan facility that apparently charges less interest than the bonds pay out, 7.7% and 6.875%. That tactic landed the chain in trouble with S&P, which branded the repurchase a “distressed exchange” because the maneuver offered investors less than what they had. The agency lowered Rite Aid’s junk B- rating to a category called SD, for selective default. Rite Aid responded, through a spokesman, that this designation is “temporary and common in these types of transactions.” S&P added that it will reevaluate the issue once the company’s offer is complete. The company notes that its next bonds aren’t slated to mature for a while, with the first due in 2023. In remarks at the drug chain’s second quarter earnings call in late September, new CEO Heyward Donigan said, “Rite Aid needs a clear new strategic vision and a pathway to execution that drives future organic growth and profitability.” No one can tell how Rite Aid and others like it will fare when the chill recession winds blow. But one thing’s for sure: there’s always payback time. |

请打开财富Plus APP