后疫情时代,美国经济为何能够反弹

Will Daniel

2024-03-25

美国经济在后疫情时代的反弹让全美专家都大跌眼镜。

文本设置

文本设置

Plus(0条)

Plus(0条)

“美国例外主义”存在已经有数百年时间,一直饱受争议。目前,民主党与共和党均在利用该理论来推进自己提出的议程。这个理论认为,美国拥有许多与众不同、独一无二的特质,其支持者和反对者均试图以该理论为依据,对美国的无数特征(从枪支暴力犯罪居高不下到不正常的医疗保健费用,再到对权威的蔑视和对自力更生的坚持)进行解释。

尽管对于“美国例外主义”在政治领域能否站得住脚目前尚无定论,但过去几年,美国经济和股市的出色表现却让这一理论成为“显学”。而且几乎没有人想到美国经济可以有如此例外的表现。

美国经济在后疫情时代的反弹让全美专家都大跌眼镜。有一些经济学常识的人都知道,在自20世纪80年代以来最严重通胀浪潮和利率快速上升的双重压力之下,美国经济本来应该是“雪上加霜”。再考虑到受到俄乌、巴以两场战争影响,供应链一片混乱,能源价格进一步走高,难怪一众经济学家和华尔街领袖近年来一致认为美国经济将走向衰退。

不过,虽然一路经历了各种“惊涛骇浪”,但美国消费者和企业却似乎挺了过来,成功创造了经济奇迹。美国经济仍在持续增长,在极具韧性的劳动力市场支撑下,美国经济取得了出乎意料的成功。虽然生活成本高昂问题依然严峻,但后疫情时代的美国却仍然实现了强劲的经济反弹,这一点在与其他发达国家比较时表现得尤为明显。

2023年第四季度,美国国内生产总值(GDP)的年化增长率为3.3%,而欧元区20国仅为0.1%,日本为1.1%。根据国际货币基金组织(International Monetary Fund)发布的《世界经济展望》(World Economic Outlook),2023年全年,美国国内生产总值的增速为2.5%,在G7经济体中名列首位。

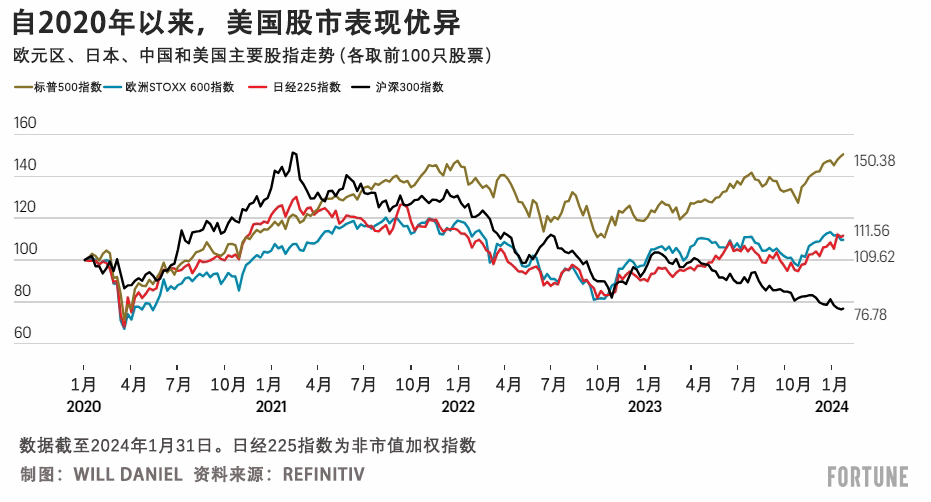

自2020年年初的新冠疫情爆发以来,受美国经济强劲表现拉动,美国股市的表现也优于其他发达国家市场。2020年1月以来,标准普尔500指数(S&P 500)上涨了53%,相比之下,欧洲STOXX 600指数的涨幅为16%,日本日经225指数(非加权)的涨幅为52%,中国沪深300指数更是下跌了23%。

美国经济之所以能够在后疫情时代取得优异表现,原因有很多,从美国在能源上的相对独立到其在应对新冠疫情时采取的积极财政和货币政策,不一而足。这些优势可以帮助美股在未来几年继续保持优异表现。

SEI Investments的首席市场策略师兼高级投资组合经理詹姆斯·索洛维在接受《财富》杂志采访时表示:“美国目前的状况依旧好于其他大多数国家,其目前的经济增速高于平均水平,虽然多少有一些出人意料,但却是正在发生的现实,这也给2024年开了一个好头。”

尽管如此,各种不可预测的风险(从美国选举的结果到国外战争的影响等)仍旧不可等闲视之。而且美股在经过过去几年的暴涨之后,估值已经很高。对投资者来说,即便美国经济的表现仍将优于其他发达国家,把全部身家都押在美国股市还会继续上涨上可能也并非最好的选择。在这个充满不确定性的时代,把所有鸡蛋都放在一个篮子里难免会有风险。

索洛维说:“我认为,就当下而言,最好还是进行分散投资。美国股市之所以一路高歌猛进,主要得益于美国股市的增长特性,但相对于其他国家,美国股市的估值已经相对偏高。”

不过,放眼2024年,美国经济可能仍将显著优于全球平均水平。对投资者来说,了解个中原因能够帮助其更好地选择下一步的投资方向,判断美国经济还可以在多长时间内在全球独领风骚。

有力的财政应对政策

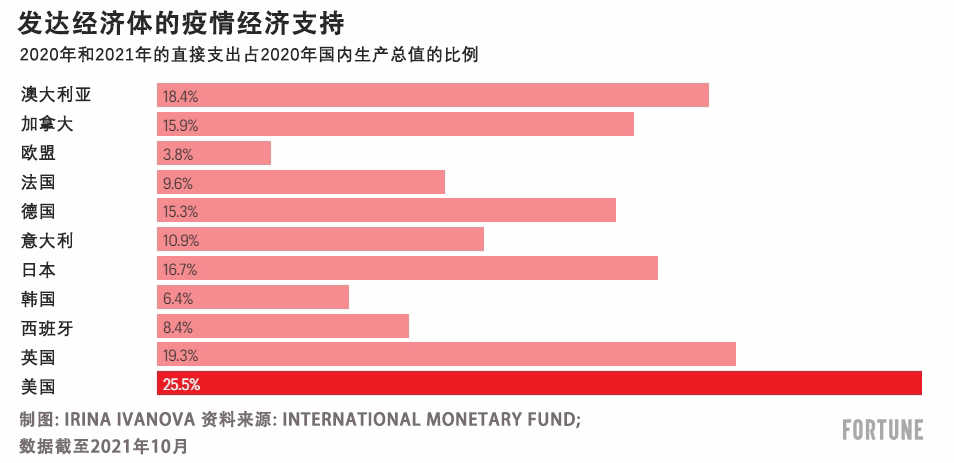

2020年年初,新冠疫情爆发,全球经济陷于停滞,为支持本国经济,各发达国家政府采取了截然不同的方法。截至目前,美国联邦政府在支出方面的做法最为积极,通过了六项新冠救济法案,在2020年和2021年共支出4.6万亿美元,约占美国国内生产总值的10%。

SEI的索洛维指出,美国的新冠财政救济支出不仅占国内生产总值的比重最大,也“更加直接,美国政府直接把钱发到了民众手中,为企业提供支持,而不仅仅是提供贷款担保”。

索洛维说,这种强力财政对策可能确实推高了通胀,但也帮助许多美国人在支出自然减少时保持了收入水平。由于收入相对稳定、支出相对较低,消费者在新冠疫情期间积累了所谓的“超额储蓄”。截至2021年8月,美国人的超额储蓄已经超过2万亿美元,这些储蓄帮助刺激了消费支出,防止了经济出现衰退。

抵御利率上升的能力

在货币方面,美联储(U.S. Federal Reserve)在新冠疫情爆发时采取了激进的降息策略,把利率降至近零水平。美国消费者和企业迅速行动,利用较低的借贷成本,在利率处于历史低位时对抵押贷款和其他贷款进行再融资。这种做法帮助他们以比预期更快的速度从疫情引发的短暂衰退中恢复过来,并在利率上升时保持了一定的支出能力。

索洛维称:“由于家庭和企业都在非常低的利率水平上进行了再融资,所以在利率上升时,他们都有一定的抵御能力。因此,与其他许多国家的民众相比,美国人并未立即感受到利率上升的影响。”

当中央银行提高利率时,企业和消费者的借贷成本就会提高,放在各国皆是如此。但借贷成本上升对消费者和企业的影响速度和严重程度却不尽相同,例如在过去几年,美国联邦储备委员会、英格兰银行(Bank of England)和欧洲中央银行(European Central Bank)都提高了利率,影响却各不相同。

以住房贷款为例。根据Bankrate的数据,2023年,美国79%的抵押贷款为30年或15年期固定利率贷款。相反,根据英国金融行为监管局(Financial Conduct Authority)的数据,英国74%的抵押贷款为2年到5年期固定利率贷款,到期后就需要重新进行融资。

因此,据英国《卫报》(Guardian)2023年12月报道,自2021年年底以来,英国55%的抵押贷款利率出现上升。而Redfin的数据显示,即便美国30年期抵押贷款的平均利率在2023年出现了大幅提高(先是飙升至8%,后又回落至近7%),美国近90%房主的抵押贷款利率依然低于6%。

索洛维解释道,对美国的许多房主而言,只有当“他们自身的情况发生变化,比如有了孩子,需要换一套大房子时,才会开始感受到更高利率带来的影响”。

能源独立

与其他发达国家相比,美国的能源相对独立,这也是其在过去几年里表现优异的另一个原因。

过去五年,美国天然气产量激增,在2023年创下历史新高。而这一变化的意义在于,2022年2月俄乌冲突爆发后,美国经济比许多发达国家更不容易受到天然气价格上涨的影响。高度依赖俄罗斯天然气的欧洲国家的天然气价格在2022年8月达到了每百万英国热量单位(BTU)70余美元的历史峰值,而在美国,这一数字仅为10美元。

近年来,美国能源业在全球液化天然气(LNG)市场逐步占据了主导地位,欧洲对美国液化天然气的依赖也越来越大。牛津经济研究院(Oxford Economics)的首席全球经济学家英尼斯·麦克菲解释道,由于缺乏能源独立性,“欧洲工业在与美国同行竞争时处于结构性劣势”。

除此之外,虽然由于俄乌冲突引发油价上涨,美国经济也受到了一定影响,但在美国总统乔·拜登释放1.8亿桶战略石油储备后,相关影响得到了有效的缓解。美国的能源公司也因为产量飙升创造了盈利纪录。这些都有助于提高美国公司的收益和股票价格,同时也为许多美国人提供了高薪工作。

美国石油产量在2023年创下历史新高,据美国能源信息署(U.S. Energy Information Agency)预计,在“油井产量提升”推动下,2024年和2025年的石油产量将再创新高。这对于防止油价进一步飙升、加剧通货膨胀会很有帮助。

美国经济能否继续独占鳌头?

为解释美国经济为何可以在后疫情时代表现优异,专家们给出了许多解释,上述因素只是其中几个而已。有经济学家指出,由于美国的资本市场更为发达,所以美国企业能够在困难时期随时获得现金,并帮助雇主留住工人。还有更多人认为,由于美国在科技领域占据主导地位,美国经济和股市得以成为这轮人工智能热潮的主要受益者。也有人指出,由于新冠疫情期间美国政府以经济刺激金的形式为美国消费者提供了直接支持,一批新企业应运而生,员工技能提升也蔚然成风,进而推动了生产率提升和经济增长。说了这么多,我们甚至还没有触及其他发达国家所面临的国内经济问题。

美国银行研究部(Bank of America Research)的经济学家们曾经预测美国将会陷入衰退,结果却欣喜地发现美国经济的表现出乎意料的强劲,对于究竟是什么因素在推动美国股市不断走高,他们给出了另一种解读,那就是投资者的“FOMO” (fear of missing out,意为害怕错过)心态。本杰明·鲍勒领导的全球股票衍生品研究(Global Equity Derivatives Research)团队在其2024年展望中写道,“害怕错过”成了“投资者脑海中最关心的事情”,对于增加更大宏观不确定性的许多重大基本面和政策面风险,则放在了次要位置。

“FOMO”是千禧一代的口头禅,由哈佛商学院(Harvard Business School)的一名学生于2004年在其于校刊上发表的一篇评论文章中首次提出。但这种情绪不禁让人想起几十年前也有过用于形容投资者热情的类似委婉说法:20世纪90年代美联储主席艾伦·格林斯潘口中的“非理性繁荣”,和20世纪30年代传奇经济学家约翰·梅纳德·凯恩斯最喜欢用的“动物精神”。这种东西多了就会产生泡沫,然后就会突然破灭,就像互联网泡沫那样,格林斯潘时代的非理性繁荣就是因为这种泡沫的破灭而宣告终结。

但真正的问题依旧没有找到答案,那就是:美国目前良好的状态能否持续下去?在推动美国经济实现强劲增长方面,有些因素目前确实发挥着积极作用,但在未来却有可能成为拖累。对科技垄断和赤字支出的依赖可能会让美国在未来付出沉痛的代价。同样,超额储蓄的消退和高昂的生活成本也会打击消费者信心,抑制经济增长。但牛津经济研究院的麦克菲认为,“与其他发达市场相比,美国的前景实际上仍然相当不错”。

麦克菲预测,美国今年的实际收入增长率将达到2.5%,有助于支持消费支出,而欧洲的实际收入增长率仅为1%。他还预计美国的财政政策将比欧洲“支持力度更大”,因为欧洲的趋势是“整顿和控制预算赤字”。

他补充道:“美国经济的供应面看起来更强劲一些。今年美国的生产率增长非常强劲,其他国家可不是这样。”与之观点类似,国际货币基金组织的经济学家预测,2024年美国经济的国内生产总值的增速将达到2.1%,高于七国集团的其他所有经济体。

尽管如此,麦克菲依然警告说,今年的总统大选给美国经济的发展打上了一个“大大的问号”,选举结果将是决定经济未来走向的关键。

“大选之后,美国将会推出怎样的政策?”他问道。“唐纳德·特朗普的减税政策将于明年到期。因此,下届政府很可能会对税收政策进行调整。我认为,这将对美国能否继续跑赢其他发达市场产生重大影响。”

SEI的索洛维也认为大选给2024年带来了很多“不确定性”,但他补充道,美国经济还有一个或许可以使其免受大选结果影响、继续蓬勃发展的特点。索洛维指出:“即便在经济低谷期,美国经济和投资者也能够适应环境的变化。实际上,在过去十多年里一些非常艰难的时期,我们的经济表现也十分亮眼,股市业绩也十分优异。”(财富中文网)

译者:梁宇

审校:夏林

“美国例外主义”存在已经有数百年时间,一直饱受争议。目前,民主党与共和党均在利用该理论来推进自己提出的议程。这个理论认为,美国拥有许多与众不同、独一无二的特质,其支持者和反对者均试图以该理论为依据,对美国的无数特征(从枪支暴力犯罪居高不下到不正常的医疗保健费用,再到对权威的蔑视和对自力更生的坚持)进行解释。

尽管对于“美国例外主义”在政治领域能否站得住脚目前尚无定论,但过去几年,美国经济和股市的出色表现却让这一理论成为“显学”。而且几乎没有人想到美国经济可以有如此例外的表现。

美国经济在后疫情时代的反弹让全美专家都大跌眼镜。有一些经济学常识的人都知道,在自20世纪80年代以来最严重通胀浪潮和利率快速上升的双重压力之下,美国经济本来应该是“雪上加霜”。再考虑到受到俄乌、巴以两场战争影响,供应链一片混乱,能源价格进一步走高,难怪一众经济学家和华尔街领袖近年来一致认为美国经济将走向衰退。

不过,虽然一路经历了各种“惊涛骇浪”,但美国消费者和企业却似乎挺了过来,成功创造了经济奇迹。美国经济仍在持续增长,在极具韧性的劳动力市场支撑下,美国经济取得了出乎意料的成功。虽然生活成本高昂问题依然严峻,但后疫情时代的美国却仍然实现了强劲的经济反弹,这一点在与其他发达国家比较时表现得尤为明显。

2023年第四季度,美国国内生产总值(GDP)的年化增长率为3.3%,而欧元区20国仅为0.1%,日本为1.1%。根据国际货币基金组织(International Monetary Fund)发布的《世界经济展望》(World Economic Outlook),2023年全年,美国国内生产总值的增速为2.5%,在G7经济体中名列首位。

自2020年年初的新冠疫情爆发以来,受美国经济强劲表现拉动,美国股市的表现也优于其他发达国家市场。2020年1月以来,标准普尔500指数(S&P 500)上涨了53%,相比之下,欧洲STOXX 600指数的涨幅为16%,日本日经225指数(非加权)的涨幅为52%,中国沪深300指数更是下跌了23%。

美国经济之所以能够在后疫情时代取得优异表现,原因有很多,从美国在能源上的相对独立到其在应对新冠疫情时采取的积极财政和货币政策,不一而足。这些优势可以帮助美股在未来几年继续保持优异表现。

SEI Investments的首席市场策略师兼高级投资组合经理詹姆斯·索洛维在接受《财富》杂志采访时表示:“美国目前的状况依旧好于其他大多数国家,其目前的经济增速高于平均水平,虽然多少有一些出人意料,但却是正在发生的现实,这也给2024年开了一个好头。”

尽管如此,各种不可预测的风险(从美国选举的结果到国外战争的影响等)仍旧不可等闲视之。而且美股在经过过去几年的暴涨之后,估值已经很高。对投资者来说,即便美国经济的表现仍将优于其他发达国家,把全部身家都押在美国股市还会继续上涨上可能也并非最好的选择。在这个充满不确定性的时代,把所有鸡蛋都放在一个篮子里难免会有风险。

索洛维说:“我认为,就当下而言,最好还是进行分散投资。美国股市之所以一路高歌猛进,主要得益于美国股市的增长特性,但相对于其他国家,美国股市的估值已经相对偏高。”

不过,放眼2024年,美国经济可能仍将显著优于全球平均水平。对投资者来说,了解个中原因能够帮助其更好地选择下一步的投资方向,判断美国经济还可以在多长时间内在全球独领风骚。

有力的财政应对政策

2020年年初,新冠疫情爆发,全球经济陷于停滞,为支持本国经济,各发达国家政府采取了截然不同的方法。截至目前,美国联邦政府在支出方面的做法最为积极,通过了六项新冠救济法案,在2020年和2021年共支出4.6万亿美元,约占美国国内生产总值的10%。

SEI的索洛维指出,美国的新冠财政救济支出不仅占国内生产总值的比重最大,也“更加直接,美国政府直接把钱发到了民众手中,为企业提供支持,而不仅仅是提供贷款担保”。

索洛维说,这种强力财政对策可能确实推高了通胀,但也帮助许多美国人在支出自然减少时保持了收入水平。由于收入相对稳定、支出相对较低,消费者在新冠疫情期间积累了所谓的“超额储蓄”。截至2021年8月,美国人的超额储蓄已经超过2万亿美元,这些储蓄帮助刺激了消费支出,防止了经济出现衰退。

抵御利率上升的能力

在货币方面,美联储(U.S. Federal Reserve)在新冠疫情爆发时采取了激进的降息策略,把利率降至近零水平。美国消费者和企业迅速行动,利用较低的借贷成本,在利率处于历史低位时对抵押贷款和其他贷款进行再融资。这种做法帮助他们以比预期更快的速度从疫情引发的短暂衰退中恢复过来,并在利率上升时保持了一定的支出能力。

索洛维称:“由于家庭和企业都在非常低的利率水平上进行了再融资,所以在利率上升时,他们都有一定的抵御能力。因此,与其他许多国家的民众相比,美国人并未立即感受到利率上升的影响。”

当中央银行提高利率时,企业和消费者的借贷成本就会提高,放在各国皆是如此。但借贷成本上升对消费者和企业的影响速度和严重程度却不尽相同,例如在过去几年,美国联邦储备委员会、英格兰银行(Bank of England)和欧洲中央银行(European Central Bank)都提高了利率,影响却各不相同。

以住房贷款为例。根据Bankrate的数据,2023年,美国79%的抵押贷款为30年或15年期固定利率贷款。相反,根据英国金融行为监管局(Financial Conduct Authority)的数据,英国74%的抵押贷款为2年到5年期固定利率贷款,到期后就需要重新进行融资。

因此,据英国《卫报》(Guardian)2023年12月报道,自2021年年底以来,英国55%的抵押贷款利率出现上升。而Redfin的数据显示,即便美国30年期抵押贷款的平均利率在2023年出现了大幅提高(先是飙升至8%,后又回落至近7%),美国近90%房主的抵押贷款利率依然低于6%。

索洛维解释道,对美国的许多房主而言,只有当“他们自身的情况发生变化,比如有了孩子,需要换一套大房子时,才会开始感受到更高利率带来的影响”。

能源独立

与其他发达国家相比,美国的能源相对独立,这也是其在过去几年里表现优异的另一个原因。

过去五年,美国天然气产量激增,在2023年创下历史新高。而这一变化的意义在于,2022年2月俄乌冲突爆发后,美国经济比许多发达国家更不容易受到天然气价格上涨的影响。高度依赖俄罗斯天然气的欧洲国家的天然气价格在2022年8月达到了每百万英国热量单位(BTU)70余美元的历史峰值,而在美国,这一数字仅为10美元。

近年来,美国能源业在全球液化天然气(LNG)市场逐步占据了主导地位,欧洲对美国液化天然气的依赖也越来越大。牛津经济研究院(Oxford Economics)的首席全球经济学家英尼斯·麦克菲解释道,由于缺乏能源独立性,“欧洲工业在与美国同行竞争时处于结构性劣势”。

除此之外,虽然由于俄乌冲突引发油价上涨,美国经济也受到了一定影响,但在美国总统乔·拜登释放1.8亿桶战略石油储备后,相关影响得到了有效的缓解。美国的能源公司也因为产量飙升创造了盈利纪录。这些都有助于提高美国公司的收益和股票价格,同时也为许多美国人提供了高薪工作。

美国石油产量在2023年创下历史新高,据美国能源信息署(U.S. Energy Information Agency)预计,在“油井产量提升”推动下,2024年和2025年的石油产量将再创新高。这对于防止油价进一步飙升、加剧通货膨胀会很有帮助。

美国经济能否继续独占鳌头?

为解释美国经济为何可以在后疫情时代表现优异,专家们给出了许多解释,上述因素只是其中几个而已。有经济学家指出,由于美国的资本市场更为发达,所以美国企业能够在困难时期随时获得现金,并帮助雇主留住工人。还有更多人认为,由于美国在科技领域占据主导地位,美国经济和股市得以成为这轮人工智能热潮的主要受益者。也有人指出,由于新冠疫情期间美国政府以经济刺激金的形式为美国消费者提供了直接支持,一批新企业应运而生,员工技能提升也蔚然成风,进而推动了生产率提升和经济增长。说了这么多,我们甚至还没有触及其他发达国家所面临的国内经济问题。

美国银行研究部(Bank of America Research)的经济学家们曾经预测美国将会陷入衰退,结果却欣喜地发现美国经济的表现出乎意料的强劲,对于究竟是什么因素在推动美国股市不断走高,他们给出了另一种解读,那就是投资者的“FOMO” (fear of missing out,意为害怕错过)心态。本杰明·鲍勒领导的全球股票衍生品研究(Global Equity Derivatives Research)团队在其2024年展望中写道,“害怕错过”成了“投资者脑海中最关心的事情”,对于增加更大宏观不确定性的许多重大基本面和政策面风险,则放在了次要位置。

“FOMO”是千禧一代的口头禅,由哈佛商学院(Harvard Business School)的一名学生于2004年在其于校刊上发表的一篇评论文章中首次提出。但这种情绪不禁让人想起几十年前也有过用于形容投资者热情的类似委婉说法:20世纪90年代美联储主席艾伦·格林斯潘口中的“非理性繁荣”,和20世纪30年代传奇经济学家约翰·梅纳德·凯恩斯最喜欢用的“动物精神”。这种东西多了就会产生泡沫,然后就会突然破灭,就像互联网泡沫那样,格林斯潘时代的非理性繁荣就是因为这种泡沫的破灭而宣告终结。

但真正的问题依旧没有找到答案,那就是:美国目前良好的状态能否持续下去?在推动美国经济实现强劲增长方面,有些因素目前确实发挥着积极作用,但在未来却有可能成为拖累。对科技垄断和赤字支出的依赖可能会让美国在未来付出沉痛的代价。同样,超额储蓄的消退和高昂的生活成本也会打击消费者信心,抑制经济增长。但牛津经济研究院的麦克菲认为,“与其他发达市场相比,美国的前景实际上仍然相当不错”。

麦克菲预测,美国今年的实际收入增长率将达到2.5%,有助于支持消费支出,而欧洲的实际收入增长率仅为1%。他还预计美国的财政政策将比欧洲“支持力度更大”,因为欧洲的趋势是“整顿和控制预算赤字”。

他补充道:“美国经济的供应面看起来更强劲一些。今年美国的生产率增长非常强劲,其他国家可不是这样。”与之观点类似,国际货币基金组织的经济学家预测,2024年美国经济的国内生产总值的增速将达到2.1%,高于七国集团的其他所有经济体。

尽管如此,麦克菲依然警告说,今年的总统大选给美国经济的发展打上了一个“大大的问号”,选举结果将是决定经济未来走向的关键。

“大选之后,美国将会推出怎样的政策?”他问道。“唐纳德·特朗普的减税政策将于明年到期。因此,下届政府很可能会对税收政策进行调整。我认为,这将对美国能否继续跑赢其他发达市场产生重大影响。”

SEI的索洛维也认为大选给2024年带来了很多“不确定性”,但他补充道,美国经济还有一个或许可以使其免受大选结果影响、继续蓬勃发展的特点。索洛维指出:“即便在经济低谷期,美国经济和投资者也能够适应环境的变化。实际上,在过去十多年里一些非常艰难的时期,我们的经济表现也十分亮眼,股市业绩也十分优异。”(财富中文网)

译者:梁宇

审校:夏林

The entire concept of “American exceptionalism” is controversial. Used by both major parties to advance their agendas of the moment, the belief that there’s something distinct and unique about America has been present for hundreds of years. It’s been co-opted by both boosters and detractors to explain away countless features of the U.S. landscape—from our high rates of gun violence and abnormal health care costs to our disdain for authority and penchant for self-reliance.

But while American exceptionalism may or may not be real in the political realm, it’s been front and center in the remarkable performance of the U.S. economy and stock market over the past few years. And almost nobody saw this exceptionalism coming.

The United States’ post-COVID rebound thoroughly surprised experts across the nation. Consult the economics textbooks, and the combined force of the worst inflationary wave since the 1980s and rapidly rising interest rates should have left the American economy looking worse for wear. Tack on two foreign wars that have crimped supply chains and boosted energy prices, and it makes sense why a U.S. recession was the near-unanimous expectation of many economists and Wall Street leaders for years.

Still, despite all these storm clouds, it looks like American consumers and businesses have so far defied the odds. The economy continues to grow, with a resilient labor market underpinning its largely unexpected success. And while serious cost of living issues remain, the U.S.’s post-COVID rebound has been particularly strong when compared to its developed peers.

In the fourth quarter of 2023, U.S. GDP grew at an annual rate of 3.3%, compared to just 0.1% for the 20 nations that make up the Euro Area, and 1.1% for Japan. And for all of 2023, U.S. GDP rose 2.5%, more than any other G7 economy, according to the International Monetary Fund’s (IMF) World Economic Outlook.

The economic strength has helped U.S. stocks trounce their developed market peers since the outbreak of COVID in early 2020. The S&P 500 is up over 53% since Jan. 2020, compared to a 16% rise for the STOXX Europe 600 index, a 52% jump for Japan’s Nikkei 225 (non-cap weighted), and a 23% drop for China’s CSI 300 index.

There are a few key reasons why the U.S. economy has outperformed in the post-COVID era, from the country’s relative energy independence to its aggressive fiscal and monetary response to the pandemic. They’re advantages that could help American stocks maintain their exceptional run of performance over the next few years.

“The U.S. is still in a better position than most other countries right now,” James Solloway, chief market strategist and senior portfolio manager at SEI Investments, told Fortune. “We're seeing above average growth, which is somewhat surprising, but nonetheless, it's happening. So we’ve entered 2024 with a bit of momentum.”

That being said, unpredictable risks, from the outcome of domestic elections to the impact of foreign wars, could still rear their head. And after U.S. stocks’ big run-up over the past few years, valuations are high. For investors, that means going all in on another era of U.S. stock market dominance may not be the best choice, even if the U.S. economy is set to outperform its developed peers. In this era of uncertainty, keeping all your eggs in one basket could be risky.

“I think that at this point, it pays to be diversified,” Solloway said. “The United States has had a great run, mainly owing to the growth nature of the stock markets here, but valuations have become quite stretched relative to other countries.”

Still, the U.S. may remain the global economy’s outlier in 2024—in a good way. And understanding why can help investors decide which way to go next, and how long this era of outperformance could go on.

A big fiscal response

When the outbreak of COVID-19 shut down the global economy in early 2020, the governments of developed nations took very different approaches to supporting their domestic economies. The U.S. federal government was by far the most aggressive with spending, dishing out $4.6 trillion, or roughly 10% of U.S. GDP in 2020 and 2021, through six COVID-19 relief laws.

SEI’s Solloway noted that not only did the U.S. have the largest fiscal response to the pandemic relative to the size of its economy, its COVID relief spending was also “much more direct, putting money into people's pockets and supporting businesses directly, as opposed to just providing loan guarantees.”

This forceful fiscal response may have boosted inflation, Solloway said, but it also helped many Americans maintain their incomes during a period when spending was naturally lower. The combination of relatively stable incomes and lower spending helped consumers build up so-called “excess savings” during the pandemic. By August 2021, Americans had over $2 trillion in excess savings, and those savings helped buoy consumer spending and prevent a recession.

Resilience to rising interest rates

On the monetary side of things, the U.S. Federal Reserve was also very aggressive in cutting interest rates to near-zero when the pandemic hit. American consumers and businesses were quick to take advantage of the lower borrowing costs, refinancing mortgages and other loans while rates were historically low. That’s helped them recover from the brief COVID-induced downturn faster than anticipated, and maintain some spending power even as interest rates have risen.

“Households and businesses both had some insulation from the increase in rates… because both refinanced at very low interest rates,” Solloway said. “And therefore they have not immediately felt the impact of higher rates yet, as opposed to a lot of other countries.”

When central banks hike interest rates, it raises borrowing costs for all businesses and consumers—and that’s true in every country. But how quickly and severely higher borrowing costs affect consumers and businesses isn’t the same—a fact on display over the past few years with the U.S. Federal Reserve, the Bank of England, and the European Central Bank all raising rates.

Take housing. In the U.S., 79% of all mortgages had fixed rates of 30 or 15 years in 2023, according to Bankrate. Conversely, in the U.K., 74% of mortgages currently have interest rates that are fixed for two to five years before they need to be re-financed, according to data from the U.K.’s Financial Conduct Authority.

As a result, 55% of U.K. mortgages saw their interest rate increase since the end of 2021, the Guardian reported in December. But in the U.S., nearly 90% of homeowners still have mortgage rates under 6%, even as average 30-year mortgage rates spiked to 8% last year before falling to nearly 7%, Redfin data shows.

For many U.S. homeowners, it’s only when “their situation changes, they have a family, they need to move to a bigger house that they start feeling the impact of higher interest rates,” Solloway explained.

Energy independence

The U.S.’s relative energy independence compared to its developed nation peers is another reason it managed to outperform over the past few years.

U.S. natural gas production has soared in the past five years, hitting a record high in 2023. When Russia invaded Ukraine in February 2022, that meant the U.S. economy was more insulated from rising natural gas prices than many of its developed peers. European national gas prices, which are highly reliant on Russian gas, peaked at over over $70 per million British Thermal Units (BTU) in August 2022, compared to a peak of just $10 per million BTU in the U.S.

The U.S. energy industry has also developed a dominant position in the liquefied natural gas (LNG) market in recent years, with Europe increasingly relying on the U.S.’s LNG. Innes McFee, chief global economist at Oxford Economics, explained that Europe’s lack of energy independence “puts European industry at a structural disadvantage versus U.S. counterparts.”

On top of that, although the U.S. economy was affected by rising oil prices after the start of the Ukraine war, President Biden’s release of 180 million barrels of oil from the strategic petroleum reserve helped blunt the impact. U.S. energy companies were also able to rake in record profits as their production soared. That helped boost U.S. corporate earnings and stock prices, while providing high-paying jobs for many Americans.

U.S. oil production hit a record high in 2023 as well, and the U.S. Energy Information Agency expects “improved well productivity” will lead to two more record production years in 2024 and 2025. That should help prevent another oil price spike that could exacerbate inflation.

Will the U.S. continue to outperform?

The factors described above are just a few of the many that experts offer to explain the U.S. economies’ post-COVID outperformance. Other economists point to the U.S.’s more developed capital markets, saying they enable U.S. businesses to readily access cash in tough times, and have helped employers hang onto workers. Still more say U.S. tech dominance has made the American economy and stock market the major beneficiary of the AI boom. And others note that the direct support for American consumers in the form of stimulus checks led to a wave of new business formation and the upskilling of workers in the U.S. during the COVID era, which has worked to increase productivity and economic growth ever since. All of this doesn’t even touch on the domestic economic problems that other developed nations are facing—particularly China, with its ailing housing market.

Bank of America Research, whose own economists predicted a recession only to be happily surprised by the U.S. economy’s strong performance, have another idea about what could be driving the U.S. stock market: investors’ “FOMO.” The Global Equity Derivatives Research team, led by Benjamin Bowler, wrote in its 2024 outlook that “fear of missing out” was “winning the war in investors’ minds” over the many material fundamental and policy risks adding to larger macro uncertainty.

The “FOMO” term is a millennial standby, invented in 2004 by a Harvard Business School student writing an opinion piece in the school magazine. But the sentiment recalls similar euphemisms for investor enthusiasm from decades before: “irrational exuberance” was Fed chair Alan Greenspan’s parlance in the 1990s, and “animal spirits” was the preferred description from legendary economist John Maynard Keynes in the 1930s. Too much of this kind of thing can create bubbles that suddenly burst, just as it did during the dotcom bust, finishing off the Greenspan-era irrational exuberance.

The real question, however, remains: can the U.S.’ run of good form last? Some of the drivers of the current strength are also potential liabilities. Dependence on tech monopolies and deficit spending could trigger a painful correction. Similarly, fading excess savings and the high cost of living could dampen consumer confidence, stifling growth. But according to Oxford Economics’ McFee, “the outlook for the U.S. is actually still pretty good relative to other peers in developed markets.”

McFee forecasts 2.5% real income growth in the U.S. this year, which should help support consumer spending, compared to just 1% in Europe. He also expects fiscal policy to be “much more supportive” in the U.S. than in Europe, where the trend is toward “consolidation and reining in budget deficits.”

“The supply side of the U.S. economy looks a bit stronger. And you've seen really strong productivity growth in the U.S. this year— that's not really the case elsewhere,” he added. To his point, IMF economists are forecasting 2.1% GDP growth for the U.S. economy in 2024, more than any other G7 economy.

All of that being said, McFee warned that the presidential election year creates one “big question” that will be key to determining the economy’s future.

“What will policy look like after the election?” he asked. “We've got the Trump tax cuts expiring next year. So there's a really big opportunity to shape tax policy in the next administration. And I think that will have a big influence on whether or not the U.S. can continue to outperform other developed markets.”

SEI’s Solloway agreed that the election creates a lot of “uncertainty” in 2024, but added that the U.S. economy has another feature that should help it thrive no matter who is in office. “You know, the U.S. economy and investors adapt, even in harrowing times,” he noted. “We’ve actually seen a very good economy, and we've seen a very good stock market, during some very trying times over the last decade-plus.”

请打开财富Plus APP