2024年应该投资哪些行业?

WILL DANIEL

2024-01-02

2024年,经济韧性为投资者创造了关键机会。

文本设置

文本设置

Plus(0条)

Plus(0条)

2023年12月13日,纽约证券交易所(New York Stock Exchange)早盘交易大厅。图片来源:MICHAEL M. SANTIAGO—GETTY IMAGES

2023年12月13日,纽约证券交易所(New York Stock Exchange)早盘交易大厅。图片来源:MICHAEL M. SANTIAGO—GETTY IMAGES一年前,华尔街还在担心通货膨胀、利率高企且持续更长时间以及欧洲爆发的新冲突。这一系列经济利空因素造成的冲突本应引发美国经济衰退,导致华尔街看空市场前景。尽管地缘政治紧张局势依然存在,并因以色列和哈马斯之间新爆发的冲突而进一步恶化,但是通胀正在消退;美联储目前正计划实施降息;经济衰退从未到来。

在2024年,经济韧性为投资者创造了关键机会,从搭乘人工智能的炒作列车到参与私人信贷热潮。华尔街领袖和财富经理们对这些新投资趋势津津乐道(在这一点上请相信我)。然而,总统大选在即、冲突愈演愈烈、利率上调仍对消费者造成压力,环境仍不明朗,风险无处不在。

金融大师们最青睐的新趋势可能会带来巨大利润,但这些趋势都有严重的下行风险,尤其是如果事实证明华尔街对经济衰退的预测并没有出现偏差,只是为时过早。不过,对于精明的投资者,甚至是想深入了解专业人士新宠的外行来说,2024年关注这些趋势可能会有所收获。

人工智能热潮

机遇

经过一年不间断的头条新闻、学术论文和华尔街报告,大多数人都厌倦人工智能话题。但是,在讨论2024年的关键投资主题时,是不可能忽视人工智能的。许多华尔街领袖认为,人工智能正在引领第四次工业革命。韦德布什证券公司(Wedbush)顶级科技分析师丹·艾夫斯(Dan Ives)说,对于投资者来说,这是一场类似于互联网发明的现代“淘金热”。

在CFRA Research分析师贾尼斯·奎克(Janice Quek)和安杰洛·齐诺(Angelo Zino)看来,2024年人工智能的崛起给投资者带来的主要好处将是信息技术预算的增加,因为企业将花费更多资金来创建人工智能应用程序。他们指出,根据高德纳(Gartner)的预测,2024年的信息技术支出将同比增长8%,其中在人工智能热潮中,软件支出将增长13.8%。相比之下,2023年的信息技术预算仅增长了3.5%。

奎克和齐诺将科技巨头微软(Microsoft)、软件公司ServiceNow和Datadog以及网络安全公司CrowdStrike和帕洛阿尔托网络公司(Palo Alto Networks)列为2024年人工智能的首选。他们在上周四的一份报告中指出,这些公司的人工智能产品和基于云计算的服务种类繁多,具备“赶上”人工智能相关信息技术支出热潮的良好条件。

风险

华尔街对人工智能的热情可能足以填满大峡谷,但人们对这项技术仍持怀疑态度。Key Private Bank首席投资官乔治·马特约(George Mateyo)说,人们普遍认为,人工智能最终将惠及从医疗保健和科技公司到制造业和金融服务巨头等众多公司。但关键问题是,在2024年,人工智能的潜力能在多大程度上转化为盈利增长——没有人知道确切答案。

“显而易见的是,人工智能的采用周期非常短。与之前的智能手机和个人电脑相比,人工智能的普及速度更快。”马特约告诉《财富》杂志。“但我确实认为,人们可能有点过于乐观,认为这一切(与人工智能相关的盈利增长)都将在2024年实现。”

马特约认为,即使这项技术的积极影响最终会“扩大”,人工智能对工作人员生产率的提升可能需要数年时间才能让许多上市公司实现利润增长。

Segal Marco Advisors首席投资官苏·克罗蒂(Sue Crotty)进一步详细阐述了她对人工智能的看法。她说:“虽然从长远来看,(人工智能)将改变游戏规则,但如今我认为这只是一场炒作,你可以引用我的这句表述。人工智能频频登上头条新闻,但实际情况却不同。”

私人信贷的辉煌时代

机遇

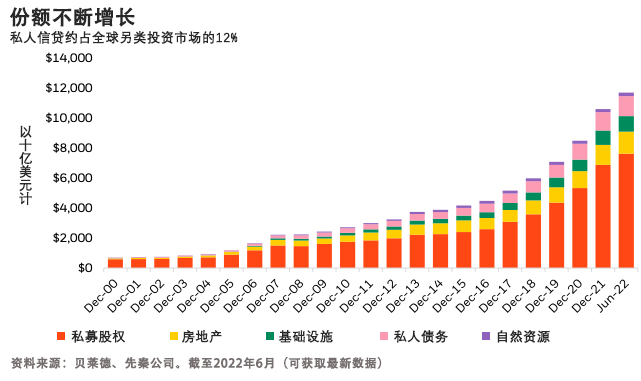

2024年的另一大关键主题可能是私人信贷的持续增长。近年来,利率上调推高了银行的存款成本和资金需求,导致其放贷频率降低。这为私人贷款机构填补有现金需求的公司或房地产项目的资金缺口打开了大门。

据彭博社报道,贝莱德(BlackRock)的数据显示,在过去几年里,私人信贷市场已发展成为一个1.6万亿美元的庞大市场。根据先秦公司(Preqin)的一项研究,随着增长持续,到2028年,该市场的价值将达到2.8万亿美元,贝莱德估计该市场的价值甚至会达到35亿美元。

另类投资平台Fundrise的联合创始人兼首席执行官本·米勒(Ben Miller)描述了在高利率环境下直接借贷(又称私人信贷)的吸引力。随着银行收紧贷款条件,许多房地产开发或租赁项目难以获得资金。“银行不放贷,而且我认为它们在很长一段时间内都不会放贷。”米勒对《财富》杂志表示,他认为银行的许多资产都被“锁定”在低利率时发放的长期贷款中。

缺乏公共贷款机构迫使许多公司和房地产项目转向私人市场,后者可以提供贷款,但利率要高得多。“我们主要专注于住宅公寓的私人贷款。我们可以为一个高价值的房地产项目设置14%的利率。”米勒解释道。“这简直高得离谱。”

然而,就连米勒也发现了私人信贷市场的风险。他认为,随着利率下降,房地产市场可能已经触底,但经济的其他部分还没有触底,经济衰退即将到来。

他警告说:“高利率要到2024年和2025年才会对大多数公司和民众造成冲击。”他认为,到2024年,向企业提供私人贷款的风险将高于向住宅房地产项目提供贷款的风险。

风险

私人借贷的风险无疑很高。以至于参议院银行委员会主席谢罗德·布朗(Sherrod Brown,民主党-俄亥俄州)在2023年11月致信美联储负责金融监管业务的副主席迈克尔·巴尔(Michael Barr)、联邦存款保险公司(FDIC)主席马丁·格鲁恩伯格(Martin Gruenberg)和货币监理署署长迈克尔·许(Michael Hsu),警告称私人信贷市场可能充满隐患。这位参议员写道:“与传统银行业不同,私人信贷市场只受到最低限度的间接监管,缺乏透明度,掩盖了其真实规模和风险。”

《财富》杂志采访的专家也对直接借贷市场不断上升的风险表示担忧。Colony Group首席市场策略师瑞奇·斯坦伯格(Rich Steinberg)解释说,私人信贷提供的9%至14%的回报率吸引了许多新投资者进入这一领域,但“该市场正变得人满为患”。这意味着,任何寻求将资金投入私人信贷的人都需要花时间寻找合适的机会,并确保值得信赖的贷款机构为私人贷款提供担保,而且进行过适当的尽职调查。

他对《财富》杂志表示,总的来说,私人信贷“实际上是为那些有能力将其作为多元化收入战略的一部分的更老练的客户准备的。”

Certuity首席投资官迪伦·克雷默(Dylan Kremer)说,他也认为投资者“在寻求将资金投入私人信贷时需要完成尽职调查”。

他说:“现在有如此多的资本追逐私人信贷,投资者需要充分了解(管理公司)和他们使用的基金,以确保私人贷款的担保标准和结构设计是正确的。”

Key private Bank的马特约表示,私人信贷领域总体上有很多机会,但这些产品“缺乏透明度”,对低收入投资者来说可能存在风险。他解释说:“从某种意义上说,它是一种非流动性资产类别,并不适合所有人。它不像短期国债,明天就可以出售,然后获得资金用于购物。”

小盘股复苏?

机遇

对于坚信华尔街经济衰退预测偏离事实的投资者来说,小盘股可能是2024年的投资良机。多年来,小盘股的表现一直落后于大盘股,但许多专家认为,这种情况将在2024年及以后发生改变。

Fundstrat Global Advisors联合创始人汤姆·李(Tom Lee)最近表示,随着通胀回到美联储2%的目标水平,利率下降,追踪小盘股的罗素2000指数2024年可能飙升50%。小盘股通常比大盘股负债更多,在过去几年里因借贷成本上升而遭受重创,但李表示,这种情况即将结束。此外,小盘股的价格历来都很便宜。“以市净率计算,相对于标准普尔指数,目前(小盘股)的交易价格与1999年的水平相当。那是持续12年跑赢大盘周期的开始。”李告诉美国全国广播公司财经频道(CNBC)。

拉扎德(Lazard)公司首席市场策略师罗纳德·坦普尔(Ronald Temple)说,他也看到了小型上市公司命运“开始逆转的迹象”。和李一样,他也指出,小盘股公司承担的债务更多,包括更多的浮动利率债务。他在2023年12月初的一份报告中写道:“鉴于这种浮动风险敞口,如果美联储转向削减短期利率,小盘股可能会比大盘股受益更多。”

坦普尔还认为,相对于大盘股,小盘股公司具有“引人注目”的价值,而且由于小盘股公司的收入更多来自美国,它们可以从美国经济持续优于发达市场同行的表现中获益。

他解释说:“罗素2000指数成分股约90%的收入来自美国,而标准普尔500指数成分股约60%至65%的收入来自美国。在我们看来,考虑到2024年及以后美国经济增长的预期韧性水平(相对而言),这些公司以国内发展为导向应该是一个利好因素。”

风险

虽然小盘股可能会在2024年反弹,但它们2023年的表现逊于大盘股也是有原因的。根据拉扎德的数据,罗素2000指数中约有40%的公司在过去一年亏损。许多规模较小的上市公司仍然需要为浮动利率债务进行再融资,这些债务是它们在利率较低时借入的,而现在的利率要高得多。盈利疲软和债务成本上升相结合,可能会在2024年成为一大挑战,尤其是如果美国经济衰退最终到来的话。

一些专家甚至警告说,在全球金融危机后的近零利率时代,许多商业模式无利可图的小型美国公司得以存活,这意味着相当数量濒临倒闭的公司即将破产。根据国际货币基金组织(IMF)最近的一项研究,这些所谓的“僵尸公司”在美国上市公司中所占的比例已从2000年的略高于6%增至2021年的超过10%。

正如《财富》杂志此前报道的那样,New Constructs首席执行官大卫·特雷纳(David Trainer)多年来一直在追踪僵尸公司,他警告称,随着利率上升,许多僵尸公司将破产。2023年11月,在WeWork (特雷纳所谓的僵尸公司之一)倒闭后,他再次发出警告。他说:“WeWork的破产只是僵尸公司崩溃的开始。投资者需要关注那些真正盈利并拥有可行商业模式的公司。烧钱不是一种商业模式。”

需要明确的是,大多数小盘股并不是僵尸公司,但如果熊市的预测是正确的话,那么商界的这些行尸走肉可能会在2024年拖垮同行,使小盘股的投资吸引力下降。(财富中文网)

译者:中慧言-王芳

一年前,华尔街还在担心通货膨胀、利率高企且持续更长时间以及欧洲爆发的新冲突。这一系列经济利空因素造成的冲突本应引发美国经济衰退,导致华尔街看空市场前景。尽管地缘政治紧张局势依然存在,并因以色列和哈马斯之间新爆发的冲突而进一步恶化,但是通胀正在消退;美联储目前正计划实施降息;经济衰退从未到来。

在2024年,经济韧性为投资者创造了关键机会,从搭乘人工智能的炒作列车到参与私人信贷热潮。华尔街领袖和财富经理们对这些新投资趋势津津乐道(在这一点上请相信我)。然而,总统大选在即、冲突愈演愈烈、利率上调仍对消费者造成压力,环境仍不明朗,风险无处不在。

金融大师们最青睐的新趋势可能会带来巨大利润,但这些趋势都有严重的下行风险,尤其是如果事实证明华尔街对经济衰退的预测并没有出现偏差,只是为时过早。不过,对于精明的投资者,甚至是想深入了解专业人士新宠的外行来说,明年关注这些趋势可能会有所收获。

人工智能热潮

机遇

经过一年不间断的头条新闻、学术论文和华尔街报告,大多数人都厌倦人工智能话题。但是,在讨论2024年的关键投资主题时,是不可能忽视人工智能的。许多华尔街领袖认为,人工智能正在引领第四次工业革命。韦德布什证券公司(Wedbush)顶级科技分析师丹·艾夫斯(Dan Ives)说,对于投资者来说,这是一场类似于互联网发明的现代"淘金热"。

在CFRA Research分析师贾尼斯·奎克(Janice Quek)和安杰洛·齐诺(Angelo Zino)看来,2024年人工智能的崛起给投资者带来的主要好处将是信息技术预算的增加,因为企业将花费更多资金来创建人工智能应用程序。他们指出,根据高德纳(Gartner)的预测,2024年的信息技术支出将同比增长8%,其中在人工智能热潮中,软件支出将增长13.8%。相比之下,今年的信息技术预算仅增长了3.5%。

奎克和齐诺将科技巨头微软(Microsoft)、软件公司ServiceNow和Datadog以及网络安全公司CrowdStrike和帕洛阿尔托网络公司(Palo Alto Networks)列为2024年人工智能的首选。他们在周四的一份报告中指出,这些公司的人工智能产品和基于云计算的服务种类繁多,具备“赶上”人工智能相关信息技术支出热潮的良好条件。

欲了解更多人工智能热门股,请查看《财富》杂志列出的2024年最值得购买的股票清单,重点包括华尔街顶级投资者的推荐股。

风险

华尔街对人工智能的热情可能足以填满大峡谷,但人们对这项技术仍持怀疑态度。Key Private Bank首席投资官乔治·马特约(George Mateyo)说,人们普遍认为,人工智能最终将惠及从医疗保健和科技公司到制造业和金融服务巨头等众多公司。但关键问题是,在2024年,人工智能的潜力能在多大程度上转化为盈利增长——没有人知道确切答案。

"显而易见的是,人工智能的采用周期非常短。与之前的智能手机和个人电脑相比,人工智能的普及速度更快。"马特约告诉《财富》杂志。"但我确实认为,人们可能有点过于乐观,认为这一切(与人工智能相关的盈利增长)都将在2024年实现。"

马特约认为,即使这项技术的积极影响最终会“扩大”,人工智能对工作人员生产率的提升可能需要数年时间才能让许多上市公司实现利润增长。

Segal Marco Advisors首席投资官苏·克罗蒂(Sue Crotty)进一步详细阐述了她对人工智能的看法。她说:“虽然从长远来看,(人工智能)将改变游戏规则,但如今我认为这只是一场炒作,你可以引用我的这句表述。人工智能频频登上头条新闻,但实际情况却不同。”

私人信贷的辉煌时代

机遇

2024年的另一大关键主题可能是私人信贷的持续增长。近年来,利率上调推高了银行的存款成本和资金需求,导致其放贷频率降低。这为私人贷款机构填补有现金需求的公司或房地产项目的资金缺口打开了大门。

据彭博社报道,贝莱德(BlackRock)的数据显示,在过去几年里,私人信贷市场已发展成为一个1.6万亿美元的庞大市场。根据先秦公司(Preqin)的一项研究,随着增长持续,到2028年,该市场的价值将达到2.8万亿美元,贝莱德估计该市场的价值甚至会达到35亿美元。

另类投资平台Fundrise的联合创始人兼首席执行官本·米勒(Ben Miller)描述了在高利率环境下直接借贷(又称私人信贷)的吸引力。随着银行收紧贷款条件,许多房地产开发或租赁项目难以获得资金。“银行不放贷,而且我认为它们在很长一段时间内都不会放贷。”米勒对《财富》杂志表示,他认为银行的许多资产都被“锁定”在低利率时发放的长期贷款中。

缺乏公共贷款机构迫使许多公司和房地产项目转向私人市场,后者可以提供贷款,但利率要高得多。“我们主要专注于住宅公寓的私人贷款。我们可以为一个高价值的房地产项目设置14%的利率。”米勒解释道。“这简直高得离谱。”

然而,就连米勒也发现了私人信贷市场的风险。他认为,随着利率下降,房地产市场可能已经触底,但经济的其他部分还没有触底,经济衰退即将到来。

他警告说:“高利率要到明年和后年才会对大多数公司和民众造成冲击。”他认为,到2024年,向企业提供私人贷款的风险将高于向住宅房地产项目提供贷款的风险。

风险

私人借贷的风险无疑很高。以至于参议院银行委员会主席谢罗德·布朗(Sherrod Brown,民主党-俄亥俄州)在11月致信美联储负责金融监管业务的副主席迈克尔·巴尔(Michael Barr)、联邦存款保险公司(FDIC)主席马丁·格鲁恩伯格(Martin Gruenberg)和货币监理署署长迈克尔·许(Michael Hsu),警告称私人信贷市场可能充满隐患。这位参议员写道:"与传统银行业不同,私人信贷市场只受到最低限度的间接监管,缺乏透明度,掩盖了其真实规模和风险。"

《财富》杂志采访的专家也对直接借贷市场不断上升的风险表示担忧。Colony Group首席市场策略师瑞奇·斯坦伯格(Rich Steinberg)解释说,私人信贷提供的9%至14%的回报率吸引了许多新投资者进入这一领域,但“该市场正变得人满为患”。这意味着,任何寻求将资金投入私人信贷的人都需要花时间寻找合适的机会,并确保值得信赖的贷款机构为私人贷款提供担保,而且进行过适当的尽职调查。

他对《财富》杂志表示,总的来说,私人信贷“实际上是为那些有能力将其作为多元化收入战略的一部分的更老练的客户准备的。”

Certuity首席投资官迪伦·克雷默(Dylan Kremer)说,他也认为投资者"在寻求将资金投入私人信贷时需要完成尽职调查"。

他说:"现在有如此多的资本追逐私人信贷,投资者需要充分了解(管理公司)和他们使用的基金,以确保私人贷款的担保标准和结构设计是正确的。”

Key private Bank的马特约表示,私人信贷领域总体上有很多机会,但这些产品“缺乏透明度”,对低收入投资者来说可能存在风险。他解释说:“从某种意义上说,它是一种非流动性资产类别,并不适合所有人。它不像短期国债,明天就可以出售,然后获得资金用于购物。”

小盘股复苏?

机遇

对于坚信华尔街经济衰退预测偏离事实的投资者来说,小盘股可能是明年的投资良机。多年来,小盘股的表现一直落后于大盘股,但许多专家认为,这种情况将在2024年及以后发生改变。

Fundstrat Global Advisors联合创始人汤姆·李(Tom Lee)最近表示,随着通胀回到美联储2%的目标水平,利率下降,追踪小盘股的罗素2000指数明年可能飙升50%。小盘股通常比大盘股负债更多,在过去几年里因借贷成本上升而遭受重创,但李表示,这种情况即将结束。此外,小盘股的价格历来都很便宜。“以市净率计算,相对于标准普尔指数,目前(小盘股)的交易价格与1999年的水平相当。那是持续12年跑赢大盘周期的开始。”李告诉美国全国广播公司财经频道(CNBC)。

拉扎德(Lazard)公司首席市场策略师罗纳德·坦普尔(Ronald Temple)说,他也看到了小型上市公司命运"开始逆转的迹象"。和李一样,他也指出,小盘股公司承担的债务更多,包括更多的浮动利率债务。"他在12月初的一份报告中写道:"鉴于这种浮动风险敞口,如果美联储转向削减短期利率,小盘股可能会比大盘股受益更多。”

坦普尔还认为,相对于大盘股,小盘股公司具有"引人注目"的价值,而且由于小盘股公司的收入更多来自美国,它们可以从美国经济持续优于发达市场同行的表现中获益。

他解释说:“罗素2000指数成分股约90%的收入来自美国,而标准普尔500指数成分股约60%至65%的收入来自美国。“在我们看来,考虑到2024年及以后美国经济增长的预期韧性水平(相对而言),这些公司以国内发展为导向应该是一个利好因素。”

风险

虽然小盘股可能会在2024年反弹,但它们今年的表现逊于大盘股也是有原因的。根据拉扎德的数据,罗素2000指数中约有40%的公司在过去一年亏损。许多规模较小的上市公司仍然需要为浮动利率债务进行再融资,这些债务是它们在利率较低时借入的,而现在的利率要高得多。盈利疲软和债务成本上升相结合,可能会在2024年成为一大挑战,尤其是如果美国经济衰退最终到来的话。

一些专家甚至警告说,在全球金融危机后的近零利率时代,许多商业模式无利可图的小型美国公司得以存活,这意味着相当数量濒临倒闭的公司即将破产。根据国际货币基金组织(IMF)最近的一项研究,这些所谓的"僵尸公司"在美国上市公司中所占的比例已从2000年的略高于6%增至2021年的超过10%。

正如《财富》杂志此前报道的那样,New Constructs首席执行官大卫·特雷纳(David Trainer)多年来一直在追踪僵尸公司,他警告称,随着利率上升,许多僵尸公司将破产。上个月,在WeWork (特雷纳所谓的僵尸公司之一)倒闭后,他再次发出警告。他说:“WeWork的破产只是僵尸公司崩溃的开始。投资者需要关注那些真正盈利并拥有可行商业模式的公司。烧钱不是一种商业模式。”

需要明确的是,大多数小盘股并不是僵尸公司,但如果熊市的预测是正确的话,那么商界的这些行尸走肉可能会在2024年拖垮同行,使小盘股的投资吸引力下降。(财富中文网)

译者:中慧言-王芳

A year ago, Wall Street was worried about inflation, “higher for longer” interest rates, and a fresh war in Europe. It was a clash of economic headwinds that was supposed to trigger a U.S. recession, leading to some bearish market outlooks from Wall Street. But while geopolitical tensions remain—and have worsened with a new conflict between Israel and Hamas—inflation is fading; the Federal Reserve is now projecting interest rate cuts; and that recession never came.

The economy’s resilience has created a few key opportunities for investors in 2024, from riding the AI hype train to playing the private credit boom. Wall Street leaders and wealth managers can’t stop talking about these new investment trends (trust me on this one). However, with the presidential election ahead, wars raging, and higher interest rates still weighing on consumers, the environment remains uncertain and risks abound.

Finance gurus’ new favorite trends could prove immensely profitable, but they all come with serious downside potential, especially if it turns out that Wall Street’s recession predictions were not wrong but simply premature. Still, for the savvy investor—or even the layperson who wants to get an inside look into the pros’ new favorite plays—it could pay to follow these trends next year.

The AI boom

The opportunity

After a year of nonstop headlines, academic papers, and Wall Street reports, most people are tired of hearing about AI. But to ignore it when discussing the key investing themes for 2024 would be impossible. Many Wall Street leaders believe AI is ushering in the fourth industrial revolution. It’s a modern-day “gold rush” for investors similar to the invention of the internet, says Wedbush top tech analyst Dan Ives.

For CFRA Research analysts Janice Quek and Angelo Zino, the main benefit in the rise of AI for investors in 2024 will be increased IT budgets as businesses spend more to create AI applications. They point to a Gartner forecast that shows IT spending will accelerate 8% year over year in 2024, with software spending jumping 13.8% amid the AI boom. That’s compared with just 3.5% growth in IT budgets this year.

Quek and Zino highlighted tech giant Microsoft, as well as software companies ServiceNow and Datadog and cybersecurity firms CrowdStrike and Palo Alto Networks, as top AI picks for 2024. These firms’ wide range of AI-enabled products and cloud-based services are well positioned to “capture” the boom in AI-related IT spending, they argued in a Thursday note.

For more top AI picks, check out Fortune’s rundown of the top stocks to buy for 2024, featuring some of Wall Street’s top investors.

The risks

There may be enough AI enthusiasm on Wall Street to fill the Grand Canyon, but the technology still has its skeptics. George Mateyo, Key Private Bank’s chief investment officer, said there’s broad consensus that AI will eventually benefit a wide range of companies, from health care and tech firms to manufacturing and financial services giants. But the crucial question is how much of AI’s potential is going to translate into earnings growth in 2024—and no one really knows the answer.

“The AI adoption cycle is really short, quite noticeably so. There’s been a more rapid adoption of AI than there was for smartphones and PCs before that,” Mateyo told Fortune. “But I do think that there might be a little bit too much optimism that this [AI-linked earnings growth] is all going to happen in 2024.”

Mateyo argued it may take a few years before the boost to worker productivity from AI improves the bottom lines of many public companies, even if the tech’s positive impact will eventually “broaden out.”

Sue Crotty, chief investment officer at Segal Marco Advisors, went a step further when detailing her views on AI. “While in the long term [AI] will be a game changer, today I think it’s a lot of hype, you can quote me on that,” she said. “AI is getting a lot of headlines, but the realities on the ground are different.”

Private credit’s glory days

The opportunity

Another key theme for 2024 is likely to be the continued rise of private credit. Higher interest rates have raised banks’ deposit costs and capital needs in recent years, leading them to lend less frequently. That’s opened the door for private lenders to fill the void for companies or real estate projects that need some cash.

The private credit market has grown into a $1.6 trillion giant over the past few years, according to data from BlackRock, Bloomberg reported. And that growth is expected to continue, with the market reaching a value of $2.8 trillion by 2028, according to a study from Preqin, or even $3.5 billion, by BlackRock’s own estimates.

Ben Miller, cofounder and CEO of alternative investment platform Fundrise, described the lure of direct lending (a.k.a. private credit) amid high interest rates. With banks tightening their lending standards, many real estate development or leasing projects are struggling to get funding. “The banks just aren’t lending. And I don’t think they’re likely to for a long time,” Miller told Fortune, arguing that a lot of banks’ assets have been “locked up” in long-term loans that were made when rates were low.

This lack of public lenders is forcing many companies and real estate projects to head to the private market, which will offer loans, but with far higher interest rates. “We focus mostly on private lending for residential apartments. And we can get a 14% interest rate for a really good property,” Miller explained. “That’s outrageously good.”

However, even Miller sees the risks in the private credit market. He argued that the real estate market may have hit its bottom with interest rates set to fall—but the rest of the economy hasn’t, and a recession is on the way.

“High interest rates won’t hit most companies, and most people, until next year and into the following year,” he warned, arguing that private lending to businesses will be riskier than lending to residential real estate projects in 2024.

The risks

The risks in private lending are definitely high. So much so that Senate Banking Committee chair Sherrod Brown (D-Ohio) sent a letter to the Fed’s vice chair for supervision Michael Barr, FDIC chairman Martin Gruenberg, and acting comptroller of the currency Michael Hsu in November, warning that the private credit market may be filled with hidden dangers. “Unlike the traditional banking industry, the private credit market is subject to minimal, indirect regulatory oversight,” the senator wrote. “The lack of transparency in this market obscures its true size and risk.”

Experts Fortune interviewed were also concerned with rising risks in the direct lending market. Rich Steinberg, chief market strategist at the Colony Group, explained that the 9% to 14% returns that private credit offers are enticing many new investors into the space, but “it’s getting more crowded.” That means anyone seeking to put money to work in private credit needs to take time to find the right opportunities and ensure the underwriting for the private loans was done with the proper due diligence by trusted lenders.

Overall, private credit “is really for more sophisticated clients that have the ability to have that as a piece of their diversified income strategy,” he told Fortune.

Certuity’s chief investment officer, Dylan Kremer, said that he also believes investors “need to pursue private credit with more diligence.”

“So much capital now is chasing into private credit that investors need to be fully aware of the [managers] and the funds that they’re using to ensure that the underwriting criteria and the structuring of the private loans are done the right way,” he said.

There are a lot of opportunities in private credit overall, according to Key Private Bank’s Mateyo, but the products are also “less transparent” and can be risky for lower-income investors. “It’s not right for everybody in the sense that it is an illiquid asset class,” he explained. “It’s not like T-bills, where you can sell them tomorrow and have the money to spend on something.”

A small-cap resurgence?

The opportunity

For investors who are convinced that Wall Street’s recession forecasts are off base, small-cap stocks may be the right opportunity next year. Small-caps have underperformed their larger peers for years, but many experts believe that will change in 2024 and beyond.

Fundstrat Global Advisors cofounder Tom Lee recently argued that the Russell 2000, which tracks small-cap stocks, could surge 50% next year as inflation returns to the Fed’s 2% target and interest rates fall. Small-caps, which typically have more debt than their larger competitors, have been hit hard by rising borrowing costs over the past few years, but that’s coming to an end, according to Lee. On top of that, small-caps are historically cheap. “On a price-to-book basis, [small-caps] are trading at where they were in 1999, relative to the S&P. And that was the start of a 12-year outperformance cycle,” Lee told CNBC.

Ronald Temple, chief market strategist at Lazard, said he, too, sees “signs of the beginning of a reversal” in the fortunes of smaller public companies. Like Lee, he noted that small-cap companies have more debt, including more floating rate debt. “Given this floating exposure, if the Fed transitions to cutting short-term rates, small-cap stocks should likely benefit more than large-caps,” he wrote in an early December note.

Temple also argued that small-cap companies offer a “compelling” value relative to large-caps, and because they generate more of their revenue in the U.S., they could benefit from the U.S. economy’s ongoing outperformance versus its developed market peers.

“Russell 2000 index constituents generate about 90% of their revenue in the United States versus around 60% to 65% of the S&P 500 index revenue,” he explained. “In our view, the domestic orientation of these companies should be a positive given the expected relative resilience of U.S. growth in 2024 and beyond.”

The risks

While small-caps could rebound in 2024, they have also underperformed large-caps this year for a reason. Some 40% of the companies in the Russell 2000 lost money in the past year, according to Lazard. And many smaller public companies still need to refinance floating rate debt that they took out when interest rates were low with today’s much higher interest rates. This combination of weak earnings and rising debt costs could be a challenge in 2024, particularly if a U.S. recession finally manifests.

Some experts even warn that many smaller U.S. companies with unprofitable business models were kept alive during the era of near-zero interest rates that came after the Global Financial Crisis, meaning that a sizable number of dead-on-their-feet firms are about to go bust. The percentage of these so-called zombie companies has grown from just over 6% of public U.S. companies in 2000 to more than 10% in 2021, according to a recent IMF study.

As Fortune previously reported, David Trainer, CEO of New Constructs, has been tracking zombie companies for years, warning that as interest rates rise, many will go bankrupt. Last month, after the collapse of WeWork (one of Trainer’s zombies), he once again issued a warning. “WeWork’s bankruptcy is just the beginning of the zombie company collapse. Investors need to focus on companies that actually make money and have viable business models,” he said. “Burning cash is not a business model.”

To be clear, most small-cap stocks are not zombies, but if the bears are right, the walking dead of the business world could pull down their peers in 2024, making small-cap stock investments less appealing.

请打开财富Plus APP