“亚洲版亚马逊”首次跻身《财富》美国500强

NICHOLAS GORDON

2023-06-09

在推销酷澎时,该公司的支持者为其冠上了下一个“亚洲版亚马逊”的名头。

文本设置

文本设置

Plus(0条)

Plus(0条)

2023年《财富》美国500强榜单按营收对美国公司进行了排名,业务主要在韩国的电子商务巨头酷澎(Coupang)以黑马之姿首次入围榜单,位列第195位。

今年酷澎之所以能首次入围《财富》美国500强,首先因为它在2022年将总部从首尔搬到了西雅图,如此一来,尽管该公司没有美国客户,但其仍有资格以美国公司的身份参与《财富》美国500强排名。据《财富》杂志统计,在上榜公司中,酷澎是在美国业务最少的两家公司之一,另一家是百胜中国(Yum China),这家快餐运营商位于德克萨斯州,在中国经营有肯德基、塔可钟和必胜客等快餐连锁店。

虽然没有为美国客户提供服务,但酷澎仍将自己视为一家美国公司。该公司首席行政官哈罗德•罗杰斯说:“本公司创始人(金范锡)是美国公民,他在美国创办了这家公司。酷澎的注册地在特拉华州,其股票在纽约证券交易所挂牌交易,并在美国等数个国家设有办事处和配送中心。

不过如果酷澎想要保住自己在美国500强中的位置,仍需保持强劲营收。虽然该公司目前仅在少数几个国家和地区(包括韩国、中国台湾和近期刚退出日本)开展业务,但其2022年营收达到了206亿美元,一举冲入200强,充分证明该公司在其服务的少数市场中占据着主导地位。

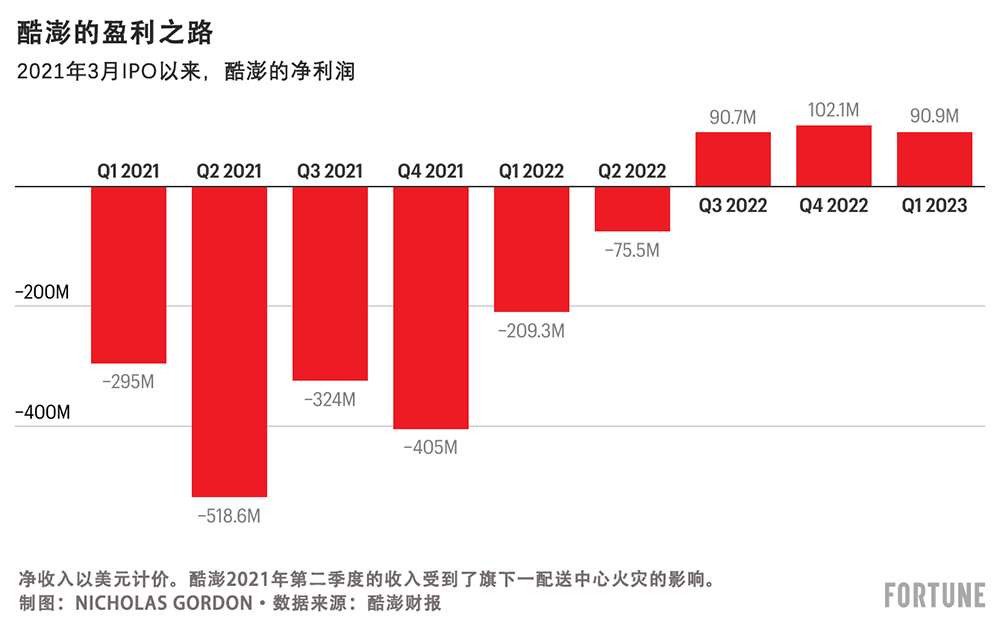

该公司近期取得的里程碑还不止于此。2022年11月,在经历多年亏损之后,酷澎首次实现季度盈利,该公司认为,之所以能取得这一成绩,首先要归功于其从零开始建立的仓储与司机网络。此后几个季度,酷澎均实现盈利,使其在反驳自己是“IPO过度炒作代表”的论调时能更有底气。

跌跌不休的股价

成立十年有余的酷澎既是科技界的宠儿,也是上市后表现令人失望的典型代表。

2010年,在从哈佛商学院辍学后,该公司首席执行官金范锡在特拉华州成立了酷澎。回到首尔后,金氏将该公司打造成了一家Groupon式的企业,并迅速转向数字零售。该公司逐步发展成为韩国主要的电商公司之一,与Naver等韩国巨头同台竞技。该公司还吸引到了斯坦利•德鲁肯米勒、比尔•阿克曼和软银愿景基金的支持。在酷澎于2021年上市之前,软银拥有该公司超过三分之一的股份。

在推销酷澎时,该公司的支持者为其冠上了下一个“亚洲版亚马逊”的名头。

在推销酷澎时,该公司的支持者为其冠上了下一个“亚洲版亚马逊”的名头。对于用户来说,该公司的吸引力来源于极为便捷的购物体验,即便在午夜时分下单,消费者依然能在第二天早上7点前收到自己购买的商品。退货也十分方便,只要将包裹放在门口让快递员取走即可。

投资者会对酷澎感兴趣,则是因为后者服务的是韩国这样一个富裕、发达且消费者习惯数字生活的经济体。在招股说明书中,酷澎援引市场研究公司欧睿(Euromonitor)的数据称,预计到2024年,韩国的零售市场规模将增长到近5400亿美元。

时任酷澎董事会成员、软银的莉迪亚·杰特在酷澎2021年3月IPO前说:“它就像是亚马逊加UPS加DoorDash加Instacart再加一点Netflix的综合体,所有这些服务都被整合到了这个极度以客户为中心的技术平台之上。”

酷澎的IPO大获成功,一共募集到了46亿美元,开盘价较发行价高出81%,交易首日,该公司的估值一度超过1000亿美元。

但这种涨势转瞬即逝。在接下来的一年里,由于投资者担心该公司在科技股普遍崩盘的情况下出现巨额亏损,酷澎的股价一路走低。股市之外该公司也是噩耗连连,不仅要面对劳工抗议,旗下一处仓库还发生了严重火灾,损失惨重。截至2022年5月,该公司股价已跌至9.35美元,较35美元的发行价已跌去73%,如果与其首日交易时的63.5美元相比,跌幅更是惨不忍睹。

目前,该公司股价较历史低点已有所回升,但速度缓慢。截至6月1日,该公司股价较去年最低点已上涨近60%,超过了15美元。不过,其目前278亿美元的市值仍仅相当于交易首日估值的约四分之一。

盈利之路

对酷澎来说,幸运的是,《财富》美国500强在评选时看的并不是公司的股价,而是营收情况。

根据酷澎的年报,在该公司2022年度的206亿美元收入中,97%来自其“产品商务”部门,其中包括零售和百货配送服务。与亚马逊类似,在销售自营商品赚取销售收入的同时,该公司也向第三方卖家提供服务,并从中赚取佣金。不过酷澎也有自己的创新,比如它还运营有送餐服务Coupang Eats和流媒体服务Coupang Play,这两项业务贡献了其2022年度剩余3%的收入。

而且酷澎的营收还在增长。该公司最近一个季度的营收为58亿美元,同比增长13%。

2022年,酷澎总体录得9200万美元的净亏损,但该公司在过去三个季度一直处于盈利状态。在最近的2023年1月至3月期间,酷澎净利润达到了9100万美元。

酷澎表示,之所以能实现盈利,主要是因为进一步提高了其花费数年时间从零打造的自营快递基础设施的运转效率。

罗杰斯说:“我们必须自己打通‘最后一公里’,这就意味着要进行大量的前期投资。”该公司曾表示,对配送基础设施的持续投入是导致其此前一直处于亏损状态的主要原因。与亚马逊或Naver依靠UPS和FedEx等第三方快递公司配送货物不同,酷澎是使用自己的车队和司机将商品送到客户手中。

罗杰斯说:“借助这种端到端物流网络,我们可以提供其他企业无法提供的服务。”

酷澎在机器人技术方面也进行了大量投资。在该公司的配送中心,随处可见的自动化车辆会将重达1000公斤的包裹送到各个分拣员手中。今年2月,该公司在接受彭博社(Bloomberg)采访时表示,自动化设备将员工的工作量减少了65%。

该公司正在努力实现业务多元化,但并非每个项目都取得了成功。该公司的流媒体视频服务面临着来自迪斯尼和Netflix等海外巨头的激烈竞争,这两家公司都在扩充其韩语产品。上季度,酷澎“新兴产品”部门(包括流媒体视频和外卖送餐)的息税折旧摊销前亏损为4700万美元。

该公司还于3月结束了其在日本为期两年的试运营,并称其希望专注于现有市场更大的增长潜力。罗杰斯说:“我们在日本和中国台湾进行了一些试点,看看哪个市场势头更好,结果发现,台湾潜力更大。”

估值过高?

一些分析师对酷澎最近的表现印象深刻,他们指出,该公司的销售增速优于韩国电商市场和零售市场的总体表现。

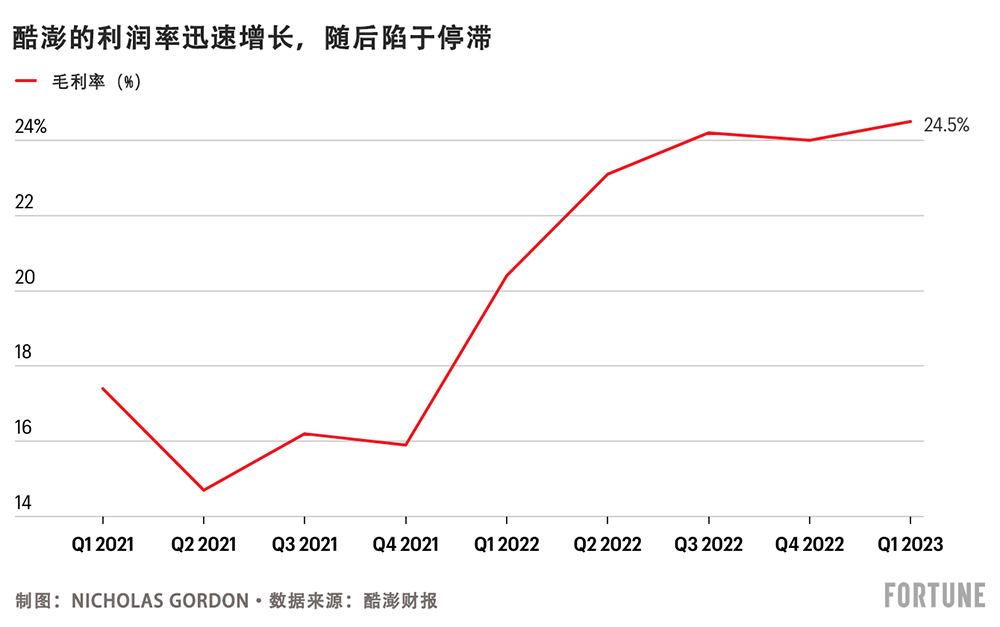

与此同时,Bernstein的韩国分析师Suh Bokyung表示,即便酷澎目前的股价远低于历史高位,但仍处于过高位置。考虑到韩国电商市场十分成熟,并且渗透率极高,酷澎在其他地区的业务又十分有限,他对酷澎能否继续维持营收增长持怀疑态度。酷澎的毛利率尤其令他感到失望,自去年11月达到24.2%后再未见多大起色。

S

uh Bokyung强调,他对酷澎的评价只针对估值,而非该公司本身。

“我很喜欢这家公司,也很欣赏他们的团队,”他说。“他们都是电商领域的专家。”

“只是估值偏高而已,”他说。(财富中文网)

译者:梁宇

审校:夏林

2023年《财富》美国500强榜单按营收对美国公司进行了排名,业务主要在韩国的电子商务巨头酷澎(Coupang)以黑马之姿首次入围榜单,位列第195位。

今年酷澎之所以能首次入围《财富》美国500强,首先因为它在2022年将总部从首尔搬到了西雅图,如此一来,尽管该公司没有美国客户,但其仍有资格以美国公司的身份参与《财富》美国500强排名。据《财富》杂志统计,在上榜公司中,酷澎是在美国业务最少的两家公司之一,另一家是百胜中国(Yum China),这家快餐运营商位于德克萨斯州,在中国经营有肯德基、塔可钟和必胜客等快餐连锁店。

虽然没有为美国客户提供服务,但酷澎仍将自己视为一家美国公司。该公司首席行政官哈罗德•罗杰斯说:“本公司创始人(金范锡)是美国公民,他在美国创办了这家公司。酷澎的注册地在特拉华州,其股票在纽约证券交易所挂牌交易,并在美国等数个国家设有办事处和配送中心。

不过如果酷澎想要保住自己在美国500强中的位置,仍需保持强劲营收。虽然该公司目前仅在少数几个国家和地区(包括韩国、中国台湾和近期刚退出日本)开展业务,但其2022年营收达到了206亿美元,一举冲入200强,充分证明该公司在其服务的少数市场中占据着主导地位。

该公司近期取得的里程碑还不止于此。2022年11月,在经历多年亏损之后,酷澎首次实现季度盈利,该公司认为,之所以能取得这一成绩,首先要归功于其从零开始建立的仓储与司机网络。此后几个季度,酷澎均实现盈利,使其在反驳自己是“IPO过度炒作代表”的论调时能更有底气。

跌跌不休的股价

成立十年有余的酷澎既是科技界的宠儿,也是上市后表现令人失望的典型代表。

2010年,在从哈佛商学院辍学后,该公司首席执行官金范锡在特拉华州成立了酷澎。回到首尔后,金氏将该公司打造成了一家Groupon式的企业,并迅速转向数字零售。该公司逐步发展成为韩国主要的电商公司之一,与Naver等韩国巨头同台竞技。该公司还吸引到了斯坦利•德鲁肯米勒、比尔•阿克曼和软银愿景基金的支持。在酷澎于2021年上市之前,软银拥有该公司超过三分之一的股份。

在推销酷澎时,该公司的支持者为其冠上了下一个“亚洲版亚马逊”的名头。

在推销酷澎时,该公司的支持者为其冠上了下一个“亚洲版亚马逊”的名头。对于用户来说,该公司的吸引力来源于极为便捷的购物体验,即便在午夜时分下单,消费者依然能在第二天早上7点前收到自己购买的商品。退货也十分方便,只要将包裹放在门口让快递员取走即可。

投资者会对酷澎感兴趣,则是因为后者服务的是韩国这样一个富裕、发达且消费者习惯数字生活的经济体。在招股说明书中,酷澎援引市场研究公司欧睿(Euromonitor)的数据称,预计到2024年,韩国的零售市场规模将增长到近5400亿美元。

时任酷澎董事会成员、软银的莉迪亚·杰特在酷澎2021年3月IPO前说:“它就像是亚马逊加UPS加DoorDash加Instacart再加一点Netflix的综合体,所有这些服务都被整合到了这个极度以客户为中心的技术平台之上。”

酷澎的IPO大获成功,一共募集到了46亿美元,开盘价较发行价高出81%,交易首日,该公司的估值一度超过1000亿美元。

但这种涨势转瞬即逝。在接下来的一年里,由于投资者担心该公司在科技股普遍崩盘的情况下出现巨额亏损,酷澎的股价一路走低。股市之外该公司也是噩耗连连,不仅要面对劳工抗议,旗下一处仓库还发生了严重火灾,损失惨重。截至2022年5月,该公司股价已跌至9.35美元,较35美元的发行价已跌去73%,如果与其首日交易时的63.5美元相比,跌幅更是惨不忍睹。

目前,该公司股价较历史低点已有所回升,但速度缓慢。截至6月1日,该公司股价较去年最低点已上涨近60%,超过了15美元。不过,其目前278亿美元的市值仍仅相当于交易首日估值的约四分之一。

盈利之路

对酷澎来说,幸运的是,《财富》美国500强在评选时看的并不是公司的股价,而是营收情况。

根据酷澎的年报,在该公司2022年度的206亿美元收入中,97%来自其“产品商务”部门,其中包括零售和百货配送服务。与亚马逊类似,在销售自营商品赚取销售收入的同时,该公司也向第三方卖家提供服务,并从中赚取佣金。不过酷澎也有自己的创新,比如它还运营有送餐服务Coupang Eats和流媒体服务Coupang Play,这两项业务贡献了其2022年度剩余3%的收入。

而且酷澎的营收还在增长。该公司最近一个季度的营收为58亿美元,同比增长13%。

2022年,酷澎总体录得9200万美元的净亏损,但该公司在过去三个季度一直处于盈利状态。在最近的2023年1月至3月期间,酷澎净利润达到了9100万美元。

酷澎表示,之所以能实现盈利,主要是因为进一步提高了其花费数年时间从零打造的自营快递基础设施的运转效率。

罗杰斯说:“我们必须自己打通‘最后一公里’,这就意味着要进行大量的前期投资。”该公司曾表示,对配送基础设施的持续投入是导致其此前一直处于亏损状态的主要原因。与亚马逊或Naver依靠UPS和FedEx等第三方快递公司配送货物不同,酷澎是使用自己的车队和司机将商品送到客户手中。

罗杰斯说:“借助这种端到端物流网络,我们可以提供其他企业无法提供的服务。”

酷澎在机器人技术方面也进行了大量投资。在该公司的配送中心,随处可见的自动化车辆会将重达1000公斤的包裹送到各个分拣员手中。今年2月,该公司在接受彭博社(Bloomberg)采访时表示,自动化设备将员工的工作量减少了65%。

该公司正在努力实现业务多元化,但并非每个项目都取得了成功。该公司的流媒体视频服务面临着来自迪斯尼和Netflix等海外巨头的激烈竞争,这两家公司都在扩充其韩语产品。上季度,酷澎“新兴产品”部门(包括流媒体视频和外卖送餐)的息税折旧摊销前亏损为4700万美元。

该公司还于3月结束了其在日本为期两年的试运营,并称其希望专注于现有市场更大的增长潜力。罗杰斯说:“我们在日本和中国台湾进行了一些试点,看看哪个市场势头更好,结果发现,台湾潜力更大。”

估值过高?

一些分析师对酷澎最近的表现印象深刻,他们指出,该公司的销售增速优于韩国电商市场和零售市场的总体表现。

与此同时,Bernstein的韩国分析师Suh Bokyung表示,即便酷澎目前的股价远低于历史高位,但仍处于过高位置。考虑到韩国电商市场十分成熟,并且渗透率极高,酷澎在其他地区的业务又十分有限,他对酷澎能否继续维持营收增长持怀疑态度。酷澎的毛利率尤其令他感到失望,自去年11月达到24.2%后再未见多大起色。

Suh Bokyung强调,他对酷澎的评价只针对估值,而非该公司本身。

“我很喜欢这家公司,也很欣赏他们的团队,”他说。“他们都是电商领域的专家。”

“只是估值偏高而已,”他说。(财富中文网)

译者:梁宇

审校:夏林

The 2023 Fortune 500 list, ranking U.S.-based companies by revenue, features a surprising newcomer at No. 195: Coupang, an e-commerce giant that conducts most of its business in South Korea.

Coupang’s landing on the Fortune 500 for the first time this year is partly the result of its moving headquarters from Seoul to Seattle in 2022, thus qualifying it as a U.S. company for the purposes of Fortune’s ranking despite its having no U.S. customers. By Fortune’s reckoning, Coupang is one of two companies with minimal U.S. business; the other is Yum China, the Texas-based fast food operator that runs KFC, Taco Bell, and Pizza Hut in China.

Despite not serving U.S. customers, Coupang sees itself as a U.S. company. “Our founder [Bom Kim] is a U.S. citizen, and started the company in the U.S.,” says Harold Rogers, the company’s chief administrative officer. Coupang is incorporated in Delaware, its shares trade on the New York Stock Exchange, and it has offices and fulfillment centers in several countries, including the U.S.

Still, Coupang also needed robust revenue to secure a spot on the Fortune 500. And despite its limited geographic footprint—it only does business in South Korea, Taiwan, and, until recently, Japan—it generated $20.6 billion in revenue last year and cracked the Fortune 200, a testament to its dominance in the few markets it serves.

Coupang’s debut on the Fortune 500 isn’t its only milestone of late. Last November, the company reported its first quarterly net profit after years of losses, a feat it attributes to the network of warehouses and drivers it built from scratch. The firm has reported profits in every quarter since then, a streak that has helped Coupang combat its recent reputation as a victim of IPO overhype.

Coupang stock slump

Since its founding over a decade ago, Coupang has managed to be both a darling of the tech sector and poster child of disappointing post-IPO performance.

CEO Bom Kim founded Coupang, incorporating it in Delaware in 2010, after dropping out of Harvard Business School. Returning to Seoul, Kim set up the business as a Groupon-style service, before quickly pivoting to digital retail. The company grew to become one of South Korea’s key e-commerce companies, competing with giants like South Korea–based Naver. The firm attracted backers such as Stanley Druckenmiller and Bill Ackman, as well as SoftBank’s Vision Fund. Before Coupang’s IPO in 2021, SoftBank owned over a third of the company.

The firm’s boosters sold Coupang as the next “Amazon of Asia.” The startup lured users with its extreme convenience; customers can order goods as late as midnight and still have them delivered before seven the next morning. Users can also return goods easily, leaving packages on their doorstep for delivery drivers to retrieve.

Investors were attracted as well to Coupang’s presence in the wealthy, developed economy of South Korea and its digitally connected consumers. In its prospectus, Coupang projected the country’s retail market would grow to nearly $540 billion by 2024, citing data from market research firm Euromonitor.

“It is Amazon with a UPS attached to it; with DoorDash, with Instacart, with a little dash of Netflix, and that is all integrated on this technology platform with an extreme degree of customer-centricity,” said SoftBank’s Lydia Jett, then one of Coupang’s board members, before the company’s IPO in March 2021.

The IPO was a bonanza. Coupang raised $4.6 billion, and shares opened 81% above their offer price, at one point valuing the company at more than $100 billion on its first day of trading.

The rally was short-lived. Coupang’s share price declined steadily over the following year, as investors worried about the company’s giant losses amid a broader collapse in tech stocks. Other bad news included labor protests and a deadly—and expensive—fire at one of Coupang’s warehouses. By May 2022, shares had fallen to just $9.35, 73% below the offer price of $35 and even further off its trading debut of $63.50.

Shares have recovered from those lows, albeit slowly; they have risen almost 60% from the lowest point last year, hitting over $15 as of June 1. Still, the company’s current market cap of $27.8 billion is roughly a quarter of the valuation it hit on its first trading day.

Path to profitability

Luckily for Coupang, the Fortune 500 doesn’t take into account seesawing stock prices. Rather, the list ranks companies by the revenue they generate.

According to the company’s annual report, 97% of Coupang’s 2022 revenue of $20.6 billion came from its “product commerce” division, which includes retail and grocery delivery services. The e-commerce firm earns sales from its own stock of goods, and pockets a fee from third-party sellers, similar to Amazon. Coupang’s newer initiatives, like meal delivery service Coupang Eats and streaming service Coupang Play, generated the remainder of its 2022 revenue.

And Coupang’s revenue is growing. The company reported $5.8 billion in revenue for the most recent quarter, up 13% year on year.

Coupang recorded a net loss of $92 million in 2022 overall, but the company has been in the black for the past three quarters. Most recently, it earned $91 million in net income in the January to March 2023 period.

Coupang attributes this newfound profitability to squeezing greater efficiencies from its proprietary delivery infrastructure, which it spent years building from the ground up.

“We had to build that last mile ourselves, which meant a lot of upfront investment,” says Rogers. The company had blamed previous losses on its continued investment in delivery infrastructure. Unlike Amazon or Naver, which rely on third parties like UPS and FedEx to deliver goods, Coupang uses its own fleet of trucks and drivers to get orders to customers.

“The way we’ve built that end-to-end logistics network, we can do things that no other company, at scale, can do,” Rogers says.

Coupang has invested heavily in robotics. Automated vehicles move through the company’s fulfillment centers to deliver 1,000-kilogram packages to sorters. The company told Bloomberg in February that automation had cut the workload for its human workers by 65%.

The company is trying to diversify its business, but not every initiative has panned out. The company’s streaming video service faces stiff competition from foreign giants like Disney and Netflix, both of which are expanding their Korean-language offerings. Coupang’s “developing offerings” segment, which includes streaming video and meal delivery, reported a $47 million loss before interest, taxes, depreciation, and amortization last quarter.

The company also ended its two-year trial run in Japan in March, saying it wanted to focus on the greater potential for growth in existing markets. “We started both Japan and Taiwan as these small experiments to see which market would gain traction,” Rogers says. “We saw a much bigger opportunity in Taiwan.”

Overvalued?

Some analysts are impressed with Coupang’s recent performance, noting that its sales growth is outperforming both the Korean e-commerce market and the country’s retail market in general.

Suh Bokyung, a Korea analyst for Bernstein, meanwhile, says Coupang’s stock is too high even though it remains well below its post-IPO peak. He’s skeptical that Coupang can record more revenue growth, given South Korea’s well-developed and highly penetrated e-commerce market and Coupang’s limited business elsewhere. He’s especially discouraged by Coupang’s gross profit margins, which have essentially flatlined since reaching 24.2% last November.

Suh stresses that his judgment of Coupang is based purely on its valuation, and not the company as a business.

“I like the company. I like the team,” he says. “They understand the e-commerce business.”

“It’s just overvalued,” he says.

请打开财富Plus APP