2023,现金为王?

Lucy Brewster

2023-05-01

此刻是否应该撤出低迷的股市,持币观望?专家们给出建议。

文本设置

文本设置

Plus(0条)

Plus(0条)

现金为王的情况再次出现。

标准普尔500指数(S&P 500)近期收益低迷,而利率却使储蓄账户的收益率达到惊人的5%,因此有投资者开始思考,他们是否应该彻底逃离不稳定的股票市场,选择投资可靠但可能有些乏味的另外一类产品:现金。美国银行(Bank of America)的分析师在一份客户研究报告中预测标准普尔500指数近期的收益率会令人失望。他们表示,现金是“具有吸引力的标准普尔500指数替代选择”。安联(Allianz)最近的一份研究报告显示,62%的美国受访者称宁愿持有现金,也不愿意承受股市风暴的冲击。最近发生的银行倒闭也促使投资者,将资金转移到更保守但低风险的账户和基金。美国银行最近的全球研究报告称,仅2023年第一季度,投资者将5,080亿美元投入货币市场基金。货币市场基金是存放现金的理想选择,而且能够带来高收益。

问题是:在市场风暴结束之前,你是否应该将大量或大部分投资转移到现金投资?理财顾问和投资分析师给出了否定回答。申克曼财富管理公司(Shenkman Wealth Management)的乔纳森·申克曼解释称:“向高收益率的大额存单、货币市场基金或国债等配置更多资金,看起来是谨慎的做法;然而,这是一种市场择机行为,应该避免。”Univest Wealth下属部门Girard的理财顾问兼投资总监马克·N·巴尔塞指出:“从长远来看,现金并非没有风险。”他解释道,现金投资无法跑赢通胀的风险极高,就像在错误的时机进行再投资的风险一样。巴尔塞表示:“投资者说:‘当情况很糟糕的时候,我会把现金投入高收益的货币市场,在一切风平浪静之后,我们会重新回到股票市场。’问题是,等到一切风平浪静的时候,市场已经发生了变化。”

美国银行依旧预测未来十年,标准普尔500指数有7%的年收益率。在设计投资策略以充分利用现金时,关键是要考虑自己的投资期限和长期财务目标。Facet Wealth的理财顾问布伦特·韦斯说:“不要追逐利率,要坚持自己的计划。”申克曼表示:“从长远来看,股市将跑赢债市,而债市将跑赢货币市场。”

然而,如果你在近期内有消费需求,或者只想将部分储蓄投入到较为安全的产品,个人理财专家支持以下投资策略。

寻找高收益产品

理财顾问强调,最简单、最有效的利用高利率的途径之一是,保证将应急资金存入高收益储蓄账户。网站Bankrate的理财顾问格雷戈·麦克布赖德说:“弹性增贷确实扩大了许多银行的存款收益率和大银行存款收益率之间的差异,作为储户,你可以将其作为优势加以利用。”虽然许多大型传统金融机构依旧为储户提供约1%的年化收益率,但一些在线银行为高收益账户提供的收益率高达4%。韦斯解释称,一些在线经纪机构,例如Ally和UFB银行等,提供最有竞争力的年化收益率。

如果最近的银行倒闭令你感到焦虑,只要你存款的银行有联邦保险,你的存款最高达到25万美元就是安全的。如果你的存款金额超过25万美元,理财顾问就建议在不同银行开立账户,让存款金额低于该限额,或者在同一个银行不同所有权类型下开立账户。韦斯还解释称,他通常建议客户在至少两家不同银行开立账户,尤其是存款金额超过美国联邦存款保险公司(FDIC)25万美元保险限额的客户。韦斯解释称:“如果一家银行出现一些问题,你在另外一家银行就还有资金可用。”

考虑建立大额存单阶梯

大额存单(CD)是在指定期限内获得利息的定期存款。大额存单阶梯是一种储蓄策略,即按照不同到期时间购买多份大额存单,形成可以带来交错收益的“阶梯”。

麦克布赖德说:“如果你在未来的确定时间点有特定现金需求,大额存单就是很好的选择。如果你期待获得能够预测的利息收入流,或者希望将投资组合多样化,通过现金配置获得最高收益同时避免承担任何风险,[这就是最好的选择]。”大额存单阶梯适合在退休期间想要获得稳定收入的投资者。如果你知道未来会有固定支出,比如支付学费或买车,大额存单阶梯就能够帮助你充分利用利率。与高收益储蓄账户一样,不同金融机构提供不同的利率,你可以通过对比找到最适合你的一家。

为了建立大额存单阶梯,你可以购买一系列在不同时间连续到期的大额存单。如果你有2,500美元,就能够投资五份大额存单,期限从一年到五年不等。第一份大额存单到期后,如果你想延续大额存单阶梯,你就能够取现,并按照你预期的期限再投资新的大额存单。

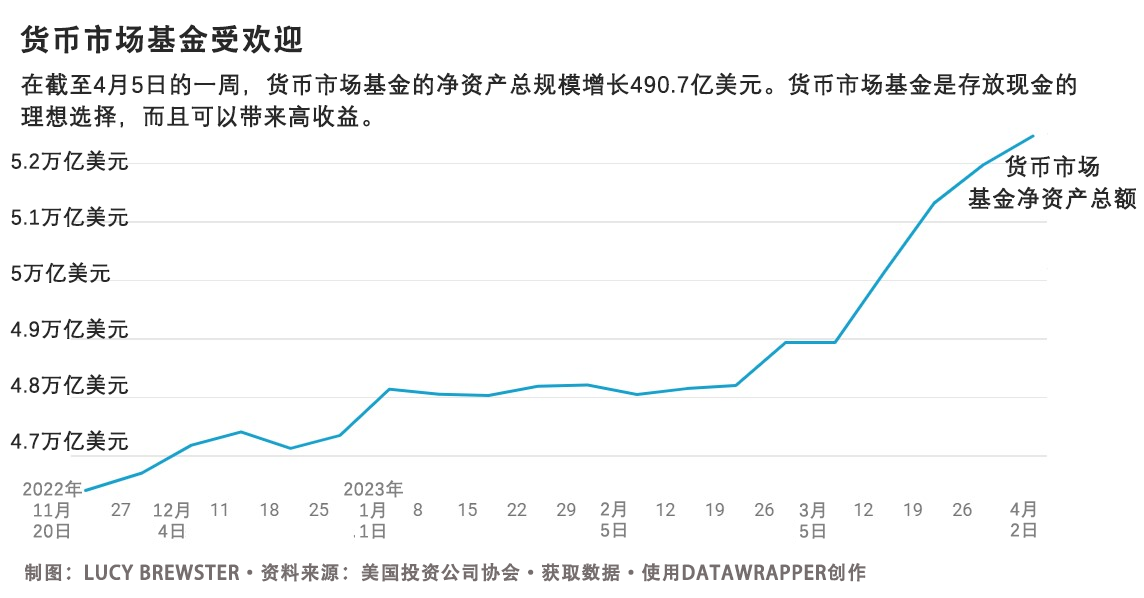

货币市场基金是一种很受欢迎的选择

另外一种引起大量投资者关注的选择是货币市场共同基金。这些共同基金的特殊性在于,他们投资具有流动性的短期资产,包括现金、基于债务的短期证券等。美国投资公司协会(Investment Company Institute)的数据显示,截至4月5日的一周,货币市场基金的总资产增长了400.7亿美元,使货币市场基金的资产总额达到5.25万亿美元。

申克曼表示:“这些基金的利率通常高于支票或储蓄账户。”他补充道:“虽然许多货币市场基金没有美国联邦存款保险公司的保险,但投资者遭受损失的风险微乎其微,因为这些基金投资最高质量的债券,这些债券的期限非常短。”

麦克布赖德称,他建议客户将计划投资的基金投入这些基金。他说:“如果你想开立经纪账户,并且你想立刻投资手头的资金,货币基金就是理想选择,你可以将货币市场基金作为出售一项投资和买入另外一项投资期间的临时选择。”

投资短期债券基金

短期债券基金是相对低风险的投资选择,适合希望从更高收益率中获利的投资者。短期债券基金以投资企业债券和其他投资级证券为主。申克曼解释称:“如果投资者的投资期限相对更长,而且愿意忍受投资项目的小幅波动,那么短期债券基金就是最佳选择。”

然而,即使相对低风险的投资,其风险也高于将钱存入现金账户的风险。投资者不应该将他们可能随时需要动用的资金,投入任何类型的股票或债券基金。申克曼补充道:“虽然这些基金依旧安全,但重要的是,投资者需要牢记它们不是货币市场账户的替代品,因为现金价值会出现波动,尤其是在利率上浮时期。”

风险越高,回报越高

重要的是,虽然在当前的市场环境下,精明地进行投资可以带来高收益,但这些账户依旧无法跑赢通胀。如果你要针对退休等长期目标进行投资,就永远不要用现金账户取代一种投资策略。

韦斯说:“有些人很胆小,他们会想‘你知道吗,或许我该等等再进行投资’,因此我要再次重申这一点:大额存单阶梯[或其他现金账户]不应该成为长期投资或财富累积策略的替代品。因此,如果你对投资感到紧张,就一定保证用于投资的资金在未来5年至10年不会动用。”

虽然目前股票市场动荡,但经验丰富的投资者有一种理念很有道理:不要因为害怕动荡的市场环境,而看不到长期收益。(财富中文网)

译者:刘进龙

审校:汪皓

现金为王的情况再次出现。

标准普尔500指数(S&P 500)近期收益低迷,而利率却使储蓄账户的收益率达到惊人的5%,因此有投资者开始思考,他们是否应该彻底逃离不稳定的股票市场,选择投资可靠但可能有些乏味的另外一类产品:现金。美国银行(Bank of America)的分析师在一份客户研究报告中预测标准普尔500指数近期的收益率会令人失望。他们表示,现金是“具有吸引力的标准普尔500指数替代选择”。安联(Allianz)最近的一份研究报告显示,62%的美国受访者称宁愿持有现金,也不愿意承受股市风暴的冲击。最近发生的银行倒闭也促使投资者,将资金转移到更保守但低风险的账户和基金。美国银行最近的全球研究报告称,仅2023年第一季度,投资者将5,080亿美元投入货币市场基金。货币市场基金是存放现金的理想选择,而且能够带来高收益。

问题是:在市场风暴结束之前,你是否应该将大量或大部分投资转移到现金投资?理财顾问和投资分析师给出了否定回答。申克曼财富管理公司(Shenkman Wealth Management)的乔纳森·申克曼解释称:“向高收益率的大额存单、货币市场基金或国债等配置更多资金,看起来是谨慎的做法;然而,这是一种市场择机行为,应该避免。”Univest Wealth下属部门Girard的理财顾问兼投资总监马克·N·巴尔塞指出:“从长远来看,现金并非没有风险。”他解释道,现金投资无法跑赢通胀的风险极高,就像在错误的时机进行再投资的风险一样。巴尔塞表示:“投资者说:‘当情况很糟糕的时候,我会把现金投入高收益的货币市场,在一切风平浪静之后,我们会重新回到股票市场。’问题是,等到一切风平浪静的时候,市场已经发生了变化。”

美国银行依旧预测未来十年,标准普尔500指数有7%的年收益率。在设计投资策略以充分利用现金时,关键是要考虑自己的投资期限和长期财务目标。Facet Wealth的理财顾问布伦特·韦斯说:“不要追逐利率,要坚持自己的计划。”申克曼表示:“从长远来看,股市将跑赢债市,而债市将跑赢货币市场。”

然而,如果你在近期内有消费需求,或者只想将部分储蓄投入到较为安全的产品,个人理财专家支持以下投资策略。

寻找高收益产品

理财顾问强调,最简单、最有效的利用高利率的途径之一是,保证将应急资金存入高收益储蓄账户。网站Bankrate的理财顾问格雷戈·麦克布赖德说:“弹性增贷确实扩大了许多银行的存款收益率和大银行存款收益率之间的差异,作为储户,你可以将其作为优势加以利用。”虽然许多大型传统金融机构依旧为储户提供约1%的年化收益率,但一些在线银行为高收益账户提供的收益率高达4%。韦斯解释称,一些在线经纪机构,例如Ally和UFB银行等,提供最有竞争力的年化收益率。

如果最近的银行倒闭令你感到焦虑,只要你存款的银行有联邦保险,你的存款最高达到25万美元就是安全的。如果你的存款金额超过25万美元,理财顾问就建议在不同银行开立账户,让存款金额低于该限额,或者在同一个银行不同所有权类型下开立账户。韦斯还解释称,他通常建议客户在至少两家不同银行开立账户,尤其是存款金额超过美国联邦存款保险公司(FDIC)25万美元保险限额的客户。韦斯解释称:“如果一家银行出现一些问题,你在另外一家银行就还有资金可用。”

考虑建立大额存单阶梯

大额存单(CD)是在指定期限内获得利息的定期存款。大额存单阶梯是一种储蓄策略,即按照不同到期时间购买多份大额存单,形成可以带来交错收益的“阶梯”。

麦克布赖德说:“如果你在未来的确定时间点有特定现金需求,大额存单就是很好的选择。如果你期待获得能够预测的利息收入流,或者希望将投资组合多样化,通过现金配置获得最高收益同时避免承担任何风险,[这就是最好的选择]。”大额存单阶梯适合在退休期间想要获得稳定收入的投资者。如果你知道未来会有固定支出,比如支付学费或买车,大额存单阶梯就能够帮助你充分利用利率。与高收益储蓄账户一样,不同金融机构提供不同的利率,你可以通过对比找到最适合你的一家。

为了建立大额存单阶梯,你可以购买一系列在不同时间连续到期的大额存单。如果你有2,500美元,就能够投资五份大额存单,期限从一年到五年不等。第一份大额存单到期后,如果你想延续大额存单阶梯,你就能够取现,并按照你预期的期限再投资新的大额存单。

货币市场基金是一种很受欢迎的选择

另外一种引起大量投资者关注的选择是货币市场共同基金。这些共同基金的特殊性在于,他们投资具有流动性的短期资产,包括现金、基于债务的短期证券等。美国投资公司协会(Investment Company Institute)的数据显示,截至4月5日的一周,货币市场基金的总资产增长了400.7亿美元,使货币市场基金的资产总额达到5.25万亿美元。

申克曼表示:“这些基金的利率通常高于支票或储蓄账户。”他补充道:“虽然许多货币市场基金没有美国联邦存款保险公司的保险,但投资者遭受损失的风险微乎其微,因为这些基金投资最高质量的债券,这些债券的期限非常短。”

麦克布赖德称,他建议客户将计划投资的基金投入这些基金。他说:“如果你想开立经纪账户,并且你想立刻投资手头的资金,货币基金就是理想选择,你可以将货币市场基金作为出售一项投资和买入另外一项投资期间的临时选择。”

投资短期债券基金

短期债券基金是相对低风险的投资选择,适合希望从更高收益率中获利的投资者。短期债券基金以投资企业债券和其他投资级证券为主。申克曼解释称:“如果投资者的投资期限相对更长,而且愿意忍受投资项目的小幅波动,那么短期债券基金就是最佳选择。”

然而,即使相对低风险的投资,其风险也高于将钱存入现金账户的风险。投资者不应该将他们可能随时需要动用的资金,投入任何类型的股票或债券基金。申克曼补充道:“虽然这些基金依旧安全,但重要的是,投资者需要牢记它们不是货币市场账户的替代品,因为现金价值会出现波动,尤其是在利率上浮时期。”

风险越高,回报越高

重要的是,虽然在当前的市场环境下,精明地进行投资可以带来高收益,但这些账户依旧无法跑赢通胀。如果你要针对退休等长期目标进行投资,就永远不要用现金账户取代一种投资策略。

韦斯说:“有些人很胆小,他们会想‘你知道吗,或许我该等等再进行投资’,因此我要再次重申这一点:大额存单阶梯[或其他现金账户]不应该成为长期投资或财富累积策略的替代品。因此,如果你对投资感到紧张,就一定保证用于投资的资金在未来5年至10年不会动用。”

虽然目前股票市场动荡,但经验丰富的投资者有一种理念很有道理:不要因为害怕动荡的市场环境,而看不到长期收益。(财富中文网)

译者:刘进龙

审校:汪皓

Cash is king again.

When near-term returns for the S&P 500 look bleak and interest rates push yields from savings accounts up to an eye-popping 5%, some investors are asking themselves if they should ditch the erratic equities market altogether for its reliable, if not boring, cousin: cash. Cash is a “compelling alternative to the S&P 500,” Bank of America analysts wrote in a research note to clients, predicting disappointing near-term returns for the S&P 500. According to a recent Allianz research report, 62% of Americans surveyed said they would rather keep their money in cash than weather the market storm. Recent bank failures have also caused investors to move their money to more conservative, low-risk accounts and funds. In the first quarter of 2023 alone, investors moved $508 billion into money market funds, a high-yielding place to store cash, according to Bank of America’s most recent global research report.

So the question is: Should you move a significant amount, or the majority, of your investments into cash until the market storm is over? The answer is no, according to advisors and investment analysts. “Allocating more funds to high-yielding CDs, money market funds, or treasuries may seem prudent; however, this is a form of market timing and should be avoided,” explained Jonathan Shenkman of Shenkman Wealth Management. “Long term, cash is not risk-free,” explained Marc N. Balcer, financial advisor and investment director at Girard, a Univest Wealth Division. He explained that the risk of your cash being outpaced by inflation is significant, as is the risk of reinvesting at the wrong time. “Investors say, ‘I’ll put cash into this high-yield money market while things are scary and then when things calm down, I’ll move it back into the market,’ and the problem with that is that by the time things calm down, the market will have already moved,” said Balcer.

Bank of America still predicts a 7% annual return for the S&P 500 over the next decade. When designing a strategy to make the most of your cash, it’s important to take into account your time horizon and long-term financial goals. “Don’t just chase the rates, follow your plan,” explained Brent Weiss, a financial advisor at Facet Wealth. “Over the long term, stocks will outpace bonds and bonds will outpace cash,” added Shenkman.

However, if you have money you’ll need to spend in the near term, or just want to park a portion of your savings in something safe, here are a few strategies that personal finance experts do endorse.

Search for high yields

Advisors emphasized that one of the simplest and most effective ways to take advantage of high interest rates is to make sure your emergency fund is in a high-yield savings account. “The accordion has certainly expanded the difference between what a lot of banks are paying and what the top banks are paying, and as a saver, you can exploit that to your advantage,” said Greg McBride, financial advisor at Bankrate. While many large traditional financial institutions still offer savers APYs of about 1%, some online banks offer yields of up to 4% for their high-yield accounts. Weiss explained that some online brokerages, such as Ally bank and UFB bank, offer the most competitive APYs.

If you feel anxious about the recent bank failures, know that as long as you are at a bank that is federally insured, your money is safe up to $250,000. If you have more than that amount in a bank account, advisors recommend opening accounts at different banks to stay under the limit or opening accounts under different ownership categories at the same bank. Weiss also explained that he usually recommends clients have accounts with at least two different banks, especially if they are saving more than the FDIC-insured $250,000. “If one bank has some issues, you have another bank with cash available,” Weiss explained.

Consider building a CD ladder

Certificates of deposit (CDs) are fixed deposits that earn interest over a designated period. A CD ladder is a savings strategy in which you stack multiple certificates of deposit (CDs) that all mature at different times to create a “ladder” of staggered returns.

“CDs are a great option if you have a specific cash need at a known point in the future,” explained McBride. “[They work best] if you are looking to generate a predictable stream of interest income or you’re looking to diversify your portfolio positioning cash allocation to get the best return without taking any risk,” McBride. CD ladders can be great for those who want a steady income during retirement. If you know you’re going to have a fixed expense in the future, like a tuition payment or car purchase, CD ladders can help you make the most of the rates. Similar to high-yield savings accounts, different financial institutions offer different rates and you can compare to find the one that makes the most sense for you.

To build your own CD ladder, you can buy a string of CDs that all expire at different times, but in succession. If you have $2,500 to invest, you could invest in five CDs that range from one-year to five-year CDs. When the first CD matures, you can cash it out and reinvest the money in a new CD that matures however many years away you want to continue the ladder.

Money market funds are a popular option

Another option that has gotten a lot of attention from investors is money market mutual funds. These mutual funds are unique in that they invest in liquid, short-term assets including cash, and debt-based securities with near-term maturities. According to data from the Investment Company Institute, total money market fund assets went up by $40.07 billion for the week of April 5, making the new total $5.25 trillion in money market fund assets.

“These funds typically earn a higher interest rate than a checking or savings account,” explained Shenkman. “While many money market funds are not FDIC-insured, the risk of investors losing money is minuscule since they invest in the highest-quality bonds with an extremely short duration,” he added.

McBride explained that he advises clients to use these funds for money that you may be planning to invest. “Money funds are a great option for your brokerage account and the money that you want to be able to invest at a moment’s notice, using the money market fund as your temporary parking between selling one investment and buying another,” said McBride.

Invest in short-duration bond funds

Short-term bond funds are relatively low-risk investment options for those who want to benefit from higher yields. Short-term bond funds invest in mostly corporate bonds and other investment-grade securities. “For investors who have a slightly longer time horizon and are willing to endure some slight fluctuation in their holdings, short-duration bond funds are a wonderful option,” explained Shenkman.

However, even relatively low-risk investments carry more risk than having your money in cash accounts. Investors should not put the cash that they might need readily available in any kind of equity or bond fund. “While these funds still provide safety, it’s important to keep in mind that they are not a substitute for money market accounts since cash will fluctuate in value, especially as interest rates increase,” added Shenkman.

With higher risk comes higher returns

It’s important to keep in mind that while being savvy with your cash can get you high returns given the current market environment, these accounts still don’t outpace inflation. You should never substitute a cash account for an investment strategy, especially for long-term goals such as retirement.

“Some people are skittish and say, 'You know what, maybe I'll just wait on investing,’ so I want to reiterate this point: What a CD ladder [or another cash account] shouldn't be is an alternative to a longer-term investment or wealth-building strategy,” explained Weiss. “So if you're nervous about investing, make sure you’re investing money you don’t need to touch for the next five to 10 years.”

While the equity market is rocky now, the sage wisdom of seasoned investors is true: Don't let tumultuous market conditions scare you away from seeing long-term returns.

请打开财富Plus APP