美联储承认,房价大幅下跌是可能的

LANCE LAMBERT

2022-10-10

实际上,在美联储承认房价可能下跌之前,很多市场的房价已经开始下跌。

文本设置

文本设置

Plus(0条)

Plus(0条)

美联储主席杰罗姆·鲍威尔(Jerome Powell)在9月份的联邦公开市场委员会新闻发布会上被要求澄清他在几个月前说美国房地产市场将经历"重启"的含义。他的回答是什么呢?我们已经进入了一个“艰难的[房产]修正时期”,将看到美国房地产市场过渡到供求都更“平衡”的时期。

然而,鲍威尔仍然没有回应这一棘手问题:美国房价会下跌吗?

快进到本周,我们终于更好地了解了美联储对房价的看法。周四,美联储理事克里斯托弗·沃勒(Christopher Waller)在肯塔基大学对听众表示,美国房价有可能出现“大幅”下跌。

沃勒对听众说:“虽然这次(房地产)市场修正可能相当温和,但我不能排除在市场恢复正常之前,需求和房价出现更大幅度下跌的可能性。”

这是美联储官员首次承认,正在进行的楼市修正可能导致全美房价下跌。沃勒还承认,房价修正最终可能不仅仅是小幅下跌。他说,这可能是一次“大幅[房价]修正”。

“尽管房价有大幅回调的风险,但有几个因素有助于减轻我对这种回调会引发一波抵押贷款违约潮并可能破坏金融体系稳定的担忧。”沃勒说。“一是由于21世纪10年代抵押贷款承销相对紧缩,如今抵押贷款借款人的信用评分普遍高于上次住房修正之前的水平。此外,上一次修正的经验告诉我们,大多数借款人只有在他们的收入受到负面冲击,以及抵押贷款资不抵债时才会违约。”

就言外之意而言,沃勒的表述似乎有四层含义:1. 房地产市场的修正可能是“温和的”;2. 有一种情况是,房地产市场的修正并不温和;3. 房价大幅下跌是有可能出现的;4. 如果房价大幅下跌,也不会引发2008年那样的止赎潮或金融崩溃。

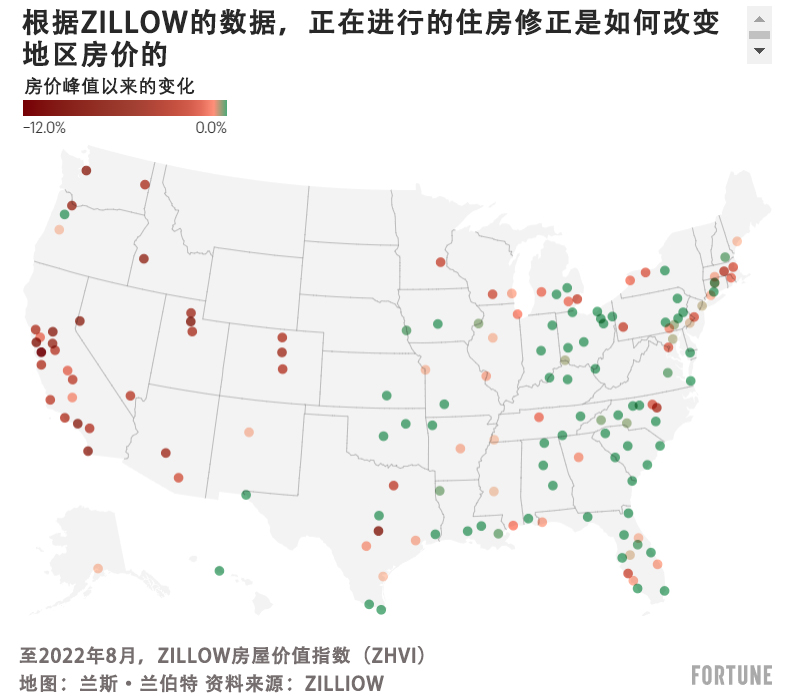

当然,在美联储承认房价可能下跌之前,很多市场的房价已经开始下跌。在约翰伯恩斯房地产咨询公司(John Burns Real Estate Consulting)追踪的148个主要地区房地产市场中,98个市场的房屋价值已从2022年的峰值下跌。在11个市场中,伯恩斯房屋价值指数跌幅已经超过5%。

“美国一些地区的房价甚至已经出现了下跌,尤其是那些在过去两年中房价涨幅最大的地区。据报道,许多建筑商正在降低标价,并提供更大的优惠力度。”沃勒告诉听众。

到目前为止,由抵押贷款利率飙升推动的房地产市场修正对以下两组市场中的一组打击最为严重。

第一组是高成本的科技中心。其中包括旧金山(较2022年的峰值下跌7.8%)、圣何塞(较2022年的峰值下跌9%)和西雅图(较2022年的峰值下跌6.2%)等市场。不仅高端房地产市场对利率更加敏感,科技领域亦是如此。

另一组是奥斯汀(较2022年的峰值下跌6.2%)、博伊西(较2022年的峰值下跌5.3%)和凤凰城(较2022年的峰值下跌4.4%)等泡沫市场。在疫情期间的房地产热潮中,这些泡沫市场的房价远超历史上当地居民收入可以承受的范围。根据穆迪分析公司的数据,奥斯汀和凤凰城的房价分别被“高估”了61%和57%。从历史上看,严重“高估”的房地产市场在房地产市场修正期间最易受到房价下跌的影响。(财富中文网)

译者:中慧言-王芳

美联储主席杰罗姆·鲍威尔(Jerome Powell)在9月份的联邦公开市场委员会新闻发布会上被要求澄清他在几个月前说美国房地产市场将经历"重启"的含义。他的回答是什么呢?我们已经进入了一个“艰难的[房产]修正时期”,将看到美国房地产市场过渡到供求都更“平衡”的时期。

然而,鲍威尔仍然没有回应这一棘手问题:美国房价会下跌吗?

快进到本周,我们终于更好地了解了美联储对房价的看法。周四,美联储理事克里斯托弗·沃勒(Christopher Waller)在肯塔基大学对听众表示,美国房价有可能出现“大幅”下跌。

沃勒对听众说:“虽然这次(房地产)市场修正可能相当温和,但我不能排除在市场恢复正常之前,需求和房价出现更大幅度下跌的可能性。”

这是美联储官员首次承认,正在进行的楼市修正可能导致全美房价下跌。沃勒还承认,房价修正最终可能不仅仅是小幅下跌。他说,这可能是一次“大幅[房价]修正”。

“尽管房价有大幅回调的风险,但有几个因素有助于减轻我对这种回调会引发一波抵押贷款违约潮并可能破坏金融体系稳定的担忧。”沃勒说。“一是由于21世纪10年代抵押贷款承销相对紧缩,如今抵押贷款借款人的信用评分普遍高于上次住房修正之前的水平。此外,上一次修正的经验告诉我们,大多数借款人只有在他们的收入受到负面冲击,以及抵押贷款资不抵债时才会违约。”

就言外之意而言,沃勒的表述似乎有四层含义:1. 房地产市场的修正可能是“温和的”;2. 有一种情况是,房地产市场的修正并不温和;3. 房价大幅下跌是有可能出现的;4. 如果房价大幅下跌,也不会引发2008年那样的止赎潮或金融崩溃。

当然,在美联储承认房价可能下跌之前,很多市场的房价已经开始下跌。在约翰伯恩斯房地产咨询公司(John Burns Real Estate Consulting)追踪的148个主要地区房地产市场中,98个市场的房屋价值已从2022年的峰值下跌。在11个市场中,伯恩斯房屋价值指数跌幅已经超过5%。

“美国一些地区的房价甚至已经出现了下跌,尤其是那些在过去两年中房价涨幅最大的地区。据报道,许多建筑商正在降低标价,并提供更大的优惠力度。”沃勒告诉听众。

到目前为止,由抵押贷款利率飙升推动的房地产市场修正对以下两组市场中的一组打击最为严重。

第一组是高成本的科技中心。其中包括旧金山(较2022年的峰值下跌7.8%)、圣何塞(较2022年的峰值下跌9%)和西雅图(较2022年的峰值下跌6.2%)等市场。不仅高端房地产市场对利率更加敏感,科技领域亦是如此。

另一组是奥斯汀(较2022年的峰值下跌6.2%)、博伊西(较2022年的峰值下跌5.3%)和凤凰城(较2022年的峰值下跌4.4%)等泡沫市场。在疫情期间的房地产热潮中,这些泡沫市场的房价远超历史上当地居民收入可以承受的范围。根据穆迪分析公司的数据,奥斯汀和凤凰城的房价分别被“高估”了61%和57%。从历史上看,严重“高估”的房地产市场在房地产市场修正期间最易受到房价下跌的影响。(财富中文网)

译者:中慧言-王芳

Fed Chair Jerome Powell was asked at the FOMC press conference in September to clarify what he meant when he said a few months earlier the U.S. housing market would “reset.” His response? We’ve entered into a “difficult [housing] correction” that will see the U.S. housing market transition to a more “balanced” market for buyers and sellers alike.

However, Powell still hasn’t addressed the elephant in the room: Will U.S. home prices fall?

Fast forward to this week, and we finally got a better understanding of the central bank’s view on home prices: On Thursday, Fed Governor Christopher Waller told an audience at the University of Kentucky that it’s possible we could see a “material” drop in U.S. home prices.

“While this [housing] market correction could be fairly mild, I cannot dismiss the possibility of a much larger drop in demand and house prices before the market normalizes,” Waller told the crowd.

That’s the first time a Fed official has acknowledged that the ongoing housing correction could see home prices fall at a national level. Waller also admitted the home price correction might end up being more than a small tick down. It could, he says, be a “material [home price] correction.”

“Despite the risk of a material correction in house prices, several factors help reduce my concern that such a correction would trigger a wave of mortgage defaults and potentially destabilize the financial system,” Waller said. “One is that because of relatively tight mortgage underwriting in the 2010s, the credit scores of mortgage borrowers today are generally higher than they were prior to that last housing correction. Also, the experience of the last correction taught us that most borrowers only default when they experience a negative shock to their incomes in addition to being underwater on their mortgage.”

Reading between the lines, it looks like Waller is making four points. 1. The housing market correction could be “mild.” 2. There’s a scenario where the housing market correction isn’t mild 3. A sharp home price decline is possible. 4. If a sharp home price drop manifests, it wouldn’t trigger a 2008-type foreclosure wave or financial collapse.

Of course, the Fed acknowledging that home prices could fall comes after, well, home prices in many markets have already started to fall. Among the 148 major regional housing markets tracked by John Burns Real Estate Consulting, 98 markets have seen home values fall from their 2022 peaks. In 11 markets, the Burns Home Value Index has already dropped by more than 5%.

"Prices have even fallen in some areas of the country, especially those that saw the largest increases over the previous two years. And many builders are reportedly cutting their list prices and offering larger incentives," Waller told the crowd.

So far, the housing correction—which is driven by spiking mortgage rates—is hitting one of two markets the hardest.

The first group are high-cost tech hubs. That includes markets like San Francisco (down 7.8% from its 2022 peak), San Jose (down 9%), and Seattle (down 6.2%). Not only are their high-end real estate markets more rate sensitive, but so are their tech sectors.

The other group are bubbly markets like Austin (down 6.2%), Boise (down 5.3%), and Phoenix (down 4.4%). During the Pandemic Housing Boom, those bubbly markets saw home prices reach levels well beyond what local incomes would historically support. According to Moody's Analytics, Austin and Phoenix are "overvalued" by 61% and 57%, respectively. Historically speaking, significantly "overvalued" housing markets are the most vulnerable to home price cuts during a housing correction.

请打开财富Plus APP