美国住房贷款延期还款计划结束,房地产市场严阵以待

Lance Lambert

2021-09-08

今年9月过后,美国房地产市场将发生严重动荡。

文本设置

文本设置

Plus(0条)

Plus(0条)

在新冠肺炎疫情最严重的时期,美国有超过720万业主参加了住房按揭延期还款计划,部分借款人可以暂停还款。之后,美国迎来了史上最快速的一轮经济复苏。现在参加延期还款计划的借款人减少到170万。

但这个人数很快就会减少到零。

因为拜登-哈里斯政府已经明确宣布,在住房按揭延期还款计划9月30日到期之后,没有再次延长该计划的打算。借款人不会一次性全部退出该计划,而是将在未来几个月内逐步退出。

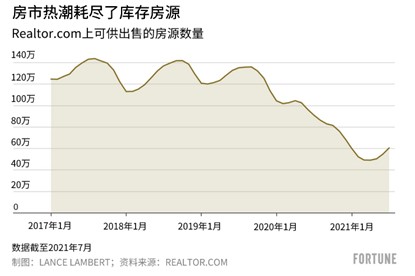

然而,正如《财富》杂志之前的报道,这将引发房地产市场的大规模动荡。美国有超过8000万业主,170万听起来并不多,但要知道目前在realtor.com上出售的房屋只有60多万套。事实上,今年的住房库存创下了40年最低。所以,170万面临还款困难的借款人中即使只有一小部分人选择出售房屋,而不是恢复月供,就会给房地产市场造成冲击。

早在7月,《财富》杂志曾经邀请Home.LLC公司的研究人员预测延期还款计划结束对市场的影响。该初创公司为购房人提供首付款援助,获得利润分成作为回报。研究人员发现,该计划结束将导致美国房屋库存量到今年晚些时候增加11%。虽然这几乎会将房地产市场从卖方市场转变为买方市场,但能够让市场稍微降温。

即使在住房按揭延期还款计划结束之前,美国的房地产市场也已经开始降温。2020年4月至2021年4月,美国住房库存量大幅减少了50%,之后开始恢复增长。6月,住房库存量增加了8.8%,7月再次增加了10.4%。据房地产研究公司CoreLogic统计,去年,美国中位数房价上涨了17.2%。CoreLogic预测,未来12个月房价上涨幅度将小幅放缓至3.2%。

但这个预测没有考虑到按揭延期还款计划取消对市场的影响。房地产市场不太可能出现崩溃:业内人士告诉《财富》杂志,在短期内,一批购房人群的出现和多年来的在建房屋数量不足,将继续导致房地产市场供不应求。

大规模止赎潮同样不会出现。强劲的房地产市场意味着面临还款困难的大部分业主都有正房屋净值。所以,如果这些业主决定停止还款,他们就可以把房子卖掉。这与经济大衰退(Great Recession)期间的情形截然不同:当时,有数以百万计资不抵债的借款人,其剩余按揭贷款额超过了名下房产的价值,他们是被迫卖掉了自己的房子。但未来几个月,住房库存量依旧会大幅增加。(财富中文网)

译者:刘进龙

审校:汪皓

在新冠肺炎疫情最严重的时期,美国有超过720万业主参加了住房按揭延期还款计划,部分借款人可以暂停还款。之后,美国迎来了史上最快速的一轮经济复苏。现在参加延期还款计划的借款人减少到170万。

但这个人数很快就会减少到零。

因为拜登-哈里斯政府已经明确宣布,在住房按揭延期还款计划9月30日到期之后,没有再次延长该计划的打算。借款人不会一次性全部退出该计划,而是将在未来几个月内逐步退出。

然而,正如《财富》杂志之前的报道,这将引发房地产市场的大规模动荡。美国有超过8000万业主,170万听起来并不多,但要知道目前在realtor.com上出售的房屋只有60多万套。事实上,今年的住房库存创下了40年最低。所以,170万面临还款困难的借款人中即使只有一小部分人选择出售房屋,而不是恢复月供,就会给房地产市场造成冲击。

早在7月,《财富》杂志曾经邀请Home.LLC公司的研究人员预测延期还款计划结束对市场的影响。该初创公司为购房人提供首付款援助,获得利润分成作为回报。研究人员发现,该计划结束将导致美国房屋库存量到今年晚些时候增加11%。虽然这几乎会将房地产市场从卖方市场转变为买方市场,但能够让市场稍微降温。

即使在住房按揭延期还款计划结束之前,美国的房地产市场也已经开始降温。2020年4月至2021年4月,美国住房库存量大幅减少了50%,之后开始恢复增长。6月,住房库存量增加了8.8%,7月再次增加了10.4%。据房地产研究公司CoreLogic统计,去年,美国中位数房价上涨了17.2%。CoreLogic预测,未来12个月房价上涨幅度将小幅放缓至3.2%。

但这个预测没有考虑到按揭延期还款计划取消对市场的影响。房地产市场不太可能出现崩溃:业内人士告诉《财富》杂志,在短期内,一批购房人群的出现和多年来的在建房屋数量不足,将继续导致房地产市场供不应求。

大规模止赎潮同样不会出现。强劲的房地产市场意味着面临还款困难的大部分业主都有正房屋净值。所以,如果这些业主决定停止还款,他们就可以把房子卖掉。这与经济大衰退(Great Recession)期间的情形截然不同:当时,有数以百万计资不抵债的借款人,其剩余按揭贷款额超过了名下房产的价值,他们是被迫卖掉了自己的房子。但未来几个月,住房库存量依旧会大幅增加。(财富中文网)

译者:刘进龙

审校:汪皓

At the height of the pandemic, more than 7.2 million homeowners were in the mortgage forbearance program, which allows some borrowers to pause their payments. The economy has since posted one of the fastest recoveries in history. Now, just 1.7 million borrowers are enrolled in the forbearance program.

But soon it’ll be zero.

The Biden-Harris administration has made it clear it has no plans for another extension of the mortgage forbearance program, which is set to lapse on Sept. 30. Borrowers won’t all get removed at once, instead they’ll be phased out over a period of several months.

Nonetheless, as Fortune has previously reported, this is a major shake-up headed for the housing market. In a nation of more than 80 million homeowners, 1.7 million might not sound like a lot—until you consider there are just over 600,000 homes for sale right now on realtor.com. In fact, this year housing inventory hit a 40-year low. So, if even a small percentage of these 1.7 million struggling borrowers opt to sell—rather than returning to their monthly payments—it could cause a shock in the housing market.

Back in July, Fortune reached out to researchers at Home.LLC, a startup that provides down payment assistance to homebuyers in return for a share of profits, to forecast how the end of forbearance would impact the market. They found the end of the program is likely to see U.S. inventory—homes for sale—rise by 11% later this year. While that’ll hardly shift the housing market from a seller’s market to a buyer’s market, it would soften the market a bit.

Even before mortgage forbearance ends, the market is already starting to cool. After seeing housing inventory plummet over 50% between April 2020 to April 2021, it’s moving up again. Inventory levels ticked up 8.8% in June, and another 10.4% in July. Over the past year, median home prices are up 17.2%, according to real estate research firm CoreLogic. In the coming 12 months, CoreLogic foresees that slowing down a bit, to just a 3.2% appreciation.

But don’t expect the end of forbearance to sink the market. A housing market crash is very unlikely: In the short term, a wave of demographics and years of under-building will ensure, industry insiders tell Fortune, that demand outmatches supply.

A foreclosure meltdown is also unlikely. The strong housing market means most of these struggling homeowners have positive home equity. So if these homeowners decide to walk away, they can simply sell. That is very different from what happened during the Great Recession: Millions of underwater borrowers, with mortgage balances greater than their home’s value—were forced to sell. But we could still see a lot more inventory in the coming months.

请打开财富Plus APP