外围股市连创新高,为什么英股就是涨不动?

Adrian Croft

2021-08-22

富时100指数在去年下跌了14%,今年表现仍然不给力。

文本设置

文本设置

Plus(0条)

Plus(0条)

2020年英国股市表现惨淡,至于今年,在英国与欧盟达成了脱欧后贸易协议,以及其经济正自新冠疫情的影响中摆脱出来,出现了强劲复苏的大背景下,人们曾经希望英股能够强势反弹。

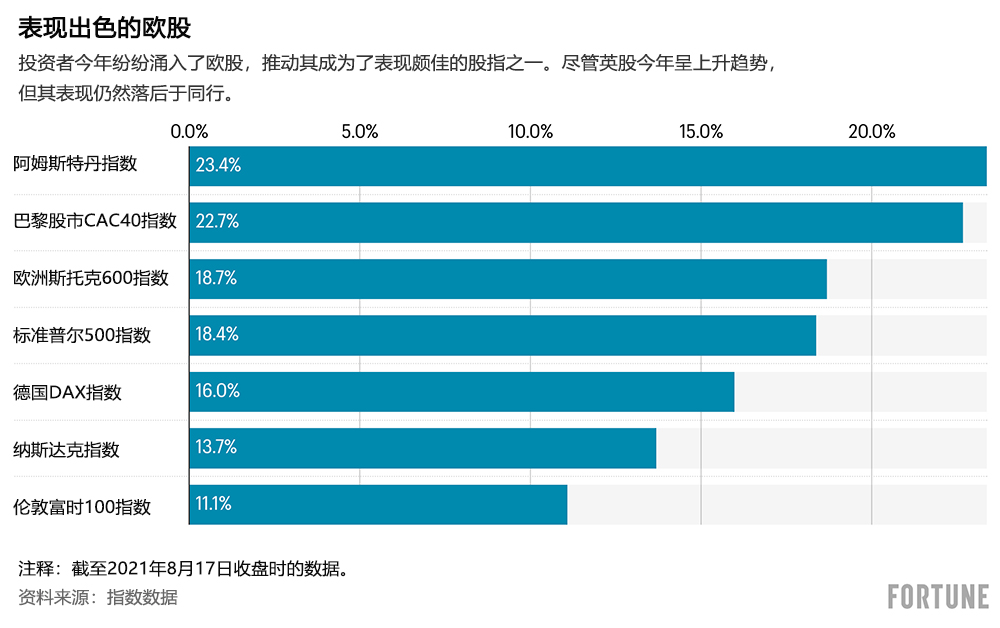

但到目前为止,伦敦股市的表现并不怎么亮眼。今年迄今,由在伦敦证券交易所上市且市值最大的100家公司组成的英国富时100指数(FTSE 100 Index)上涨了10%,其表现不及标准普尔500指数(S&P 500,涨幅为19%),以及欧盟(European Union)的几大交易所(英国刚刚与其分道扬镳)。

阿姆斯特丹和巴黎证券交易所是欧洲表现最出色的交易所,今年迄今已经上涨逾22%,而德国的DAX指数上涨了15%,其中包括股息再投资收入。

对伦敦股市来说更糟糕的是,其涨幅不大的前提是富时100指数在去年下跌了14%,是当时表现最差的几个主要股市之一。去年英国受到了新冠疫情的重创,13万人因此死亡,持续数月的封锁措施则致使以服务业为主的经济陷入了停滞,GDP萎缩10%,创下了有记录以来最大的年度跌幅。

今年伦敦股市的复苏本不该如此缓慢。那么它为何如此落后于同行呢?

脱欧和“传统经济”的重担

2021年本该是伦敦股市遥遥领先的一年。

英国于2016年通过了公投决定退出欧盟,在经过四年多一波三折的脱欧谈判后,其终于在2020年平安夜与欧盟达成了脱欧后贸易协议,允许双方在英国脱欧后继续进行免关税和免配额的货物贸易。

随后,由于疫苗供应充足和接种进度领先,政府借此解除了许多封锁规定,英国经济得以重新开放,走在了其他欧洲国家的前面。据英国财政部部长里希·苏纳克说,英国今年第二季度经济环比增长4.8%,在七国集团(Group of Seven)中表现最好。

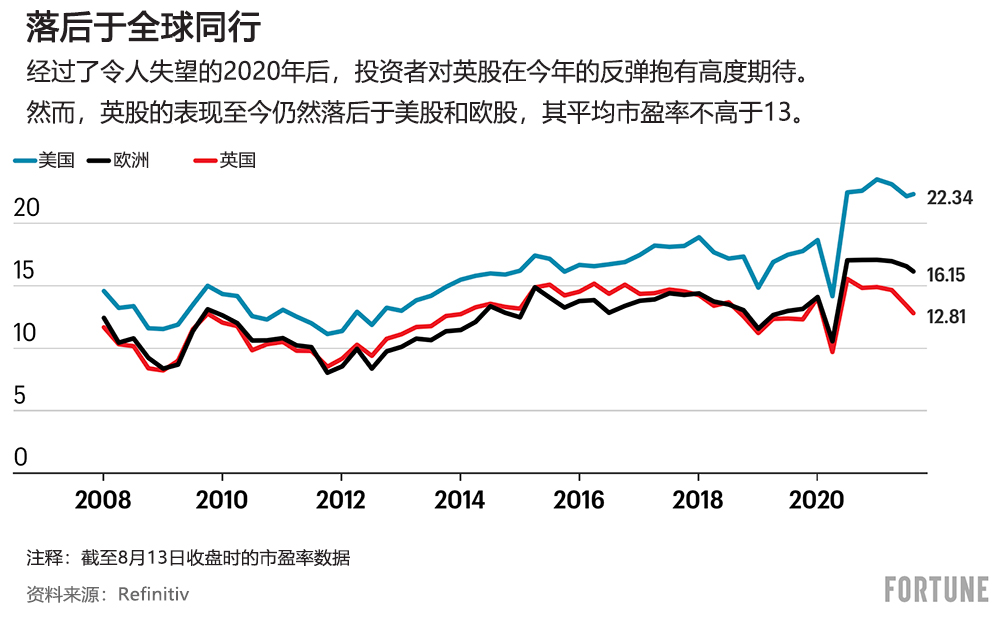

但英股上方仍然笼罩着一层阴霾,投资者对它们的估值远低于国际同行。数据提供商Refinitiv的数据显示,截至8月13日收盘时,英股的平均市盈率不到13,落后于市盈率16的欧股,也远低于美股的22。

资产管理公司施罗德集团(Schroders)的英国投资组合经理尼克·基萨克表示,英国脱欧拉低了投资者对其的印象分是英国市场表现不佳的部分原因。

另一个原因是,富时100指数的成员多是“传统经济”公司,矿业公司有力拓集团(Rio Tinto)和必和必拓(BHP,8月17日宣布将在澳大利亚进行主要上市)、石油公司有荷兰皇家壳牌集团(Shell)和英国石油公司(BP)、烟草公司有英美烟草(British American Tobacco)和帝国品牌(Imperial Brands),银行则有巴克莱(Barclays)和劳埃德(Lloyds)等。英国市值最大的公司是制药巨头阿斯利康(AstraZeneca,1800亿美元),该公司与牛津大学(Oxford University)合作,为大多数英国人供应了新冠疫苗。

“不受欢迎”

然而,多年来,投资者的注意力一直牢牢地粘在成长型股票上,特别是有望在未来迅速扩张的科技股。疫情期间,鉴于封锁措施促进了线上交易的迅速发展,并证明了我们对技术的依赖性,这一趋势只会愈发加强。对英国来说,不幸的是富时100指数中几乎没有几家股价正在飙升的科技公司,能够推动英股像美股那样创下历史新高。没有苹果(Apple),没有谷歌(Google),没有亚马逊(Amazon)。

今年头几个月,英国的好日子似乎已经到来了,当时通胀和利率预期不断上升,以收益和股息为基础的价值型股票可能会因此估值变低,促使人们纷纷投向价值型股票,而英国则可以提供大量价值型股票。通胀和利率上升会不利于成长型股票,因为它们会降低未来预期收益的当前价值。

但结果证明这种变化非常短暂。在10年期美国国债收益率下行,央行说服了投资者通胀飙升只是暂时情况后,成长型股票在年中再次领跑。

为此,投资公司Hargreaves Lansdown的股票分析师尼克·海特表示,伦敦股市表现不佳的大部分原因可以归结为“在英国上市的股票类型不受欢迎”这一事实。

英国折价?

让投资专家摸不着头脑的是,一些公司出现折价交易仅仅是因为它们的总部位于英国,不管其业绩和前景如何。

施罗德集团最近将英国公司与欧洲大陆、美国和全球的同类企业进行了比较,研究表明,“许多优质企业普遍存在折价交易,”基萨克在接受《财富》杂志采访时表示。

他说,施罗德持股前十中的几只英国股票,例如分析公司RELX(前身为里德·爱思唯尔集团)、保险公司保诚保险(Prudential)和医疗设备制造商施乐辉(Smith & Nephew)等,与全球同行相比,它们在没有明显原因的情况下出现了大幅折价。

Hargreaves Lansdown公司的海特指出,许多受到折价影响的公司甚至与英国经济没有密切联系。

像日用消费品公司联合利华(Unilever)和利洁时集团(Reckitt Benckiser),以及饮料巨头帝亚吉欧(Diageo)这样的公司“几乎只有一个英国公司的名头而已,”海特说。“他们在全球都有子公司,他们在世界各地做生意。在全球经济的大背景下,英国经济的成败在很多情况下只是一个小插曲。”

更让人困惑的是,由中型公司组成的富时250指数(FTSE 250 Index)与国内市场的关联通常比富时100指数更密切。但今年迄今为止,其涨幅达到了16%,比富时100指数更快。

一些投资者已经开始从估值偏低的英股中寻找机遇。Refinitiv 的数据显示,今年迄今为止,收购英国企业总交易价值已经增长了277%,达到2320亿美元。网络安全公司NortonLifeLock斥资超过80亿美元收购了总部位于捷克共和国的Avast,它是富时100指数中为数不多的几家大型科技公司之一。美国工程公司派克汉尼汾(Parker-Hannifin)提出以70%的溢价收购英国航空航天公司梅吉特(Meggitt),引发了一场可能的收购战。两家美国私募股权公司正在竞购英国连锁超市莫里森(Morrisons)。

基萨克表示,与全球市场相比,英国股市仍然保持低位,他预计股市会出现反弹。

“随着股市在脱欧后变得舒适起来,英国与欧洲大陆或美国等全球同行之间的估值差距应该会逐渐缩小。”他说。“即使全球资产配置机构没有这么做,企业并购也会推动这一结果的产生。”

英镑效应

其他市场专家表示,如果考虑到由于英国脱欧迷雾消散和疫苗接种步伐加快,英镑走强,那么与欧洲竞争对手相比,英国股市的表现不佳就不是那么明显了。

自2020年3月疫情最严重的时候以来,英镑兑欧元汇率上涨了11%,兑美元汇率上涨了19%,因此用美元或欧元衡量的话,英股的涨幅要高很多。

但英镑走强也对富时100指数中的大型跨国公司造成了不利影响,这些公司在世界各地用多种货币记账收入然后将利润换算成英镑,致使它们的业绩黯然失色。对于以美元计价的矿业和能源公司来说,这一直是一个特殊问题。

投行Liberum Capital的投资策略主管约阿希姆·克莱门特表示,英股表现之所以逊于欧股,90%是因为英镑走强。

他对英国和欧洲股市的前景非常看好。他告诉《财富》杂志,英国和欧洲今年的平均回报率“非常接近”20%,“我认为明年还会再达到15%至20%”。

克莱门特表示,在酒店和餐馆重新开业以及经济全面复苏的大背景下,他预计,与欧洲其他国家和美国经济相比,英国经济在2021年下半年和2022年的增长将更为强劲。在股市层面这一优势将变为,相比起欧洲同行英股表现稍好。

但是,尽管他预计需求释放将导致今明两年对英国的投资增加,但克莱门特认为,英国经济的中长期前景“肯定受到了脱欧的不利影响,特别是考虑到我们现在脱欧相对艰难”。(财富中文网)

译者:Claire

2020年英国股市表现惨淡,至于今年,在英国与欧盟达成了脱欧后贸易协议,以及其经济正自新冠疫情的影响中摆脱出来,出现了强劲复苏的大背景下,人们曾经希望英股能够强势反弹。

但到目前为止,伦敦股市的表现并不怎么亮眼。今年迄今,由在伦敦证券交易所上市且市值最大的100家公司组成的英国富时100指数(FTSE 100 Index)上涨了10%,其表现不及标准普尔500指数(S&P 500,涨幅为19%),以及欧盟(European Union)的几大交易所(英国刚刚与其分道扬镳)。

阿姆斯特丹和巴黎证券交易所是欧洲表现最出色的交易所,今年迄今已经上涨逾22%,而德国的DAX指数上涨了15%,其中包括股息再投资收入。

对伦敦股市来说更糟糕的是,其涨幅不大的前提是富时100指数在去年下跌了14%,是当时表现最差的几个主要股市之一。去年英国受到了新冠疫情的重创,13万人因此死亡,持续数月的封锁措施则致使以服务业为主的经济陷入了停滞,GDP萎缩10%,创下了有记录以来最大的年度跌幅。

今年伦敦股市的复苏本不该如此缓慢。那么它为何如此落后于同行呢?

脱欧和“传统经济”的重担

2021年本该是伦敦股市遥遥领先的一年。

英国于2016年通过了公投决定退出欧盟,在经过四年多一波三折的脱欧谈判后,其终于在2020年平安夜与欧盟达成了脱欧后贸易协议,允许双方在英国脱欧后继续进行免关税和免配额的货物贸易。

随后,由于疫苗供应充足和接种进度领先,政府借此解除了许多封锁规定,英国经济得以重新开放,走在了其他欧洲国家的前面。据英国财政部部长里希·苏纳克说,英国今年第二季度经济环比增长4.8%,在七国集团(Group of Seven)中表现最好。

但英股上方仍然笼罩着一层阴霾,投资者对它们的估值远低于国际同行。数据提供商Refinitiv的数据显示,截至8月13日收盘时,英股的平均市盈率不到13,落后于市盈率16的欧股,也远低于美股的22。

资产管理公司施罗德集团(Schroders)的英国投资组合经理尼克·基萨克表示,英国脱欧拉低了投资者对其的印象分是英国市场表现不佳的部分原因。

另一个原因是,富时100指数的成员多是“传统经济”公司,矿业公司有力拓集团(Rio Tinto)和必和必拓(BHP,8月17日宣布将在澳大利亚进行主要上市)、石油公司有荷兰皇家壳牌集团(Shell)和英国石油公司(BP)、烟草公司有英美烟草(British American Tobacco)和帝国品牌(Imperial Brands),银行则有巴克莱(Barclays)和劳埃德(Lloyds)等。英国市值最大的公司是制药巨头阿斯利康(AstraZeneca,1800亿美元),该公司与牛津大学(Oxford University)合作,为大多数英国人供应了新冠疫苗。

“不受欢迎”

然而,多年来,投资者的注意力一直牢牢地粘在成长型股票上,特别是有望在未来迅速扩张的科技股。疫情期间,鉴于封锁措施促进了线上交易的迅速发展,并证明了我们对技术的依赖性,这一趋势只会愈发加强。对英国来说,不幸的是富时100指数中几乎没有几家股价正在飙升的科技公司,能够推动英股像美股那样创下历史新高。没有苹果(Apple),没有谷歌(Google),没有亚马逊(Amazon)。

今年头几个月,英国的好日子似乎已经到来了,当时通胀和利率预期不断上升,以收益和股息为基础的价值型股票可能会因此估值变低,促使人们纷纷投向价值型股票,而英国则可以提供大量价值型股票。通胀和利率上升会不利于成长型股票,因为它们会降低未来预期收益的当前价值。

但结果证明这种变化非常短暂。在10年期美国国债收益率下行,央行说服了投资者通胀飙升只是暂时情况后,成长型股票在年中再次领跑。

为此,投资公司Hargreaves Lansdown的股票分析师尼克·海特表示,伦敦股市表现不佳的大部分原因可以归结为“在英国上市的股票类型不受欢迎”这一事实。

英国折价?

让投资专家摸不着头脑的是,一些公司出现折价交易仅仅是因为它们的总部位于英国,不管其业绩和前景如何。

施罗德集团最近将英国公司与欧洲大陆、美国和全球的同类企业进行了比较,研究表明,“许多优质企业普遍存在折价交易,”基萨克在接受《财富》杂志采访时表示。

他说,施罗德持股前十中的几只英国股票,例如分析公司RELX(前身为里德·爱思唯尔集团)、保险公司保诚保险(Prudential)和医疗设备制造商施乐辉(Smith & Nephew)等,与全球同行相比,它们在没有明显原因的情况下出现了大幅折价。

Hargreaves Lansdown公司的海特指出,许多受到折价影响的公司甚至与英国经济没有密切联系。

像日用消费品公司联合利华(Unilever)和利洁时集团(Reckitt Benckiser),以及饮料巨头帝亚吉欧(Diageo)这样的公司“几乎只有一个英国公司的名头而已,”海特说。“他们在全球都有子公司,他们在世界各地做生意。在全球经济的大背景下,英国经济的成败在很多情况下只是一个小插曲。”

更让人困惑的是,由中型公司组成的富时250指数(FTSE 250 Index)与国内市场的关联通常比富时100指数更密切。但今年迄今为止,其涨幅达到了16%,比富时100指数更快。

一些投资者已经开始从估值偏低的英股中寻找机遇。Refinitiv 的数据显示,今年迄今为止,收购英国企业总交易价值已经增长了277%,达到2320亿美元。网络安全公司NortonLifeLock斥资超过80亿美元收购了总部位于捷克共和国的Avast,它是富时100指数中为数不多的几家大型科技公司之一。美国工程公司派克汉尼汾(Parker-Hannifin)提出以70%的溢价收购英国航空航天公司梅吉特(Meggitt),引发了一场可能的收购战。两家美国私募股权公司正在竞购英国连锁超市莫里森(Morrisons)。

基萨克表示,与全球市场相比,英国股市仍然保持低位,他预计股市会出现反弹。

“随着股市在脱欧后变得舒适起来,英国与欧洲大陆或美国等全球同行之间的估值差距应该会逐渐缩小。”他说。“即使全球资产配置机构没有这么做,企业并购也会推动这一结果的产生。”

英镑效应

其他市场专家表示,如果考虑到由于英国脱欧迷雾消散和疫苗接种步伐加快,英镑走强,那么与欧洲竞争对手相比,英国股市的表现不佳就不是那么明显了。

自2020年3月疫情最严重的时候以来,英镑兑欧元汇率上涨了11%,兑美元汇率上涨了19%,因此用美元或欧元衡量的话,英股的涨幅要高很多。

但英镑走强也对富时100指数中的大型跨国公司造成了不利影响,这些公司在世界各地用多种货币记账收入然后将利润换算成英镑,致使它们的业绩黯然失色。对于以美元计价的矿业和能源公司来说,这一直是一个特殊问题。

投行Liberum Capital的投资策略主管约阿希姆·克莱门特表示,英股表现之所以逊于欧股,90%是因为英镑走强。

他对英国和欧洲股市的前景非常看好。他告诉《财富》杂志,英国和欧洲今年的平均回报率“非常接近”20%,“我认为明年还会再达到15%至20%”。

克莱门特表示,在酒店和餐馆重新开业以及经济全面复苏的大背景下,他预计,与欧洲其他国家和美国经济相比,英国经济在2021年下半年和2022年的增长将更为强劲。在股市层面这一优势将变为,相比起欧洲同行英股表现稍好。

但是,尽管他预计需求释放将导致今明两年对英国的投资增加,但克莱门特认为,英国经济的中长期前景“肯定受到了脱欧的不利影响,特别是考虑到我们现在脱欧相对艰难”。(财富中文网)

译者:Claire

After the U.K. stock market’s dire performance in 2020, there were hopes U.K. shares would stage a storming comeback this year, lifted by a Brexit trade deal and a strong recovery from the COVID pandemic.

But so far the London market’s gains have been underwhelming. The flagship FTSE 100 index of the biggest U.K. companies is up 10% so far this year, but it is underperforming the S&P 500, up 19%, and the major bourses in the European Union, which Britain has just parted company with.

The Amsterdam and Paris exchanges are Europe’s star performers with gains of more than 22% so far this year, while Germany’s DAX is up 15%, including reinvested dividends.

Worse for London stocks is that this slow rise comes after the FTSE 100 slumped by 14% last year, one of the worst-performing major markets. The U.K. was hard hit by COVID last year, with 130,000 deaths to date and months of lockdown that sent the services-heavy economy into a tailspin, slashing GDP by a record 10% in 2020.

This year's London stock recovery wasn't supposed to be this slow. So why is the U.K. market so badly lagging its peers?

The weight of Brexit and the “old economy”

The year 2021 was meant to be when London shot ahead.

More than four years of uncertainty and wrangling following the 2016 Brexit vote to leave the EU ended with a Christmas Eve 2020 agreement that allowed tariff-free trade in goods between Britain and its biggest trading partner to continue after the U.K. left the bloc.

Britain then jumped ahead of other European countries by securing ample vaccine supplies and out-vaccinating them, allowing the government to end many restrictions and the economy to reopen. Britain’s 4.8% economic growth in the second quarter this year was the fastest in the Group of Seven major economies, according to Finance Minister Rishi Sunak.

But a pall still hangs over U.K. shares, with investors awarding them a much lower valuation than international peers. U.K. shares, as of the Aug. 13 close, are trading at an average multiple of less than 13 times earnings, according to data provider Refinitiv, lagging European shares, which trade on a multiple of 16 times earnings, and far below the 22 multiple for U.S. shares.

Nick Kissack, U.K. portfolio manager at asset management firm Schroders, says a Brexit hangover in investors’ perceptions is part of the reason for the U.K. market’s underperformance.

Another factor is that the FTSE 100 is viewed as heavy on “old economy” companies—miners like Rio Tinto and BHP (which announced on August 17 it will move to a primary listing in Australia), oil companies Shell and BP, cigarette companies British American Tobacco and Imperial Brands, and banks like Barclays and Lloyds. The U.K.’s most valuable company, worth $180 billion, is AstraZeneca, the pharma giant that partnered with Oxford University on the COVID vaccine given to most Brits.

“Unloved”

For years, however, investors’ focus has been firmly on growth stocks, especially tech stocks primed for fast future expansion. That has only increased during the pandemic as lockdowns accelerated the transition to online trade and showed how much we rely on technology. Unfortunately for the U.K., the FTSE 100 has few of the fast-growing tech companies that have driven U.S. indexes to record highs. No Apple, no Google, no Amazon.

The U.K.’s moment in the sun appeared to have arrived in the first few months of this year when rising inflation and interest rate expectations prompted a rotation to value stocks, shares that may be undervalued based on their earnings and dividends and which the U.K. is well supplied with. High inflation and rising interest rates are noxious for growth stocks as they reduce the current value of expected future earnings.

But the change turned out to be short-lived—growth stocks once again took the lead in midyear after central banks persuaded investors that a surge in inflation was only temporary and 10-year U.S. Treasury bond yields fell back.

To that end, Nick Hyett, equity analyst at investment firm Hargreaves Lansdown, says much of the London stock market’s underperformance can be chalked up to the fact that “the types of stocks that are listed in the U.K. are unloved.”

A U.K. discount?

What is making investment professionals scratch their heads is that some companies appear to trade at a discount simply because they are based in the U.K.—regardless of their performance and prospects.

Recent research by Schroders comparing U.K. businesses with equivalent companies in continental Europe, the U.S., and globally showed “a fairly pervasive and broad discount across a number of quality names," Kissack told Fortune.

Several U.K. stocks that are among Schroders’ top 10 holdings—such as analytics firm RELX (formerly Reed Elsevier), insurer Prudential, and medical device specialist Smith & Nephew—trade at hefty discounts to global peers for no obvious reason, he said.

Hyett of Hargreaves Lansdown notes that many of the companies being hit with a kind of U.K. discount are not even closely tied to the U.K. economy.

Companies like consumer goods groups Unilever and Reckitt Benckiser and drinks giant Diageo are “businesses that are in the U.K. almost in name only," Hyett said. "They have subsidiaries all over the world; they trade all over the world. The success or failure of the U.K. economy is a blip in the context of overall results in many cases."

Furthering the confusion, the FTSE 250 index of midcap companies that are generally more domestically focused than the FTSE 100 members has grown more quickly than the large-cap FTSE 100—up 16% so far this year.

Some investors have started to spot opportunities in these low U.K. valuations. Takeovers of U.K. companies have risen by 277% so far this year to $232 billion, according to Refinitiv. Cybersecurity company NortonLifeLock is paying more than $8 billion for Czech Republic–based Avast, one of the few big tech firms in the FTSE 100. U.S. engineering firm Parker-Hannifin has offered a 70% premium for U.K. aerospace firm Meggitt, sparking a possible takeover battle, and two U.S. private equity firms are vying to buy U.K. supermarket chain Morrisons.

Kissack said that U.K. equities remained cheap compared to global markets, and he expected them to bounce back.

“As the market gets comfortable in a post-Brexit world, the valuation discount that’s being applied to the U.K. versus continental European peers or global peers such as the U.S. should gradually narrow,” he said. “If it isn’t done by global asset allocators, it will be done via M&A."

The sterling effect

Other market experts say the U.K. stock market’s underperformance compared with European competitors is less pronounced if one takes account of the strengthening of the British pound as the Brexit fog cleared and the pace of vaccinations stepped up.

Sterling has gained 11% in value against the euro and 19% against the U.S. dollar since the depths of the pandemic in March 2020, so measured in dollars or euros, U.K. stock market gains would be much greater.

But the stronger pound has also hit the big multinational companies in the FTSE 100, which book revenues globally in a variety of currencies and then translate the profits back into pounds, taking the shine off their results. That has been a particular issue for mining and energy companies whose products are priced in dollars.

Joachim Klement, head of investment strategy at investment bank Liberum Capital, said stronger sterling accounted for 90% of the U.K. stock market’s underperformance compared with continental European markets.

He is bullish on the prospects for both U.K. and European stocks. The U.K. and Europe were “pretty much on track” to average a 20% return this year, “and I think we will get another 15% to 20% next year,” he told Fortune.

Klement said he expected the U.K. economy to grow more strongly than the rest of Europe and possibly also the U.S. in the second half of 2021 and 2022 as hotels and restaurants reopen and the economy bounces back, an advantage that would translate into marginally better performance by U.K. equities compared to their European peers.

But while he expects pent-up demand to lead to higher investment in the U.K. this year and next, Klement believes the U.K. economy’s medium- to long-term prospects “have definitely been damaged by Brexit, especially given that we now have a relatively hard Brexit.”

请打开财富Plus APP