美股面临的最大风险是什么?你可能完全想不到

Ben Carlson

2021-03-11

随着人们看到新冠疫情尽头的曙光,通胀预期开始抬头,但这对股市来说却不是什么好消息。

文本设置

文本设置

Plus(0条)

Plus(0条)

在新冠疫情的前半阶段,利率一直在做单向运动——下滑。于去年夏末降至0.5%的最低点之后,10年期国债收益率终于迎来了高涨。

没有人知道利率上涨的具体原因是什么,但随着人们看到疫情尽头的曙光,通胀预期开始抬头。如果利率的上涨是因为投资者预计未来的经济增速会更高,那这肯定是件好事情。

但投资者始终会担心风险,而且有人担心利率的此次上扬可能会让股市脱轨。这里当然存在这种可能性,但历史告诉我们,股市在利率上涨的环境中总是处变不惊。

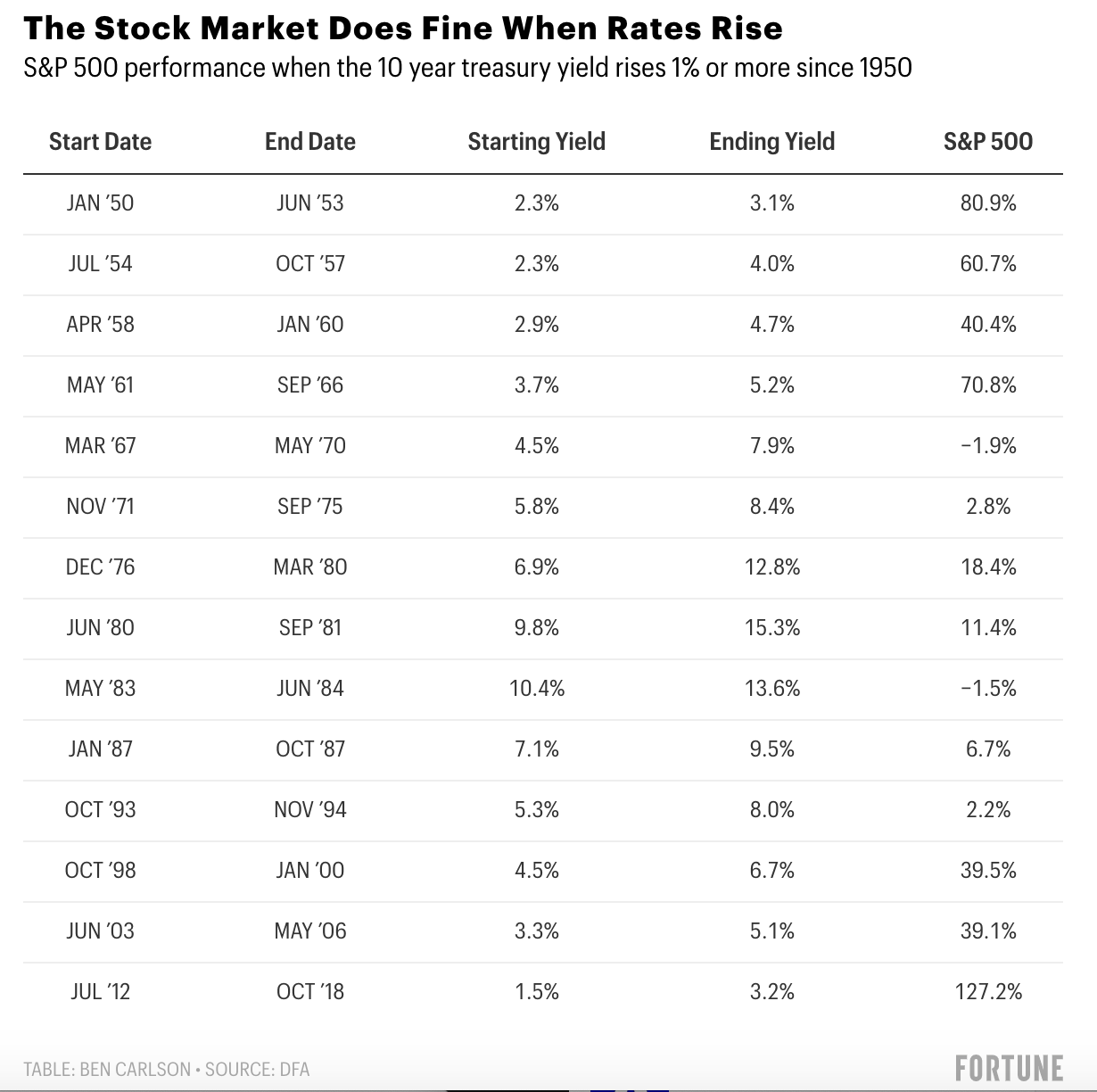

我回顾了自1950年以来每一次10年期国债收益率涨幅不低于1%时,美国股市在债券收益率上涨后的表现:

在利率上涨的环境下,股市下跌的情形仅出现过两次。事实上,股市在这些时期(利率增长1%或以上)的年化回报率为10.5%,基本上就是美国股市长期回报的平均水平。

值得注意的是,其中的一些利率增长时段确实出现在一些股市暴跌之前。1987年的利率上涨之后,股市在当年10月出现了历史上最大的单日跌幅。利率在20世纪90年代末互联网泡沫的最后几年中出现了上涨,当时美联储(Federal Reserve)正尝试消除股市疯狂的投机情绪。最终,美联储的举措奏效了,股市跌幅高达50%。

然而,我们确实不知道利率要达到哪个临界线才会让投资者认为事情已经失去了控制。这里的标准确实不好把握,更多的是对心态的考验。

如果上涨的利率并非是投资者在当前环境中需要担心的因素,那么我们应该关注什么?

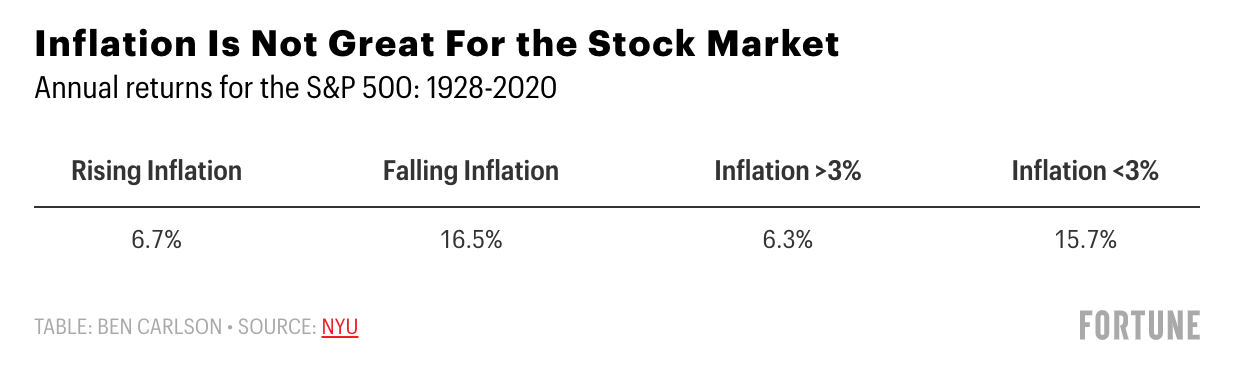

通胀就比利率水平重要的多。

自1928年以来,美国平均年化通胀率刚好在3%左右。基于标普500指数(S&P 500)在这个时期的平均回报,股市希望通胀率能够保持在这一水平之下,而且是只降不升。

多年来,在通胀率上升之际,股市平均年化回报率增长了6.7%,然而在通胀下跌时期,股市的平均年化回报接近17%。当我们审视某一年到下一年的通胀时,年化回报也会出现类似的现象。在历史上,当通胀高于上一年时,股市的平均回报率为6.3%,但当通胀出现同比下降时,股市的年化回报率接近16%。

如今,按照历史标准来看,通胀水平依然处于低位,同比增幅为1.4%。但通胀预期(按照5年期盈亏平衡通胀率计算)如今处于2013年以来的最高水平,达到了2.4%。然而这个数字依然低于长期平均水平,而且实际结果通常难以与预期完全吻合。

不断上升的利率和通胀预期对经济来说是个好消息。其中每个变量都可能会被疫情结束所带领的经济增长以及随之引发的消费者支出反弹而消化。

但是,投资者需要注意其中可能存在的潜在风险。当股市在去年疲软的经济环境中依然风生水起时,人们感觉并没有多大的风险。如果股市在今年不断提振的经济中略有停滞,人们也可能会有同样的感觉。然而这就是股市的运行方式,而且其当前的表现并不一定合乎情理。(财富中文网)

本文作者本·卡尔森(Ben Carlson)是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。作者可能持有文中提及的证券或资产。

译者:冯丰

审校:夏林

在新冠疫情的前半阶段,利率一直在做单向运动——下滑。于去年夏末降至0.5%的最低点之后,10年期国债收益率终于迎来了高涨。

没有人知道利率上涨的具体原因是什么,但随着人们看到疫情尽头的曙光,通胀预期开始抬头。如果利率的上涨是因为投资者预计未来的经济增速会更高,那这肯定是件好事情。

但投资者始终会担心风险,而且有人担心利率的此次上扬可能会让股市脱轨。这里当然存在这种可能性,但历史告诉我们,股市在利率上涨的环境中总是处变不惊。

我回顾了自1950年以来每一次10年期国债收益率涨幅不低于1%时,美国股市在债券收益率上涨后的表现:

在利率上涨的环境下,股市下跌的情形仅出现过两次。事实上,股市在这些时期(利率增长1%或以上)的年化回报率为10.5%,基本上就是美国股市长期回报的平均水平。

值得注意的是,其中的一些利率增长时段确实出现在一些股市暴跌之前。1987年的利率上涨之后,股市在当年10月出现了历史上最大的单日跌幅。利率在20世纪90年代末互联网泡沫的最后几年中出现了上涨,当时美联储(Federal Reserve)正尝试消除股市疯狂的投机情绪。最终,美联储的举措奏效了,股市跌幅高达50%。

然而,我们确实不知道利率要达到哪个临界线才会让投资者认为事情已经失去了控制。这里的标准确实不好把握,更多的是对心态的考验。

如果上涨的利率并非是投资者在当前环境中需要担心的因素,那么我们应该关注什么?

通胀就比利率水平重要的多。

自1928年以来,美国平均年化通胀率刚好在3%左右。基于标普500指数(S&P 500)在这个时期的平均回报,股市希望通胀率能够保持在这一水平之下,而且是只降不升。

多年来,在通胀率上升之际,股市平均年化回报率增长了6.7%,然而在通胀下跌时期,股市的平均年化回报接近17%。当我们审视某一年到下一年的通胀时,年化回报也会出现类似的现象。在历史上,当通胀高于上一年时,股市的平均回报率为6.3%,但当通胀出现同比下降时,股市的年化回报率接近16%。

如今,按照历史标准来看,通胀水平依然处于低位,同比增幅为1.4%。但通胀预期(按照5年期盈亏平衡通胀率计算)如今处于2013年以来的最高水平,达到了2.4%。然而这个数字依然低于长期平均水平,而且实际结果通常难以与预期完全吻合。

不断上升的利率和通胀预期对经济来说是个好消息。其中每个变量都可能会被疫情结束所带领的经济增长以及随之引发的消费者支出反弹而消化。

但是,投资者需要注意其中可能存在的潜在风险。当股市在去年疲软的经济环境中依然风生水起时,人们感觉并没有多大的风险。如果股市在今年不断提振的经济中略有停滞,人们也可能会有同样的感觉。然而这就是股市的运行方式,而且其当前的表现并不一定合乎情理。(财富中文网)

本文作者本·卡尔森(Ben Carlson)是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。作者可能持有文中提及的证券或资产。

译者:冯丰

审校:夏林

Throughout the first half of the pandemic, interest rates went in one direction—down. After bottoming out at 0.5% toward the end of the summer, 10-year Treasury yields are finally on the upswing.

No one knows the precise reason for the increase in rates, but inflation expectations are rising now that there is light at the end of the tunnel for the pandemic. When rates are rising because investors expect economic growth to be higher in the future, that’s a good thing.

But investors always worry about risk, and there is fear this rise in rates could derail the stock market. That is certainly possible, but history shows the stock market holds up well in rising rate environments.

I went back to 1950 to find each instance where the 10-year Treasury yield rose by 1% or more to see how U.S. stocks performed when bond yields were moving higher:

There have only been two instances where stocks fell during a rising rate environment. In fact, the annualized returns in each of these periods where rates rose 1% or more was 10.5%, which is right around the average long-term return for the U.S. stock market.

It is worth noting some of these rising rate environments did precede some nasty stock market falls. Rates raced higher in 1987 right before the biggest one-day crash in history in October of that year. And rates rose in the final couple of years in the late-1990s dotcom bubble as the Fed was trying to snuff out a speculative mania. Eventually, it worked, and stocks got cut in half.

But we certainly don’t know the exact level of rates in which investors would determine things have gotten out of hand. There is no line in the sand on these things. It’s more of an exercise in psychology than anything.

So if it’s not rising interest rates investors need to worry about in the current environment then what should you be looking for?

Inflation is far more important to stocks than interest rate levels.

Since 1928, the average annual inflation rate in the United States is right around 3%. Based on the average returns for the S&P 500 in that time, the stock market would prefer the inflation rate stays below that level and that it’s falling not rising.

The average annual return for years in which the inflation rate is rising saw stocks up 6.7%, while the average annual return when inflation is falling was nearly 17%. A similar relationship exists when looking at inflation from one year to the next. Historically, when inflation has been higher than the previous year, stocks have returned an average of 6.3% against an average annual return of almost 16% when the inflation rate is down year over year.

Inflation is still quite low by historical standards today, at around 1.4% over the past year. But inflation expectations, as measured by the five-year break-even inflation rate, are now at their highest level since 2013 at 2.4%. That's still below the long-term average, and actual results don’t always line up perfectly with expectations.

Rising interest rates and inflation expectations are a good thing for the economy. Each of these variables is pricing in higher economic growth from the potential end of the pandemic and the ensuing spending boom it could bring about from consumers.

But investors need to be aware of the potential risks involved as well. It felt backward when the stock market was doing so well in the face of a weakening economy last year. It may feel equally backward if the stock market pauses for a bit in the face of a strengthening economy this year. Yet this is how the stock market works, and it doesn’t always make sense in the moment.

Ben Carlson is the director of institutional asset management at Ritholtz Wealth Management. He may own securities or assets discussed in this piece.

请打开财富Plus APP