大选风云里,华尔街的“愿望清单”

Bernhard Warner

2020-11-03

无论怎么看,2020年对于金融界而言都是最难的一年。

文本设置

文本设置

Plus(0条)

Plus(0条)

无论怎么看,2020年对于金融界而言都是艰难的一年。

截至9月23日收盘,金融股在标普500指数中的表现为倒数第二差,今年以来已累计下跌超24%。

造成这种局面的原因有很多,目前美国银行的利率已接近于零,基本贷款业务遭重挫。与此同时,疫情严重影响了正常经济活动,不断挤压着投行的盈利空间,并加大了不良贷款的风险。

更糟糕的是,十月以后,美国经济有所复苏,并购活动也开始增多,华尔街的形势却依旧低迷。

虽然近期金融股的标普500指数略微回升,但KBW纳斯达克银行指数仍在下跌,今年以来的跌幅已超逾38%。

总而言之,金融业急需一次大提振。那么美国大选是否会为其创造机会呢?

事实上,这个问题并不新鲜。

每隔四年,华尔街上的游说者们就会针对下一届政府起草一份“愿望清单”。该项工作早在就职日前便已启动,今年亦是如此。

税收问题

众所周知,特朗普一直是税收鹰派。2018年起,他把公司税率从35%下调至了21%。此举直接增加了银行收入并促成股市繁荣,同时也造成了巨大的财政赤字,未来必须依赖增税或财政紧缩措施来弥补。

值得注意的是,即便没有疫情,美国正常的经济增长速度也不足以填补这一巨大空缺。

包括华尔街各大总裁在内,几乎每一位《财富》五百强CEO,都希望公司税率能保持稳定。因此,拜登“提高企业应缴税率”的提议令这些公司颇为担忧。

“如果拜登获胜,参议院交由民主党控制,那么公司税很可能会从现有的21%提高到28%。只要做个简单的计算,就会发现标普500指数收益将会随之下降10%。” LPL金融研究公司副总裁兼市场策略师杰夫•布赫宾德于本周在“市场信号”广播栏目中表示。

(*注:此处的10%十分重要,后文会在“自由贸易”一节中详述。)

拜登增税计划的其余部分则旨在对高收入阶层施行社会保障、长期资本、及合法股息相关的组合增税。这也基本与特朗普于2017年定下的减税及就业法案背道而行。

现在看来这种情况发生的可能性较小,除非民主党大获全胜,但金融业内人士仍就这一可能性,以及其会导致的后果影响进行了计算。

“如果真的大幅提高股息税,那么派息企业和公共事业、日用品及金融业相关部门的利益将会受到损害,因为它们本身就和税收问题紧密相关。”私人财富管理公司班森集团(Bahnsen Group)创始人兼管理合伙人大卫•班森说道,他手下的客户资产已达2.5亿。

但班森还补充称,他手里的一些华尔街客户并没有对高税收政策过度恐慌。

“确实会有一些担忧,但没有到恐慌的程度。”

他指出“当初奥巴马上任以后,仅仅花了一年的时间,就在2010年结束了小布什的减税时代,那两年奥巴马一直都在强调减税政策对于经济复苏进程的不利影响。我觉得拜登接下来也会和奥巴马当年一样。”

此外,班森强调:“这一切都还不好说。因为美国历史上从未有任何一位总统在竞选期间提及税收计划,并保证在上任后能把计划落实成真正的税法。”

所以华尔街“愿望清单”上的第一条无疑就是:1.不要有太猛烈的税收改革。

基础设施投资

华盛顿内部人士和整个华尔街都心知肚明的是,在两党的激烈对抗中,有一点极具讽刺意味:与税收政策的分歧不同,双方实际上都很支持在基础设施建设中投入大量财政资金,以重振美国经济——但如果想让民主党控制的国会同意共和党的总统签署这项支出法案,几乎是不可能的。反之亦然。

几乎可以肯定的是,要实现大规模刺激财政支出方案的出台,国会和总统必须由同一党把控。

然而,华尔街的愿望仍是有望实现的。

美国企业界都希望能出台一项巨额的财政支出法案,以提振美国经济。而无论出台何种激励措施,只要能展开大规模重建,促进经济复苏,金融行业都将是最大的受益者之一,特别是能使美国用以恢复就业率的激励措施。

如果没有其他因素干扰,面对这样的现实条件,美联储最终可能会再次加息——而此举又将极大地帮助银行从负债累累的状况中纾困。

任何基础设施投资——无论是能加快美国现代化进程的道路和机场(特朗普对美国机场的现状很不满,特别是纽约的拉瓜迪亚机场),还是拜登投入1.7万亿美元用以建设“清洁能源未来”的承诺,都将受到金融业的欢迎。

因此,这里是第二个关键要点:支出,支出,支出。

“我可以肯定地说,”班森表示,“没有人会让债务状况阻碍政府进一步增加财政支出。”

自由贸易

特朗普的贸易战使全球的企业都打了个寒颤,而这也反过来冲击了美国的那些巨无霸企业,打破了他们的最低营收底线。

出口商受到的打击显而易见,但整个经济领域,包括华尔街,也都感受得到这种不利影响。

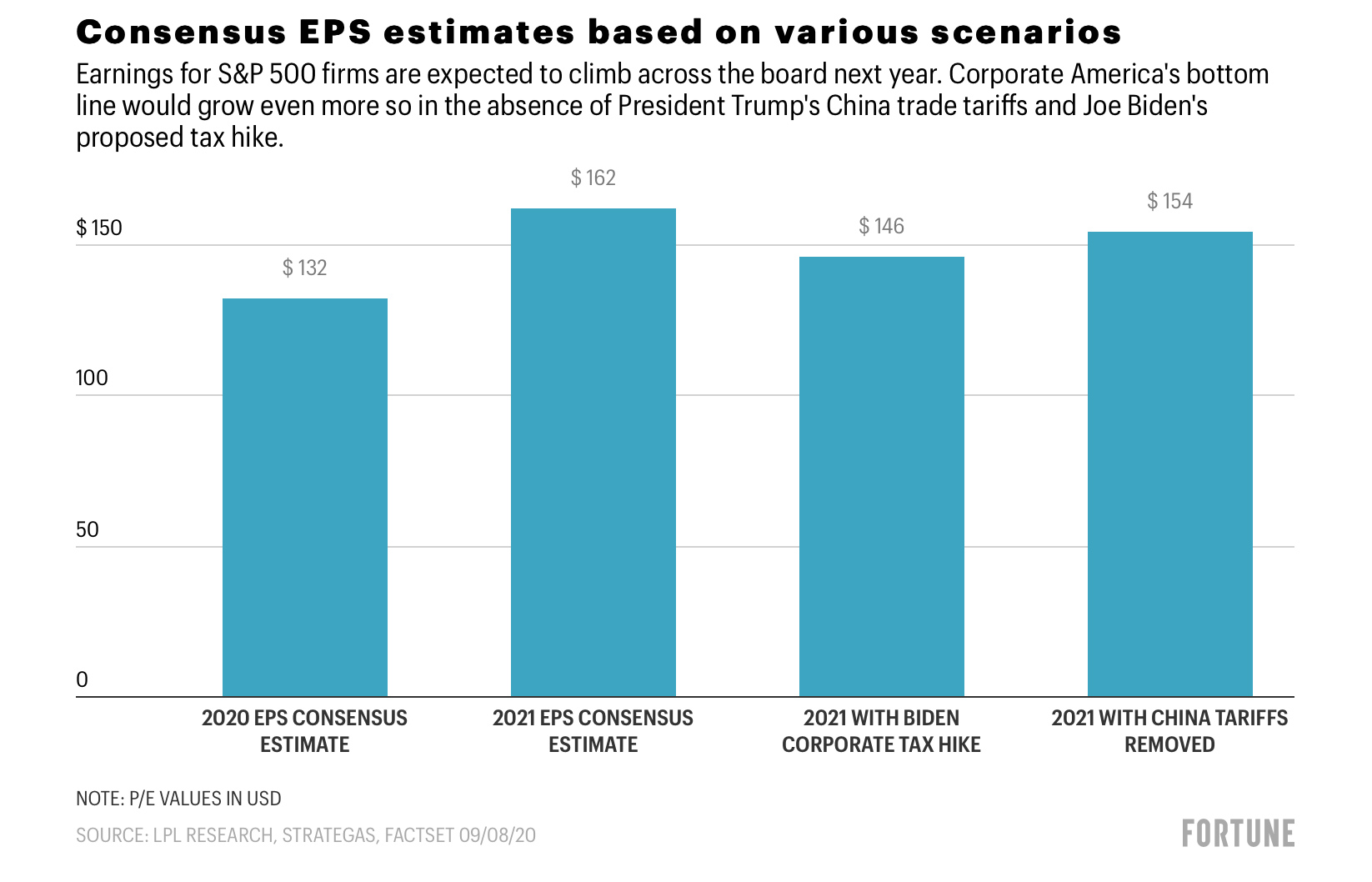

因此,根据LPL金融机构的分析师布赫宾德计算,如果取消与中国的贸易关税壁垒,将为标普500指数中的公司增加数十亿美元的收入。

布赫宾德认为,如果拜登胜选,那么在他的任期内,人们“可能会从政府的公共支出中获得潜在的收益,包括绿色能源补贴、基础设施投资等。再加上减少或取消某些针对中国的关税,这都将抵消那些由于对公司增税而造成的损失。”

下表是LPL金融机构对大选后的商业前景做出的详细预测。

目前,一个公认较为准确的估计是,到2021年,标普500指数公司每股的收益将同比增长近20%——那时,人们将迎来一个低税收和自由贸易的世界。

例如,仅从取消对华关税中获得的每股收益就可以使公司利润增加16%。维持现行的企业所得税税率将会带来10.6%的利润增幅,虽然幅度较小,但颇具意义。

尊敬的总统阁下,如果您看到这里,请让我们回到自由开放的全球贸易中,这对经济增长是有利的。另外,也请您参阅有关税收的第一点。

华尔街的监管

一直以来,华尔街就对行政机构加强监管保持警惕。今年也是如此。

但是,只要经济复苏是属于总统的一项职责,人们就会逐渐打消增加额外繁文缛节或监督审查的顾虑。

目前,双方似乎都没有控制华尔街的政治诉求。

班森表示:“如果谁有意对《沃尔克规则》和资本准入门槛等方面进一步施压,是不会受到欢迎的。”

也就是说,股票回购是引发两党关注的热点问题。如果“改革华尔街”被国会或白宫列入明年的议程,那么便会造成一定的损失。

但是另一方面,华尔街也在谋求向新一届管理者展示自己能力的机会,并希望能为解决美国经济问题贡献自己的一部分力量。

而他们之所以这么做,有一个明显的动机:金融业的老板们都在极力避免未来重蹈2020年的覆辙。(财富中文网)

编译:陈怡轩 陈聪聪

无论怎么看,2020年对于金融届而言都是艰难的一年。

截至9月23日收盘,金融股在标普500指数中的表现为倒数第二差,今年以来已累计下跌超24%。

造成这种局面的原因有很多,目前美国银行的利率已接近于零,基本贷款业务遭重挫。与此同时,疫情严重影响了正常经济活动,不断挤压着投行的盈利空间,并加大了不良贷款的风险。

更糟糕的是,十月以后,美国经济有所复苏,并购活动也开始增多,华尔街的形势却依旧低迷。

虽然近期金融股的标普500指数略微回升,但KBW纳斯达克银行指数仍在下跌,今年以来的跌幅已超逾38%。

总而言之,金融业急需一次大提振。那么美国大选是否会为其创造机会呢?

事实上,这个问题并不新鲜。

每隔四年,华尔街上的游说者们就会针对下一届政府起草一份“愿望清单”。该项工作早在就职日前便已启动,今年亦是如此。

税收问题

众所周知,特朗普一直是税收鹰派。2018年起,他把公司税率从35%下调至了21%。此举直接增加了银行收入并促成股市繁荣,同时也造成了巨大的财政赤字,未来必须依赖增税或财政紧缩措施来弥补。

值得注意的是,即便没有疫情,美国正常的经济增长速度也不足以填补这一巨大空缺。

包括华尔街各大总裁在内,几乎每一位《财富》五百强CEO,都希望公司税率能保持稳定。因此,拜登“提高企业应缴税率”的提议令这些公司颇为担忧。

“如果拜登获胜,参议院交由民主党控制,那么公司税很可能会从现有的21%提高到28%。只要做个简单的计算,就会发现标普500指数收益将会随之下降10%。” LPL金融研究公司副总裁兼市场策略师杰夫•布赫宾德于本周在“市场信号”广播栏目中表示。

(*注:此处的10%十分重要,后文会在“自由贸易”一节中详述。)

拜登增税计划的其余部分则旨在对高收入阶层施行社会保障、长期资本、及合法股息相关的组合增税。这也基本与特朗普于2017年定下的减税及就业法案背道而行。

现在看来这种情况发生的可能性较小,除非民主党大获全胜,但金融业内人士仍就这一可能性,以及其会导致的后果影响进行了计算。

“如果真的大幅提高股息税,那么派息企业和公共事业、日用品及金融业相关部门的利益将会受到损害,因为它们本身就和税收问题紧密相关。”私人财富管理公司班森集团(Bahnsen Group)创始人兼管理合伙人大卫•班森说道,他手下的客户资产已达2.5亿。

但班森还补充称,他手里的一些华尔街客户并没有对高税收政策过度恐慌。

“确实会有一些担忧,但没有到恐慌的程度。”

他指出“当初奥巴马上任以后,仅仅花了一年的时间,就在2010年结束了小布什的减税时代,那两年奥巴马一直都在强调减税政策对于经济复苏进程的不利影响。我觉得拜登接下来也会和奥巴马当年一样。”

此外,班森强调:“这一切都还不好说。因为美国历史上从未有任何一位总统在竞选期间提及税收计划,并保证在上任后能把计划落实成真正的税法。”

所以华尔街“愿望清单”上的第一条无疑就是:1.不要有太猛烈的税收改革。

基础设施投资

华盛顿内部人士和整个华尔街都心知肚明的是,在两党的激烈对抗中,有一点极具讽刺意味:与税收政策的分歧不同,双方实际上都很支持在基础设施建设中投入大量财政资金,以重振美国经济——但如果想让民主党控制的国会同意共和党的总统签署这项支出法案,几乎是不可能的。反之亦然。

几乎可以肯定的是,要实现大规模刺激财政支出方案的出台,国会和总统必须由同一党把控。

然而,华尔街的愿望仍是有望实现的。

美国企业界都希望能出台一项巨额的财政支出法案,以提振美国经济。而无论出台何种激励措施,只要能展开大规模重建,促进经济复苏,金融行业都将是最大的受益者之一,特别是能使美国用以恢复就业率的激励措施。

如果没有其他因素干扰,面对这样的现实条件,美联储最终可能会再次加息——而此举又将极大地帮助银行从负债累累的状况中纾困。

任何基础设施投资——无论是能加快美国现代化进程的道路和机场(特朗普对美国机场的现状很不满,特别是纽约的拉瓜迪亚机场),还是拜登投入1.7万亿美元用以建设“清洁能源未来”的承诺,都将受到金融业的欢迎。

因此,这里是第二个关键要点:支出,支出,支出。

“我可以肯定地说,”班森表示,“没有人会让债务状况阻碍政府进一步增加财政支出。”

自由贸易

特朗普的贸易战使全球的企业都打了个寒颤,而这也反过来冲击了美国的那些巨无霸企业,打破了他们的最低营收底线。

出口商受到的打击显而易见,但整个经济领域,包括华尔街,也都感受得到这种不利影响。

因此,根据LPL金融机构的分析师布赫宾德计算,如果取消与中国的贸易关税壁垒,将为标普500指数中的公司增加数十亿美元的收入。

布赫宾德认为,如果拜登胜选,那么在他的任期内,人们“可能会从政府的公共支出中获得潜在的收益,包括绿色能源补贴、基础设施投资等。再加上减少或取消某些针对中国的关税,这都将抵消那些由于对公司增税而造成的损失。”

下表是LPL金融机构对大选后的商业前景做出的详细预测。

目前,一个公认较为准确的估计是,到2021年,标普500指数公司每股的收益将同比增长近20%——那时,人们将迎来一个低税收和自由贸易的世界。

例如,仅从取消对华关税中获得的每股收益就可以使公司利润增加16%。维持现行的企业所得税税率将会带来10.6%的利润增幅,虽然幅度较小,但颇具意义。

尊敬的总统阁下,如果您看到这里,请让我们回到自由开放的全球贸易中,这对经济增长是有利的。另外,也请您参阅有关税收的第一点。

华尔街的监管

一直以来,华尔街就对行政机构加强监管保持警惕。今年也是如此。

但是,只要经济复苏是属于总统的一项职责,人们就会逐渐打消增加额外繁文缛节或监督审查的顾虑。

目前,双方似乎都没有控制华尔街的政治诉求。

班森表示:“如果谁有意对《沃尔克规则》和资本准入门槛等方面进一步施压,是不会受到欢迎的。”

也就是说,股票回购是引发两党关注的热点问题。如果“改革华尔街”被国会或白宫列入明年的议程,那么便会造成一定的损失。

但是另一方面,华尔街也在谋求向新一届管理者展示自己能力的机会,并希望能为解决美国经济问题贡献自己的一部分力量。

而他们之所以这么做,有一个明显的动机:金融业的老板们都在极力避免未来重蹈2020年的覆辙。(财富中文网)

编译:陈怡轩 陈聪聪

No matter how you look at it, 2020 has been rough on Big Finance.

Financial stocks are the second worst performer in the S&P 500, down more than 24% year to date as of the Sept. 23 close. There are plenty of culprits. Interest rates are near zero, cutting into banks’ bread-and-butter lending business. Meanwhile, the pandemic has put a big fat pause on economic activity, squeezing investment banking fees and ratcheting up the risk of underperforming loans.

Making matters worse, even as the economy begins to recover, and M&A picks up, investors continue to punish Wall Street. The KBW Nasdaq Bank Index has slumped 38% this year while the benchmark S&P 500 is up slightly.

In other words, Big Finance needs a big lift. Could it possibly come from Washington in an election year?

It’s not such a wild question. Every four years, Wall Street lobbyists draw up a wish list to put in front of the incoming administration. They usually start working on it well before Inauguration Day. This is what could be on such a memo this year.

Taxes

It’s no secret that President Trump has been a tax hawk, slashing the corporate tax rate from 35% to 21%, a move that went into effect in 2018. The positive result was a boom for the stock market, and a windfall in trading revenues for the banks. The downside? Mammoth deficit-spending that will have to be paid off down the road—either through increased taxes or through fiscal austerity measures. (Spoiler: Even before the coronavirus pandemic, the economy just wasn’t growing fast enough to magically plug that deficit hole.)

Just about every Fortune 500 CEO, Wall Street bosses included, wants to see this corporate tax rate hold steady. And so they’re a bit concerned with Democratic presidential candidate Joe Biden’s proposal to increase the rate businesses have to pay the tax man.

“If Biden wins and you get the Senate to flip, then there’s a good chance you get the corporate tax rate to go from 21% to 28%. Just doing the simple math takes the S&P 500 earnings down in the neighborhood of 10%,” Jeff Buchbinder, vice president and market strategist at LPL Financial Research, said on the Market Signals podcast this week.

(Remember that 10% figure. We’ll come back to it in the “Free trade” section.)

The rest of the Biden tax plan seeks to weaken Trump’s 2017 Tax Cuts and Jobs Act by raising taxes on a combination of income, Social Security, long-term capital gains, and qualified dividends for the upper-income brackets.

Unless it’s a clean sweep by the Democrats, none of this will happen. But the finance pros are still running the numbers on any and all possibilities, and what it would mean.

“I think if there was really to be a significant increase on taxation, on dividends, it would hurt dividend-paying companies and those sectors—utilities, consumer staples, and financial—that rely more heavily on them,” says David Bahnsen, founder and managing partner of the Bahnsen Group, a private wealth management firm with $2.5 billion in client assets under management.

But, Bahnsen adds, Wall Street—and by Wall Street, he’s also including investors like his clients—is not freaking out about the prospect of higher taxes. There’s concern, but not full-on alarm. “Obama,” he notes, “had all the political capital to let Bush’s tax cuts sunset in 2010. And he punted it out two years and cited, accurately, that it would be a bad thing to do in the midst of an economic recovery. I have every expectation that Biden would do the same thing.”

And besides, he adds: “What we do know is that not a single President in American history has had a tax plan in their campaign that then got photocopied and became a tax law. Ever.”

So at the top of the wish list you might see the words “1) Taxes: Don’t do anything drastic.”

Infrastructure spending

The irony of this one is well known to Washington insiders—and Wall Street too is now grasping the cruel twist. It goes something like this: Unlike with tax policy, there is actually plenty of bipartisan support for vast spending measures to rebuild America. And yet there’s little to no chance that, say, a Democrat-controlled Congress would give a Republican President the pleasure of signing such a spending bill into law. And vice versa.

It would almost certainly require one-party control to get a massive fiscal stimulus spending package to come to fruition.

And yet Wall Street can still dream of one.

Corporate America would love a big fat spending bill to jump-start the U.S. economy. And Big Finance would be among the industries to benefit most from any incentives that led to a building boom, particularly one that got America back to work. If nothing else, such a reality would conceivably lead to the conditions needed for the Federal Reserve to eventually raise interest rates again, a move that would help banks’ balance sheets dramatically.

Any spending measures—whether it be to modernize America’s roads and airports (Trump deplores the state of American airports, particularly LaGuardia Airport in New York) or Biden’s $1.7 trillion promise to build a “clean energy future”—would be most welcome to Big Finance.

So, here’s point No. 2: Spend, spend, spend.

“I promise you,” Bahnsen says, “there is nobody that’s going to let the debt get in the way of spending more money.”

Free trade

Trump’s trade wars have put the chill on global business, and that’s come home to roost on the bottom line of America’s biggest businesses. Yes exporters are hit, but the impact can be felt across the economy, to Wall Street too. Consequently, LPL Financial’s Buchbinder calculates that the removal of trade tariffs with China would add billions to the earnings of S&P 500 companies.

Under a Biden presidency, Buchbinder reckons, “you’d get spending potentially—green energy spending, infrastructure spending, and the like—plus reduction or elimination of some China tariffs. That would offset some of the drag on corporate earnings that you’d get from the possible corporate tax increase.”

This is spelled out in the chart below, furnished by LPL Financial.

At the moment, the consensus estimate is for the earnings per share of S&P 500 companies to climb nearly 20% year over year in 2021—that’s in a world of low taxes and free(r) trade. For example, the EPS boost alone from the removal of Chinese tariffs would amount to a 16% increase in corporate profits. Keeping the corporate tax rate as is would result in a smaller, but still meaningful, 10.6% rise in profits.

Dear President, the letter might then read, let’s go back to free and open global trade. It’s good for growth. And see point No. 1 about taxes.

Wall Street regulation

Wall Street is always wary of further regulatory scrutiny. This year is no different. But as long as the economic recovery is job one of the President, the concerns about additional red tape or stepped-up oversight are on the back burner.

There just doesn’t seem to be the political will at the moment to rein in Wall Street. “An attempt to re-amplify pressures around the Volcker Rule, capital requirements, etc., will not be viewed favorably” by Washington, Bahnsen says.

That said, one hot-button issue that’s getting bipartisan attention is stock buybacks. If Wall Street reform is on the agenda of Congress or the White House next year, this could become a casualty.

But otherwise, Wall Street will be looking to present itself to the new administration as part of the solution in getting America’s economy off the floor.

There’s an obvious motive: The bosses of Big Finance are desperate to avoid a repeat of 2020.

请打开财富Plus APP