美国股市持续创出新高,新手何时能入手?

|

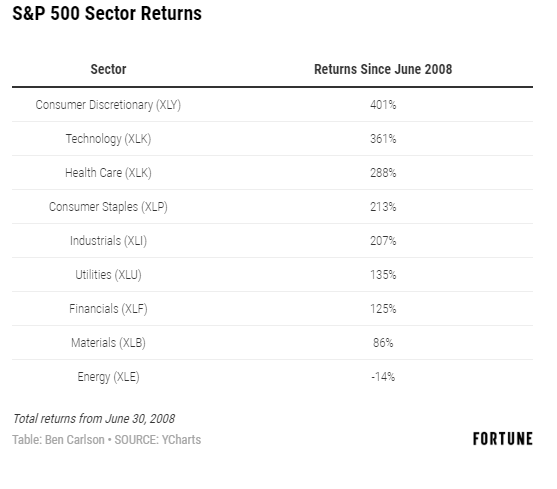

目前情况对投资者来说相当好。2019年的标普500指数屡创新高,而且今年其涨幅已经超过了去年底近20%的跌幅。虽然相对而言美股在这个周期中轻松领跑,但其他国家的股市也已经正式加入这场派对——MSCI全球所有国家指数(MSCI All-Country World Index)今年同样刷新了历史最高点。 股市屡创新高对于持股者来说好极了,但股市一味上涨也带来了下行压力。有些人持币等待好的买点,有些人刚有了一笔可以入市的新资金,如果股价持续上涨,他们不得不继续观望。股市不断上涨就像第二十二条军规那样矛盾,对当前回报率来说这是好迹象,但它几乎一定会压低预期回报率,原因是在股市上涨时,股息收益率和估值往往也会上升。 对于在市场出现惨案后可以较放心地买入股票的投资者来说,好消息是总会在某个地方出现熊市,甚至是在整个股票市场都在扼杀熊市之际。在本轮牛市中,以下三个领域在一定程度上一直处于落后位置。 能源股票 2008年6月,石油价格突破每桶150美元。从那时至今,油价下跌了三分之二,标普500指数的能源板块(代码:XLE)也滑落了13%以上,和该指数逾200%的上涨形成了鲜明对比。在此期间,能源股一直表现最差,远远落后于其他板块,而且这种情况甚至还没有结束。就连在金融危机中暴跌的金融股(代码:XLF)从2008年夏天到现在也领先能源板块135%以上。 |

Things are pretty good for investors at the moment. The S&P 500 continues to hit new high after new high in 2019. The gains this year have more than made up for the nearly 20% loss near the end of last year. While U.S. markets have outperformed handily on a relative basis during this cycle, foreign stocks have officially joined the party, with the MSCI All-Country World Index breaking out to new highs this year as well. New highs are great for those holding stocks in their portfolio but there is a downside when stocks seemingly do nothing but rise. Anyone who’s been holding cash waiting for lower prices and a better entry point or those with new savings to deploy into the markets have had to do so at higher and higher prices. Rising prices are a catch-22 in that they’re a welcome sign for current returns but almost certainly detract from expected returns, given that dividend yields and valuations tend to rise when markets move higher. The good thing for investors who are more comfortable buying when there’s blood in the streets is there will always be a bear market somewhere, even when the broad stock market is killing it. Here are three areas of the market that have been left behind to some extent during this bull market: Energy Stocks Oil prices hit more than $150/barrel in June 2008. Since then, oil prices are down two-thirds while the energy sector (ticker: XLE) of the S&P 500 has fallen more than 13% versus a gain of more than 200% for the overall index. Energy has been by far the worst sector during this period and it’s not even close. Even financials (ticker: XLF), which were crushed in the crisis, have outperformed energy since the summer of 2008 by more than 135%. |

|

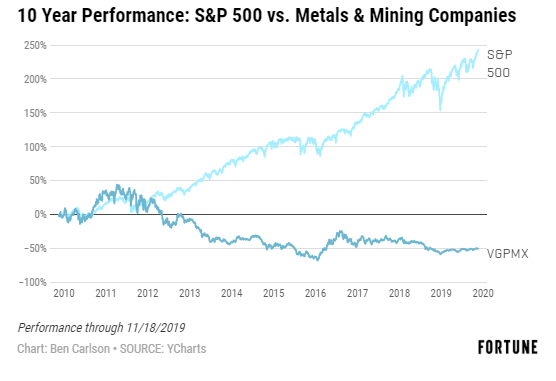

如果正在考虑抄底,目前收益率3.8%的能源板块ETF(代码:XLE)可供一试。 贵金属和矿业股 如果希望找到和大盘几乎没有关联的股票,那就非贵金属和采矿板块莫属。这些大宗商品生产商的股票经常有碾压波动性的表现,无论是向上还是向下。Vanguard Global Capital Cycles Fund(代码:VGPMX)不光在这个周期中一直落后于大盘,它还在不断地大幅下挫。过去10年VGPMX的跌幅接近50%,标普500指数则上涨逾240%。 |

The energy sector ETF (XLE) currently yields 3.8% for your troubles if you’re thinking about trying to catch a falling knife here. Precious Metals & Mining Stocks If you want to find stocks that have little correlation to the overall stock market, look no further than precious metals & mining stocks. These commodity producer stocks often exhibit pulverizing volatility, both to the upside and the downside. The Vanguard Global Capital Cycles Fund (ticker: VGPMX) has not only trailed the overall stock market during this cycle, but it’s also in the midst of a crash. Over the past 10 years, VGPMX is down nearly 50% while the S&P 500 is up more than 240%. |

|

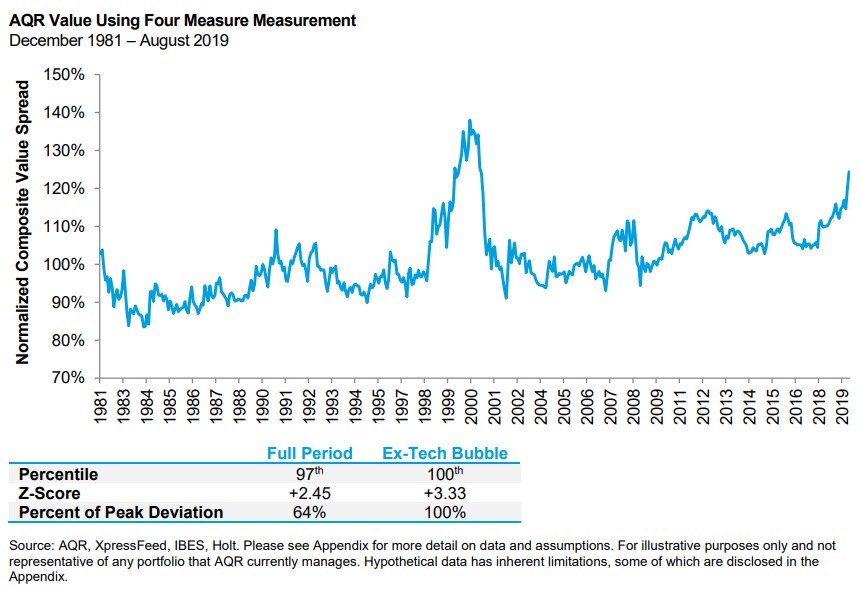

尽管这次下跌了50%,但2016年一年就VGPMX曾经上涨50%。从2011年至2015年,这只基金下滑了近75%。投资者经常会搜寻和大盘关联度低的资产,以便增加持仓多元性带来的好处。贵金属和矿业公司看来就属于这一类,但追逐无关资产有时意味着在市场其他领域都高歌猛进之际承担巨大的亏损。 价值股 当20世纪90年代末出现互联网泡沫的时候,成长股全面超越价值股,原因是投资者争相追捧“新经济”中的科技公司。在泡沫最大的时候,成长股和价值股的相对估值差距达到了历史最高点,用人们认可的几乎所有“价值”定义来衡量都是如此。而当泡沫消退时,价值股在随后几年里把成长股远远地甩在后面。 许多倾向于基本面的投资者都希望这种情况再次出现,原因是本轮周期中成长股又彻底击败了价值股。亚马逊、苹果、Netflix、谷歌和Facebook等高成长公司占据了投资者的心,乏味的老式价值股则被遗弃在了尘土中。 经过一段时间后,价值股的估值看起来终于够低了,至少对资本管理公司AQR的克里夫·阿斯尼斯来说是这样。他在近期发表的一篇研究报告中用多种价值指标说明成长股目前的估值已经非常高,仅次于互联网泡沫时期。阿斯尼斯写道:“除了科技泡沫阶段,价值股的价值已经降至历史最低点,差距相当大。” |

Those 50% losses are despite a 50% gain in 2016 alone. From 2011-2015 this fund was down close to 75%. Investors are often in search of asset classes with low correlation to the broad market to add portfolio diversification benefits. Precious metals & mining companies seem to fit that bill but the catch with uncorrelated assets is sometimes that means eating big losses while the rest of the market screams higher. Value Stocks During the dot-com bubble in the late-1990s, growth stocks stomped all over value stocks as investors rushed into technology companies in the “new economy.” By almost every accepted definition of “value”, growth stocks were more expensive than their value counterparts at the peak of that bubble on a relative basis than at any time in history. When the bubble deflated, value went on a huge run of outperformance over growth for years to come. Many fundamentally-inclined investors are hoping for a repeat of this situation as growth has once again decidedly beat the pants off value stocks during this cycle. High growth companies such as Amazon, Apple, Netflix, Google, and Facebook have attracted investor mindshare while boring old value stocks have been left in the dust. It’s taken some time but it looks like value stocks are finally getting cheap enough, at least according to AQR’s Cliff Asness. Using a number of different value metrics, Asness showed in a recent research piece that growth is more expensive now than at any time other than the dot-com bubble. Asness writes, “Excluding the tech bubble the value of value is the cheapest it’s ever been by a fairly decent margin.” |

|

当然,时机的选择总是上述问题中的难点。某只股票正在下跌绝不意味着它不会继续滑落一段距离。某只股票很便宜绝不意味着它不会变的更便宜。金融危机以来,能源股以及金属和矿业股持续遭受如此沉重的打击是有原因的——大宗商品价格本身大幅下跌,而通胀一直得到控制。价值型公司持续跑输成长型公司可能是因为软件正在“吞噬”这个世界,无形资产实现增长以及投资者在资本充足的环境下愿意为成长投入资金。 发生惨案时通常都会有绝佳的解释。每一类股票的暴跌都有原因。这就是当前局势让投资者如此困惑的原因。大家面临的选择是要么投资于基本面良好但价格高的资产,要么投资于基本面正在变差但价格低的资产。 对投资者来说,最困难的一点是决定自己是要自律,还是要发挥想象力,继续持有表现落后的投资。我猜那些一直手握能源股、金属和采矿公司以及价值股的人现在会觉得自己的想法有点儿虚幻了。时间会告诉我们,他们所坚持的想象能否带来回报。(财富中文网) 本文作者是注册金融分析师本·卡尔森(Ben Carlson),他是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。 译者:Charlie 审校:夏林 |

Of course, the hard part with these things is always the timing. Just because something is down, doesn’t mean it can’t go down some more. And just because something is cheap, doesn’t mean it can’t get cheaper. There’s a reason energy stocks and metals & mining shares have been hit so hard since the financial crisis—commodities prices themselves have been battered while inflation has been kept under control. And value companies have likely underperformed growth companies because software is eating the world, the growth in intangible assets, and the willingness of investors to pay up for growth in a world awash in capital. When there’s blood in the streets, there’s usually a perfectly good explanation for it. Each of these categories has a black eye for a reason. That’s what makes the current situation for investors so confusing. Your choices are (a) invest in assets with good fundamentals but high prices or (b) invest in assets with deteriorating fundamentals but low prices. One of the hardest things to do as an investor is determining whether you’re being disciplined or delusional by sticking with an underperforming investment. I’m guessing those who have stuck with energy stocks, metals & mining companies, and value stocks feel a bit delusional at the moment. Time will tell if their disciplined delusion will pay off. Ben Carlson, CFA is the Director of Institutional Asset Management at Ritholtz Wealth Management. |