投资基金要当心:过于看重业绩可能导致巨大亏损

|

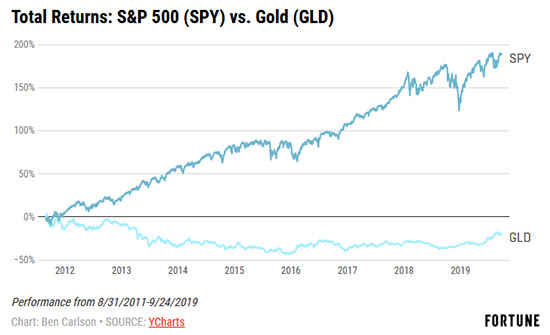

2011年8月,SPDR Gold Shares ETF (GLD)短暂超越S&P 500 SPDR ETF (SPY),成为资产最多的交易所交易基金。然而自那以后,这两大基金的投资业绩却有天壤之别。 |

In August 2011, the SPDR Gold Shares ETF (GLD) briefly surpassed the S&P 500 SPDR ETF (SPY) as the largest exchange-traded fund in terms of assets. Since then, the investment performance of these two funds are night and day. |

|

从2011年8月至今,S&P 500的总体回报约有190%的涨幅,而GLD的总体回报则比那个夏天的最高点低了近20%。成为全球第一的交易所交易基金本身没有什么魔咒,但这个荣誉却让GLD的资产严重流失。 |

The S&P 500 is up roughly 190% in total since the end of August 2011 while gold remains nearly 20% below its high watermark from that summer. There’s nothing magical about becoming the biggest ETF in the world but the aftermath of this honor was none too kind to the assets in GLD: |

|

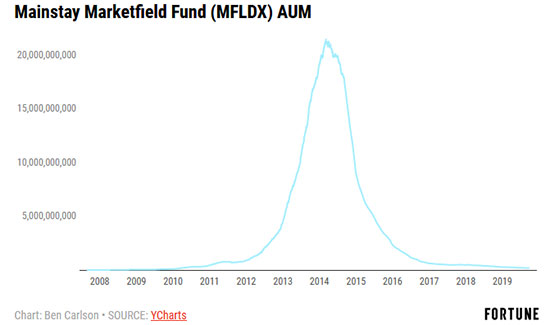

GLD的管理资产额从2011年夏末的超过770亿美元一路锐减到2015年年底的210亿美元。这一情况的有趣之处是,管理资产额比相关基金的业绩下滑更为严重。 GLD的管理资产在四年多一点的时间里缩水了72%以上,而GLD本身的业绩只下滑了43%。基金价格的跌幅已然相当巨大,但资金外流的严重程度还要更甚。 在GLD成为全球最大交易所交易基金的过程中,情况恰恰相反。从2007年到2011年8月,GLD的价格涨幅超过180%,但同期的资产却增长了近700%。其部分原因可能在于金融危机导致对冲系统性风险猛增,黄金成为许多人青睐的替代品。但很明显,追求业绩也在从中起到了推波助澜的作用。 基金表现良好,资产就会蜂拥涌入。基金一旦显出颓势,资产则会迅速逃离。这在基金领域不是什么新鲜事。过去一直有追求业绩的人,未来也同样如此。 SPY如今以超过2,700亿美元的资产获得了最大交易所交易基金的称号。令人惊讶的是,从2011年被GLD短暂超越至今,SPY的资产增长都来自于市场收益,而不是投资者的现金流。SPY的管理资产额自2011年8月至今仅有194%的增长,与基金总回报的增长率190%几乎持平。 指数基金和交易所交易基金无法避免追求业绩的影响,但更加非传统的资产类别和策略似乎会更多地面临投资者对业绩的追求。 自2008年股市崩盘之后,投资者迫切想要寻求能够减少股市风险或拥有不相干的较高预期回报的其他投资手段。流动资产领域几乎没有什么基金具备这样的前景,但却有一家基金由于业绩突出得到了投资者的关注。 Mainstay Marketfield Fund (MFLDX) 的投资收益相当丰厚,自2009年到2014年第一季度的回报率超过100%。这一时期,SPY的涨幅超过130%。不过另类基金可以切换资产类别,也有能力卖空证券,这保持了对投资者巨额资金的吸引。 MFLDX的资产从起初2009年的3,400万美元暴增到2014年年初的超过210亿美元。尽管基金业绩仅仅翻了一倍,资产却增长了600倍。沃伦·巴菲特曾经表示:“规模是出色业绩的大敌”,这句话对MFLDX同样适用。 从2014年第一季度起,MFLDX变得黯淡无光。到目前为止,美国股市上涨了近80%,而它的跌幅却超过11%。资金撤离了这只基金,就和它当初涌入时一样迅速。它的管理资产如今不足2亿美元,与2014年的高点相比跌幅达99%。 |

From a high of more than $77 billion in that late-summer of 2011, assets under management (AUM) in GLD fell all the way to $21 billion by the end of 2015. What’s interesting in this scenario is how much more AUM fell than performance in the underlying fund. Assets in GLD fell more than 72% in a little over 4 years while performance in GLD itself was only down 43%. That’s a fairly substantial crash in price but an even more substantial outflow in terms of assets. The flipside was true in the run-up to becoming the world’s largest ETF. From 2007 through August 2011, GLD was up more than 180%. But assets in the fund grew nearly 700% in that time. Some of this could have been due to the fact that the financial crisis created a flight to hedge systemic risk, of which gold is a favored proxy for many. But it’s clear there was also an element of performance chasing going on as well. When the fund performed well, assets poured in. And then when the fund performed poorly, assets fled. This is nothing new in the fund space. There have always been performance chasers and there will always be performance chasers. SPY now wears the crown as the largest ETF with more than $270 billion in assets. Surprisingly, the growth in assets for SPY since GLD passed it briefly in 2011 has come from market gains, not flows from investors. Assets under management in SPY have grown just shy of 194% since August 2011, not much more than the close to 190% total returns in the fund. Index funds and ETFs aren’t immune to performance chasing but the more non-traditional asset classes and strategies tend to see more performance chasing from investors. Following the market crash in 2008, investors were eager for alternative investments that would either hedge the stock market or offer an uncorrelated return stream with high expected returns. Few funds in the liquid alt space delivered on these promises but one fund did gain investor attention because of its performance. The Mainstay Marketfield Fund (MFLDX) saw strong returns, delivering a return of more than 100% from 2009 through the first quarter of 2014. The S&P 500 was up more than 130% in this time, but the fact that an alternative fund that switches between a number of asset classes and has the ability to short securities was able to keep up attracted huge inflows from investors. Assets in MFLDX exploded from just $34 million at the outset of 2009 to more than $21 billion by early-2014. So while fund performance merely doubled, assets were up 60,000%. Warren Buffett once said, “Size is the enemy of outperformance,” and the Marketfield Fund was no different. Since the first quarter of 2014, MFLDX has gone nowhere, losing a total of more than 11% up to now. U.S. stocks are up nearly 80% in this time. The fast money that poured into this fund fled just as fast as it came in. Assets are now under $200 million, down 99% from the highs in 2014. |

|

这就是一个效果惊人的追求业绩的案例。那些在金融危机中受到伤害,并在寻找疯狂股市替代品的投资者可能是罪魁祸首。市场变幻无常,而投资者也是如此。 追求业绩的历史悠久,这类行为永远不会消亡。任何时候都会有一些表现突出的基金或深奥的策略。不幸的是,大多数投资者往往在它们的强劲表现落幕之后才开始注资。(财富中文网) 本文作者是注册金融分析师本·卡尔森(Ben Carlson),他是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。 译者:严匡正 |

This was a performance chase of epic proportions, most likely caused by investors who were still somewhat scarred from the financial crisis and in search of an alternative to the stock market’s crazy ways. The market can be fickle but so are investors. Performance chasing is as old as the hills so this type of behavior is never going away. There will always be certain funds or esoteric strategies that do better than others at times. Unfortunately, most investors tend to put their money into these strategies only after they’ve already experienced strong outperformance. Ben Carlson, CFA is the Director of Institutional Asset Management at Ritholtz Wealth Management. |