本轮经济繁荣将告终,我们该怎么办?

Geoff Colivn

2018-07-29

经济增长放缓,牛市落幕,要做什么才能避免受到冲击?

文本设置

文本设置

Plus(0条)

Plus(0条)

|

夏日炎炎,商界对美国经济的乐观情绪也像烈日一样火爆。美国一流企业首席执行官协会Business Roundtable调查显示,今年6月美国大企业首席执行官信心爆棚,他们预计的企业营业收入和投资规模都超出3月的预期,信心值创该调查十五年来新高。首席财务官同样信心满满。四大会计师事务所之一德勤调查显示,首席财务官最近对北美经济的预期达到八年来最高水平。美国独立企业联盟报告显示,小企业领导者的乐观心态也达到了过去三十年来从未有过的高位。用一个比喻评价,美国商界上下一派歌舞升平、击钟鼎食的气象。 这种时候要让欢腾的舞步戛然而止似乎有些不尽人情。我们不会这么泼冷水。今年7月中旬,预测机构料将公布二季度GDP增长预期,即便他们预计美国经济至少未来几个季度仍会保持强劲增长也不意外。失业率正处于历史低位,就业前景向好吸引更多美国人重返劳动力大军。难怪商界领袖们如此有信心。 |

THE OPTIMISM IS BEAMING like the summer sun. America’s big-company CEOs are bursting with confidence, in June expecting to take in even more revenue and make bigger investments than they foresaw in March, when they were more confident than ever before in the 15 years the Business Roundtable has been surveying them. CFOs are just as ebullient. Their perception of the North American economy was recently the highest in the eight years Deloitte had been asking about it. Leaders of small businesses also are brimming with optimism—more than at any time in the past 30 years, reports the National Federation of Independent Business. At least figuratively, confetti is flying, disco balls are spinning, and Champagne corks are popping across the length and breadth of American business. It seems a shame to pull the plug on the dance music, so we won’t, exactly. As of mid-July, forecasters were expecting the announcement of a knockout GDP growth number for the second quarter, and it wouldn’t be surprising if the U.S. economy continued to grow impressively for at least a few quarters more. Unemployment is near historic lows, and better job prospects are drawing more workers back into the labor force. No wonder business leaders are confident. |

|

然而,经济走强的迹象掩盖了一些根本现实,这些现实问题不会逐渐消失,也不容忽视。股市上涨停滞等信号暗示,当前美国的经济扩张已接近尾声,而不是刚刚起步。我们稍后会介绍更多此类信号。对经济扩张的担忧已推升长期利率,不利于资产估值。贸易战影响的不确定性导致很多企业推迟行动,收缩潜在投资。事实上,歌舞升平氛围背后,经济的警告信号无处不在。美国经济增长迟早会大幅下滑,甚至衰退,而且可能比我们想象中来得快。一贯如此。 季节性变化将至 先从明显的迹象说起:经济是一个周期接另一个周期。不同于自然界的四季更迭、月盈月缺或是潮汐起落,商业周期的起止向来难以预测。某个时候经济活动会暂时走上巅峰,然后开始收缩,直至最终跌落最低谷,此后又开始回升。讽刺的是,判断我们处在增长期末尾的熟悉标志就是经济过热,有点类似印度的夏天:企业促使工厂生产,超出其长期可持续的水平,员工加班增加。需求非常强劲,通胀开始回升,导致央行加息,于是股价等资产估值趋平或者回落。全球最大对冲基金桥水基金的首席执行官瑞·达利欧指出:“这就是经济强劲时股票和其他资产价格往往下跌的原因。” 现状正是如此。美国国会预算办公室(CBO)发现,今年国内经济开始有过热迹象,产出超过了潜在的长期可持续水平。今年5月国会预算办公室预计,随着薪资上涨,越来越多劳动者将重返工作岗位。6月就是如此。人才市场供应继续吃紧,劳动者对找工作很有自信,自愿离职率创十七年来新高。同时,雇主可能为了吸引并留住优秀员工而不得不竞相加薪,这将直接打击企业盈利。 通胀和利率双双走高,国会预算办公室预计涨势可能持续。达利欧称,综合所有因素来看,“我们都很清楚现在处于商业周期的‘末期’。” 美国经济走到这一步经历了很长时间,从历史角度看,这种持久性不同寻常。包括上次衰退后的经济复苏阶段在内,美国经济扩张已经持续110个月,可以说相当长寿,如果在人类世界堪比年逾百岁的老人。根据美国国家经济研究所分析,这是164年来美国第二长的扩张期,期间美国经济扩张平均持续39个月。唯一一次超过当前扩张的时期是1991年到2001年,当时维持了120个月。 然而年迈未必意味着经济扩张将寿终正寝,但步入老年通常会出现一些状况。一旦开始衰老,就会整体崩溃。老年学专家称之为病变,常常和一些“并发症”相互关联。当前美国经济的繁荣表象之下,已埋伏很多病变。 劳动力不足 经济产出概念非常简单:由劳动力、资本和生产力组成的函数。很简单的一个事实是,如果劳动力增长非常缓慢,就像当前美国劳动力市场一样,经济很难快速增长。20世纪70年代,劳动力增速为每年2.6%,现在约为0.2%。原因之一是,几十年来,美国人生孩子越来越少(去年美国生育率降至历史最低水平)。随着婴儿潮一代不断老去并退出劳动力市场,美国工人数量将急剧下降。美国劳工统计局去年10月预测,2016年至2026年间将新增1150万个就业岗位,劳动力缺口达100万人。 为了应对人口减少的压力,美国公司依赖大量国外人才。2017年,移民占美国劳动力的17.1%,多年来该比例一直在上升。事实上,正如今年早些时候明尼阿波利斯联邦储备银行行长尼尔·卡什卡里在《华尔街日报》撰文提出,对美国来说吸引关键劳动力“像享受免费午餐一样”。 |

Yet all these signs of economic strength mask fundamental realities that won’t fade away and mustn’t be ignored. The current economic expansion is much nearer its end than its beginning, as accumulating hints suggest—including the stagnating stock market, about which we’ll say more in a bit. Already the concerns are pushing up long-term interest rates, which is bad for asset values. Uncertainty about the effects of a trade war is causing many companies to postpone action, dampening potential investment. Indeed, look past those disco balls and you’ll see economic warning signs everywhere. A significant slowdown or even recession is coming sooner or later, and it’s probably coming sooner than you think. It always does. A Seasonal Change is Coming LET’S START WITH THE OBVIOUS: Economies follow cycles. Unlike with seasons or the moon or the ocean tides, the timing of the business cycle is never easy to predict. But at some point, economic activity reaches a temporal peak, then begins to contract until eventually it bottoms out and starts growing once more. A familiar sign that we’re in the waning stage of the growing season, ironically, is that the economy overheats—think of it as an Indian summer: Companies push factories to produce more than their long-term sustainable output, pushing employees to work more overtime. Demand is so strong that inflation starts to increase, leading central bankers to raise interest rates, which causes asset values, including stock prices, to level off or fall. Ray Dalio, CEO of the world’s largest hedge fund, Bridgewater Associates, writes, “That is why it is not unusual to see strong economies accompanied by falling stock and other asset prices.” All of that is happening now. The Congressional Budget Office finds that this year, the economy has begun overheating in just this way, producing more than its sustainable longterm potential. The CBO predicted in May that as wages rose, more people who had left the labor force would come back to work, and, yes, that’s just what happened in June. The labor market continues to be tight, with workers so confident that they’re voluntarily quitting their jobs at the highest rate in 17 years. Meanwhile, employers will likely have to bid up wages in order to attract and keep good workers, hitting corporate earnings directly. Inflation and interest rates are rising and will likely continue to do so, forecasts the CBO. With all those factors combining, says Dalio, “We know that we are in the ‘late-cycle’ part” of the business cycle. It is somewhat remarkable, historically speaking, that it has taken this long to get here. America’s current expansion is 110 months old (including the recovery period after the last recession), which makes it a marvel of longevity—the economic equivalent of a supercentenarian. The current growth run is the second longest in the 164 years for which the National Bureau of Economic Research has done the analysis; the average expansion has run a mere 39 months. The only one that outlasted this one lived to be 120 months old (1991–2001). Old age isn’t by necessity a death knell for an expansion—but then, there is something that tends to accompany it: When things start to break down, they break down en masse. Gerontologists call these tandem and often interlinked pathologies “comorbidities.” And in this economy, just under the skin, there seem to be plenty of them. We Don’t Have Enough Workers ECONOMIC OUTPUT is pretty straightforward in concept: It’s a function of labor, capital, and productivity. The simple fact is, it’s hard for an economy to grow very fast if the labor force is growing very slowly, as the U.S. labor force is doing. In the 1970s, it increased at a 2.6% annual rate; now the rate is about 0.2%. One reason for this is that for many decades, Americans have been having fewer and fewer babies (the U.S. fertility rate dropped to a new all-time low last year). As the baby-boom generation continues to age and exit the workforce, the number of American-born workers will sharply decline. This past October, the Bureau of Labor Statistics projected that over the period of 2016 to 2026, there will be 11. 5 million jobs created and a million fewer people in the workforce to fill them. To counter that demographic drag, American companies have relied on an influx of people from outside the country. Immigrants accounted for 17.1% of the U.S. workforce in 2017, a percentage that has been rising for years. This critical labor force infusion, in fact, has been “as close to a free lunch as there is for America,” as Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, put it earlier this year in an op-ed for the Wall Street Journal. |

|

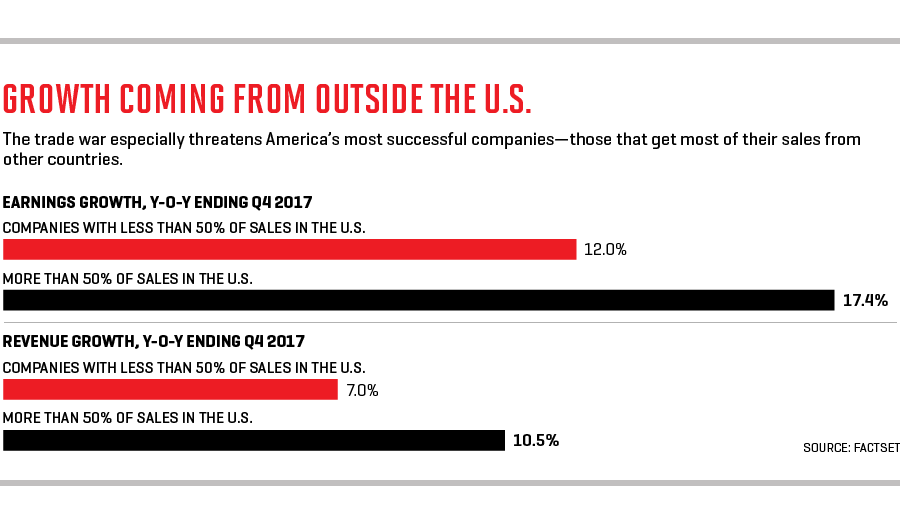

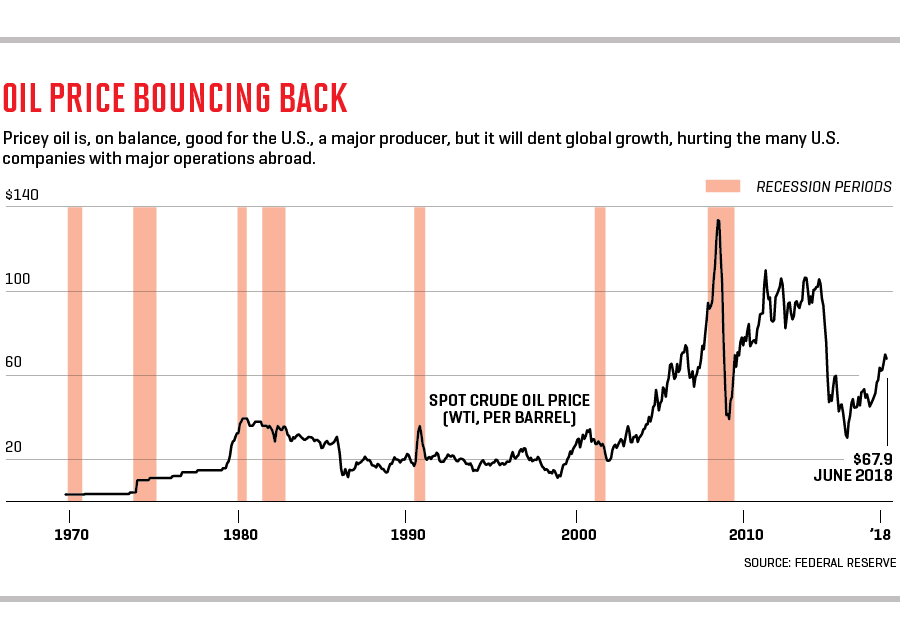

然而很少有人知道,补充劳动力实际上也面临全球竞争。没错:其他出生率下降的发达国家同样需要新工人弥补退休人员留下的岗位。之前美国一直占据优势,不仅能吸引到低薪工人填补美国人不愿做的工作,还吸引到大批科学家和企业家。(硅谷就有座加拿大政府购买的广告牌,建议签证有问题的技术人员“转向加拿大”。)这就是为什么特朗普总统的移民很可能会限制美国公司发展——移民方面的强硬政策不仅是政治立场,也是经济政策。 到目前为止,美国的移民打击并未显着减少净移民人数,但其中复杂的风险可能对美国企业产生深远影响,不管规模大小。 贸易战令其他问题情况更糟 仅看特朗普政府移民政策的话,可能不会影响经济增长。但联邦政府另一项政策在边境制造更多麻烦,而且这次是跟长期贸易伙伴。即便美国与中国、欧洲、加拿大和墨西哥之间新一轮贸易战不会持久,也会与老龄化一样成为不良影响。据FactSet报道,去年大部分业务在海外的美国公司比其他同行增长速度更快,盈利能力也更强。因此,发动贸易战会严重影响美国最强劲的经济增长引擎。 从数据来看,目前与贸易有关的冲突在美国每年20万亿美元的经济中无关紧要。即使7月初美国对340亿美元中国商品征税引发报复反应,也不会显著降低GDP。但相关影响会以两种相互交织的方式迅速出现。 首先,战争规模再大通常也会从小型战斗开始,之后引发不断升级循环。当前贸易战似乎还在发展过程中。美国针对中国的行动3月开始,当时特朗普对进口铝和钢铁征收关税,其中只有约27亿美元来自中国生产商。中国随即对同等数量的美国出口征收新关税。第二天,特朗普提出对500亿美元中国产品征收关税;第二天中国也报复性征收关税。双方龃龉一直持续,现在美国威胁对5000亿美元的中国进口产品征收关税,中国则发誓要“不惜一切代价”实施报复。 随着赌注越来越高,言辞也愈发激烈。6月特朗普表示,中国“威胁到没有做错任何事的美国公司、工人和农民”。中国商务部斥责该言论为“勒索”。最新的关税于7月生效时,中国一份党报警告称,“美国显然低估了全球反对力量和中国发动报复时能发挥多大能量”。 随着公开威胁日渐明确,退一步的可能性越来越小。推动全球经济增长的两大经济体喋喋不休地争吵,可能发展为一场历史性的贸易战。 争端还可能以另一种方式影响美国经济,即便双方对抗不激化一样会实现。问题在于人们会对未来发展不确定。正如美银美林经济学家米歇尔·梅耶在最近一份报告中提到,该影响——即“不确定性引发震荡”已经发生,美联储很担心。联邦公开市场委员会在6月会议上报告称,“由于贸易政策存在不确定性,部分地区资本支出计划已缩减或推迟”,并补充称“大多数参与者”担心不确定性会影响“商业情绪”或商业信心,以及“投资支出”。 别指望局势很快会明确。谁也没法预测大规模贸易战会怎么发展。上一次贸易战还是20世纪30年代,当时可没有现在这般复杂快速的全球供应链。商业决策者对最终结果也只能猜想。 不确定性会导致一切停摆,这对增长没有好处。 油价上涨将阻碍全球发展 另一个威胁则是油价高企,经常也差点登上新闻头条新闻。最近油价为每桶约73美元,由于美国也是化石燃料主要生产国,所以油价上涨对美国有直接好处,但油价过高也很可能削弱全球增长,因为随着美元走强,石油(无论出自哪国) 对其他国家来说成本更高。 |

What’s less widely understood is that there has actually been a global competition for this supplementary workforce. That’s right: Other developed nations with declining birthrates likewise need new workers to help offset their armies of retirees—and America has been winning this battle, luring not just low-wage workers to fill jobs that native-born Americans aren’t rushing to do but also scientists and entrepreneurs. (Witness the Silicon Valley billboards, bought by the government of America’s northern neighbor, imploring techies with visa troubles to “Pivot to Canada.”) That’s why President Trump’s immigrant-hostile policy isn’t just a political stance, it’s also an economic one—and one that’s almost sure to limit the ability of U.S. companies to grow. So far, America’s immigration crackdown has not significantly reduced net in-migration, but it’s a compounding risk that could have far-reaching consequences for American businesses large and small. A Trade War Makes Other Problems Worse BY ITSELF, the Trump administration’s immigration policies may not be enough to stop growth in its tracks. But another federal policy is making even more trouble at the border—this time with America’s long-standing trading partners. Nascent trade wars with China, Europe, Canada, and Mexico—even if they don’t last—have become yet another comorbidity for our aging expansion. U.S. companies that do most of their business abroad grew faster and were more profitable than the rest last year, just as in previous years, FactSet reports. Waging a trade war thus disproportionately hurts America’s strongest engines of economic growth. By the numbers, the trade-related skirmishes so far are insignificant in America’s $20 trillion-a-year economy. Even the tit-for-tat imposition of tariffs on $34 billion of trade by the U.S. and China in early July will not, by itself, noticeably reduce GDP. Yet the effects could easily mushroom, in two intertwined ways. First, even the biggest wars typically start with minor battles that spark an unstoppable cycle of escalation. In the current trade war, that appears to be underway. Hostilities with China began in March when President Trump imposed tariffs on aluminum and steel imports, only about $2.7 billion of which come from Chinese producers. China responded with new tariffs on an equivalent amount of U.S. exports. The next day, Trump proposed tariffs on $50 billion of Chinese imports; China proposed retaliatory tariffs the day after that. On and on this went until the U.S. has now threatened tariffs on nearly all of America’s $500 billion of Chinese imports, and China has vowed to retaliate “at any cost.” As the stakes get higher, the rhetoric gets more bellicose. China is “threatening United States companies, workers, and farmers who have done nothing wrong,” Trump said in June. China’s Trade Ministry called the speech “blackmail.” When the latest tariffs took effect in July, a Chinese Communist Party newspaper warned that “Washington has obviously underestimated the giant force that the world’s opposition and China’s retaliation can produce.” As public threats become more explicit, backing down from them appears ever less likely. That’s how a piddling spat between the world’s two largest economies, jointly the foundation of global economic growth, could become a historic trade war. But the second way the current dispute could damage the U.S. economy doesn’t even require that hostilities get worse. It requires only that people become less certain about where all this is headed. That effect—an “uncertainty shock,” as Bank of AmericaMerrill Lynch economist Michelle Meyer called it in a recent note—is happening already, and it worries the Fed. “Contacts in some Districts indicated that plans for capital spending had been scaled back or postponed as a result of uncertainty over trade policy,” the Federal Open Market Committee reported from its June meeting, adding that “most participants” were concerned such uncertainty could depress “business sentiment”—confidence, that is—“and investment spending.” Don’t expect much more clarity anytime soon. No one can predict where a large-scale trade war would lead. The last one occurred in the 1930s, when today’s intricate, light-speed global supply chains would have been nearly unfathomable. Which leaves business decisionmakers only to wonder how all this shakes out. Uncertainty prompts paralysis—and that’s no good for growth. Rising Oil Prices Will Gum Up Global Gears ANOTHER THREAT—this one lingering just below the top news headlines—is the high price of oil. Recently around $73 a barrel, it’s on balance a direct benefit to the U.S. now that America is a prodigious producer of the fossil fuel—but expensive oil is also very likely to dent global growth, particularly since the strengthening dollar makes oil (wherever produced) yet more costly for other countries. |

|

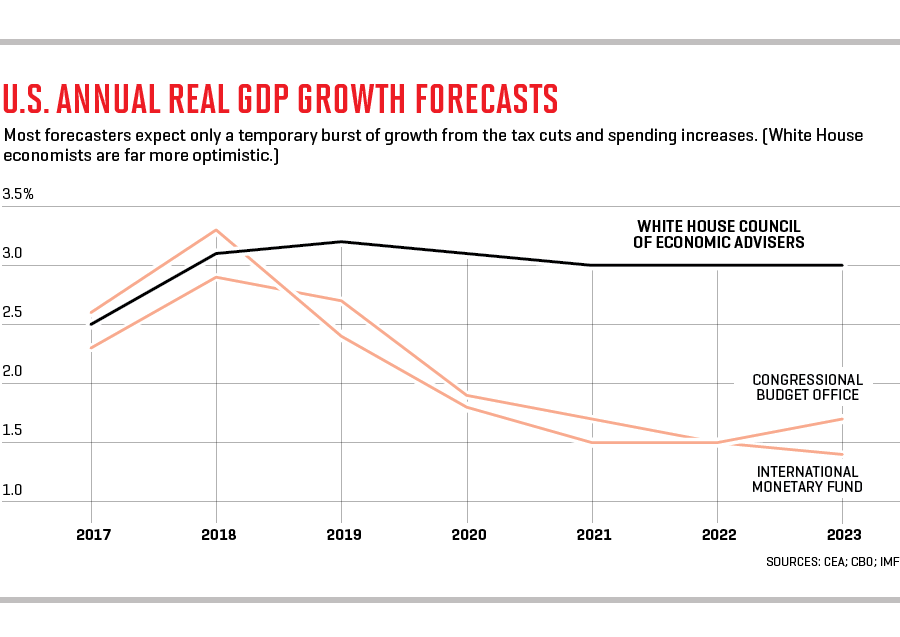

经济合作与发展组织(OECD)是以促进全球经济增长为目标的政府间机构,该机构指出,高油价是主要的“重大风险”之一。尽管某些人可能认为美国不必在意全球经济普遍放缓,但油价走高终将有损美国大公司和许多小公司的利益。 刺激政策可能会短暂推动经济增长... 正如我们指出,经济衰退和承压的迹象似乎反映出上一个商业周期终结。但有个很重要的反证,因为我们多次听说最近联邦政府减税和支出增加。一些经济学家表示,令人兴奋的刺激计划将避免经济衰退,不仅如此,未来几年还会推动迅速增长。 实际上,从所有传统标准看,经济增长都堪称亮眼。经过多年低速扩张,2018年可能是十年内GDP增长最强劲的一年。但不能指望刺激来保持刺激。 西北大学经济学家罗伯特·J·戈登在最新著作《美国经济增长的兴衰》里的观点相当有说服力,他指出美国从1870年到1970年的“特殊世纪”是“独特的高速增长期,以后无法重复。”他说,以前人们认为GDP增长3%很正常,但已不可持续。然而,减税和增加支出营造的“旧式财政刺激”将推动短暂强劲的增长,“至少一段时间内增长3%以上”,而且“未来四到六个季度平均增长3%”。 他表示,“然后刺激政策效应逐渐消失。”经济回到缓慢增长的新常态。 |

The Organization for Economic Cooperation and Development, an intergovernmental agency aimed at fostering economic growth worldwide, points to high oil prices as one of the main “risks that loom large.” And while a broad global slowdown may seem, to some, removed from U.S. interests, it would hurt America’s biggest companies and many of its smaller ones as well. The Stimulus May Pad Growth For A While… THE SIGNS of economic senescence and stress, as we noted, would seem to mirror the end of past business cycles. But there’s one big counterpoint, as we’ve all heard many a time, and that’s the recent federal tax cut and spending increases. That whammy of a stimulus, say some economists, will stave off any recession—and not only that, it will jumpstart growth for years to come. Indeed, the economy, by all traditional measures, seems to be growing smartly. After years of low-horsepower expansion, 2018 could be the best year for GDP growth in at least a decade. But don’t count on the stimulus to keep stimulating. Robert J. Gordon, the Northwestern University economist whose latest book is The Rise and Fall of American Growth, argues persuasively that America’s “special century” from 1870 to 1970 represented “a singular interval of rapid growth that will not be repeated.” Regular yearly GDP growth of 3%, once considered normal, is no longer sustainable, he says. Yet “old-fashioned fiscal stimulus” from tax cuts and a spending boost will produce a brief but powerful blast of growth—“3%-plus growth for at least a while” and “an average of 3% growth probably for the next four to six quarters.” Then, he says, “the stimulus fades away.” And it’s back to the slow-growth new normal. |

|

当然,一切假设短期内经济会出现提升。然而可能不会。出于多种原因,刺激措施可能无法像宣传中一样发挥作用。首先,减税和支出增加等财政启动通常在商业周期底部部署,而不是顶部。旧金山联储研究人员在一项新研究中表示,相关政策对不断增长的经济体影响不大。有证据表明,“实际提升作用可能远远低于许多人预计”,可能“接近零”。 美联储前主席本·伯南克则预计,近期将出现巨大变化。他在最近的华盛顿政策讨论中表示,刺激计划“选了个非常错误的时机”。(他拒绝了采访。)“经济已经充分就业。”刺激措施“今年和明年将对经济造成重大打击,2020年也是。总有一天大笨狼怀尔狼(动画片角色)会发现自己站在悬崖边双脚踩空。” 此外,许多公司将省下来的税款用于股票回购,而不是投资经营。股东可能很高兴,但从长远来看不会刺激经济增长。我们认为,虽然刺激措施可能会推进经济扩张,但很像把汽车油门踩到底。一段时间里速度非常快,甚至可能令人兴奋,但很快汽油就会耗尽......或者撞车。 ......然后情况可能更糟 值得注意的是,刺激还会产生另一种影响:国会预算办公室宣称,比起没有近期减税和支出增加的情况,未来十年累计的联邦赤字将增加1.6万亿美元。如果各种税收和支出条款结束时国会决定继续的话,赤字规模可能更大,现在看起来可能性很高。这点很令人担心,具体来说有多个原因(正如《财富》杂志的记者肖恩·塔利在2018年4月1日发表的《深陷债务》里提到)。下一次经济衰退不可避免地到来时,华盛顿就无法采用通常的减税和增加支出的手段补救。如果债务不断膨胀让外国投资者感到害怕,购买美国国债减少,利率只能上升,联邦利息支付将会增加,在恶性循环中债务更快扩张。 许多公司已过度杠杆化 虽然人们对联邦债务日益增长的威胁已经讨论很多,但另一项基本被忽视的信用风险中也出现了麻烦:企业债务。非金融公司债务已经上升到GDP的73.5%,创历史新高,却没引起太多关注。 目前来看问题并不是很严重,因为利率一直很低,这也是公司大量借贷的重要原因之一。但随着利率上升,美国公司生存环境日趋恶劣。标普国际信贷分析师安德鲁·张表示,如果利率上升而经济放缓,也就是双重打击齐下的话,眼下创纪录的企业债务“将成为大问题。”现在看起来发生的可能性越来越大。“人们能意识到风险,但行动起来并不是很规矩。”他告诉《财富》杂志。公司债的投资者越来越紧张。投资级公司债是今年上半年表现最差的债券。 |

That, of course, assumes we’ll get that short-term boost. We may not. The stimulus may not work as advertised for a number of reasons. First, fiscal fire-starters like tax cuts and spending increases are usually deployed at the bottom of the business cycle, not the top. They just don’t add much oomph to an economy that’s already growing, say researchers at the San Francisco Fed in a new study. The evidence suggests that “the true boost is likely to be well below” what many forecasters predict and could be “as small as zero.” Former Fed chairman Ben Bernanke foresees a more dramatic near future. The stimulus is arriving “at the very wrong moment,” he said at a recent Washington policy discussion. (He declined an interview request.) “The economy is already at full employment.” The stimulus “is going to hit the economy in a big way this year and next year, and then, in 2020, Wile E. Coyote is going to go off the cliff.” What’s more, many companies are spending their tax bonus on share buybacks rather than investing it in operations. That may make shareholders happy for a while, but it’s not going to stimulate economic growth over the long haul. Our take is that while the stimulus might extend this expansion, it’s a lot like flooring the accelerator in a car. For a time, you go really fast, and it might even be thrilling—but pretty soon you run out of gas … or crash. …And Then It May Make Things Worse THE STIMULUS, it’s important to note, will have another effect as well: The accumulated federal deficit over the next decade will be $1.6 trillion larger than it would have been without the recent tax cuts and spending increases, according to the CBO—and it will be larger still if various tax and spending provisions set to end are renewed by Congress, as seems highly likely. That’s concerning for all kinds of reasons (as Fortune’s Shawn Tully showed in “Deep in Debt,” April 1, 2018). When the next recession inevitably arrives, Washington will be less able to apply the usual remedies of lower taxes and greater spending. If ballooning debt eventually spooks foreign investors into buying fewer Treasuries, rates will have to rise and federal interest payments will grow, expanding the debt even faster in a bad-news feedback loop. Many Companies Are Already Overleveraged WHILE MUCH has been said about the growing menace of federal debt, trouble is brewing as well in a different and largely overlooked credit risk: corporate debt. Without many alarm bells sounding, the debt of nonfinancial companies has risen to 73.5% of GDP—an all-time high. It hasn’t been a problem so far because interest rates have been so low—which is a big reason companies borrowed so heavily in the first place. But as interest rates rise, the Goldilocks environment is darkening. Today’s record corporate debt “would be a problem if rates are rising while the economy slows—a double whammy,” says S&P Global credit analyst Andrew Chang. That’s exactly the scenario that is beginning to seem more likely. “People are aware of the risk but not quite behaving like an aware citizen,” he tells Fortune. Investors in corporate bonds are getting nervous. Investment-grade corporate debt was the worst-performing category of debt investment in this year’s first half. |

|

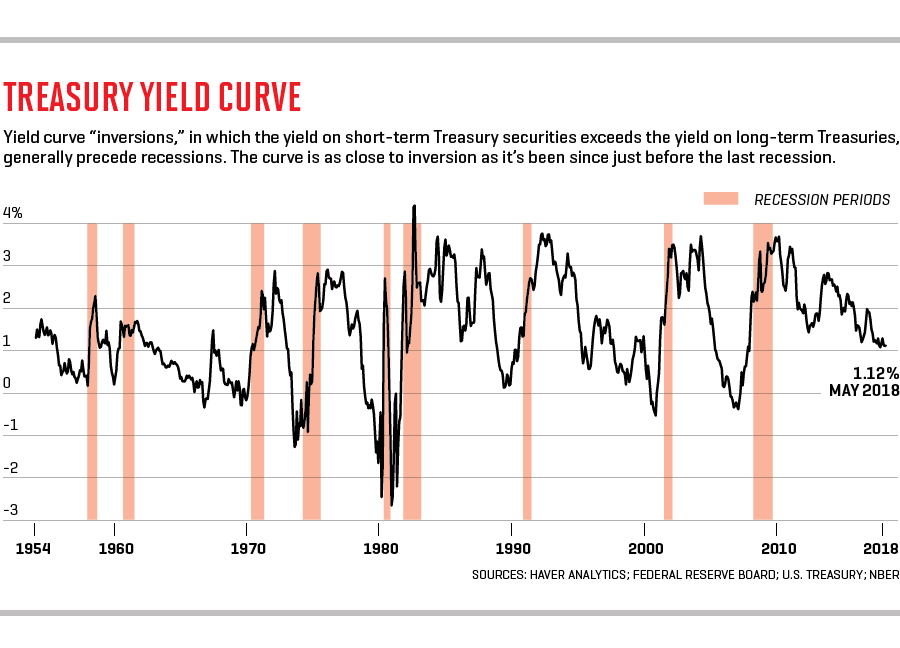

一些债券持有人指出,美国公司持有近2万亿美元的现金,以此来自我安慰。但该说法有两大漏洞。首先,24家大公司占据了庞大现金储备的一半(领头的是苹果公司,现金达2670亿美元),但这些公司的债务可占不到总体的一半。 其次,企业美国的净债务,即债务减去现金规模仍然达息税折旧及摊销前利润的1.5倍(即扣除利息、税收、折旧和摊销后的利润)。债务收益率达到过去15年来最高。“现金可能处于历史最高水平,但债务也一样,”标普国际的张表示,“人们却没注意到债务部分。” 情况已经相当严重,连美联储都开始留意了。今年4月,美联储理事莱尔·布雷纳德表示,“我们梳理了金融脆弱性后发现,两个领域风险上升:资产估值和商业杠杆。”两种风险都与公司债务有关。布雷纳德指出,公司债券的收益率“比历史水平低”,意味着当前债券价格非常高。而且与债务收益率一样,商业杠杆“相对于历史水平来看很高”。 明白了么?如果没完全理解,看看负责评估美国金融稳定性的财政部金融研究办公室的评论,可能会清楚一些:“非金融业务杠杆率......在潜在漏洞的热力图上已变红色”。 这一不良趋势也引发央行人士担心,因为有时只要出现小波动就能导致一连串公司破产。正如布雷纳德观察,“利润受到意外负面冲击加上利率提升”可能会打击一系列债券以及出贷方。如果真的发生,不仅会对债券市场造成压力,还可能影响整体经济。 可靠的指标正在下降 紧盯债务及其成本很有必要,因为债券利率在预测经济衰退方面向来很准,现在也快要预测出下一次衰退。如果长期(10年期)国债收益率低于短期(三个月)国债收益率,也即收益率曲线倒挂,就说明衰退不远。过去的50年里,该指标从未漏报也未误报过经济衰退。收益率曲线倒挂就意味着经济衰退,唯一的问题距离经济衰退开始还有多少时间;平均而言是10个月,不过2008-09经济衰退之前有16个月。 Haver Analytics的数据显示,截至7月中旬,收益率曲线尚未倒挂,但已非常接近,比2008年金融危机和经济衰退之前还要接近。 |

Some debt holders try to comfort themselves by noting that U.S. corporations are sitting on nearly $2 trillion of cash. But that reasoning faces two big holes. First, just 24 companies account for about half of that mammoth cash cache (led by Apple, with $267 billion), yet they account for nowhere near half of America’s corporate debt. Second, corporate America’s net debt—that is, debt minus cash—is still about 1.5 times Ebitda (earnings stripped away from interest, taxes, depreciation, and amortization). That would make it the highest debt-to-earnings ratio in the past 15 years. “Cash may be at an all-time high, but so is debt,” says S&P Global’s Chang, “and people aren’t noticing the second part.” The situation is serious enough to grab the Fed’s attention. Fed governor Lael Brainard, speaking in April, said, “Our scan of financial vulnerabilities suggests elevated risks in two areas: asset valuations and business leverage.” Both risks involve corporate debt. Brainard noted that yields on corporate bonds are “low by historical comparison,” meaning the bonds look awfully expensive. And business leverage, like that debt-to-earnings ratio, is “high relative to historical trends.” Got all that? Well, if not, maybe this comment from the Treasury’s Office of Financial Research—the arm of the department that assesses U.S. financial stability—can bring home the message: “Nonfinancial business leverage ratios … are flashing red on the heat map” of potential vulnerabilities. Those trends trouble central bankers because all it takes is a single jolt, in some cases, to create a cascade of corporate havoc. As Brainard observed, “unexpected negative shocks to earnings in combination with increased interest rates” could hammer those bonds and the lenders who own them. If that happens, it won’t just stress the bond market. The effects could ripple through the whole economy. Reliable Indicators Are Pointing Down FOCUSING ON DEBT and its cost is wise because bond interest rates boast an excellent record of forecasting recessions—and they’re close to predicting one now. When the yield on long-term (10-year) Treasury securities falls below the yield on short-term (threemonth) Treasuries—an inversion of the yield curve—a recession is on the way. Over the past 50 years, this test has given no false positives or failed to signal a coming downturn. Yield curve inversion has always equaled recession, and the only question is how long it will be before the recession starts; on average, it’s 10 months, though it took 16 months before the 2008–09 recession. As of mid-July, the yield curve had not inverted, but it was getting close—closer than it has been since just before the 2008 financial crisis and recession, according to Haver Analytics. |

|

另一个可靠的衰退指标则令人惊讶。当前失业率处于低谷,这有点反常,因为低失业率表明经济在强劲增长。但超低失业率也意味着扩张接近极限。过去65年里该指标从未出错,也从未误报。 复杂的是,只有低谷过去我们才能确定。今年5月失业率创下了17年来的最低点3.8%,然后在6月上升至4%,因为更多工人重新开始找工作。到底是不是失业率低谷,至少还得过几个月才能知道。但就目前而言,我们只能说我们比较接近。 市场和经济不可避免地转向时,会像所有变化一样变成机会。 除了知道哪些指标最能预测经济衰退,我们还知道不应该问谁:经济学家。至少在这项任务上,他们很糟糕。多年以来,全球各地的经济学家从未在经济衰退几个月前成功预测。奈德·戴维斯研究公司发现,美国“1970年以来的七次经济衰退中,经济学家预测全体失败”。实际上,经济学家从来“预测”不到衰退,直到衰退到来才知道。而且即便衰退开始他们也会低估下降趋势,只能不断修改预测,一直拖到经济衰退结束前不久才能说对。经济学家在帮助人们了解经济运作方式方面有些贡献,但在预测经济衰退上真的很差。 这点很重要,因为这意味着经济衰退到来之前专家不会预告,也就意味着你得自己做好准备。 分析师还在幻想 在此背景下,华尔街分析师似乎沉浸在乐观情绪里无法自拔。过去70年中,美国企业利润年复合增长率为5.6%。在史上最大牛市,即1982年到2000年间,利润增长率为6.5%。然而华尔街分析师认为标准普尔500指数公司利润还能以每年15%飙升,不是几个季度,而是未来五年内。 有史以来最伟大的投资者之一,约翰·邓普顿说:“牛市出于悲观主义,在怀疑中成长,在乐观情绪里成熟,最终在兴奋中消亡。”当前的乐观情绪像是兴奋,不客气的说就是精神错乱。 想预测市场拐点很愚蠢,没人知道未来半年或12个月股票走势怎样。即使当前价格太高,市场也不一定会暴跌。也可能长期滞涨,直到利润赶上价格。 |

Another highly reliable presage of downturns is surprising. It’s a trough in the unemployment rate—counterintuitive because low unemployment shows that an economy is growing strongly. But super-low unemployment also means the expansion is pressing up against its limits. In the past 65 years, this indicator has never missed and has never called a false positive. Complicating such a call is the fact that we can’t be sure a trough has occurred until after the fact. Unemployment hit a 17-year low of 3.8% in May, then edged up to 4% in June as more workers rejoined the labor force looking for jobs. Whether that turns out to be a bottom won’t be known for at least a few more months. For now, though, we can only say it’s hard to believe we aren’t at least very near one. When the markets and the economy inevitably do turn, it will be, like all change, an opportunity. In addition to knowing which indicators are best at predicting recessions, we also know whom not to ask: economists. At least on this one task, they’re terrible. Around the world, over long periods of time, the consensus of economists has consistently failed to predict recessions even a few months before they begin. Ned Davis Research finds that in the U.S., “economists, as a consensus, called exactly none” of the seven recessions since 1970. In fact, economists typically do not “forecast” a recession until after it has started, and even then they initially understate the decline, revising their estimates until finally getting them right shortly before the recession ends. Economists are highly valuable in helping the rest of us understand how the economy works, but they’re notably reluctant to predict downturns. This is important to remember because it means the experts won’t tell us a recession is coming until it’s already here. Which means it’s up to you to prepare for it. (For some help, see the sidebar “Where to Invest When the Party Ends” on the next page.) Analysts Are In Fantasyland AGAINST THAT BACKDROP, Wall Street analysts seem utterly clueless in their optimism. Consider that over the past 70 years, U.S. corporate profits have grown at a 5.6% compound annual rate. During the greatest bull market in history, from 1982 to 2000, they grew at 6.5%. Yet Wall Street analysts believe the profits of the S&P 500 companies will rage ahead at a searing 15% annual pace—not for a few quarters, but over the next five years. One of the all-time great investors, John Templeton, said, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” This sounds like euphoria, or what we might less politely term insanity. Trying to call turns in the market is folly, and there’s no telling how stocks might perform in the next six or 12 months. Even if today’s prices are in fact far too high, the market need not plunge. It could just stagnate until profits eventually catch up with prices. |

|

两位顶尖投资者认为,市场回归理性之前甚至可能短期再涨一波。瑞·达利欧就在观察“股价最后冲刺”,他认为这是构成“经典顶部”的关键元素。基金经理杰里米·格兰瑟姆曾提前发现网络泡沫和房地产泡沫,他称之为“崩盘”,最后全场疯狂买入,标志着牛市终结。1999年最后三个月就是个戏剧性的例子。 牛市如何结束以及何时结束基本无法预计,但种种迹象表明,步入第10年的牛市已临近终点。达利欧和其他经验丰富的投资者都表示,找不到值得买入的股票。CNBC最近一期百万富翁调查显示,富裕的投资者正撤出股市,转向现金或准现金投资。耶鲁大学诺贝尔经济学奖获得者罗伯特·希勒定期调研投资者,询问其对股票估值没有过高有多少信心;最新数据是自1999年以来最低水平。 然而,华尔街分析师毫无撤退的意思。“有点像1928年的情形,”席勒说。“乐观情绪太浓厚,感觉要去破坏气氛都有点不爱国。” 所以不光要小心,还要准备 股市泡沫、经济指标下行、金融稳定性亮起红灯,还有贸易战等等……要担心的事情太多。这并不一定意味着灾难即将来临。从现状来看,股市可能像格兰瑟姆说的一样恢复上涨甚至“崩盘”。今年经济可能会明显增长,但不用多想也该感觉紧张了。除经济顾问委员会,似乎没人相信长期来看GDP可以增长3%,即便最近的刺激措施能推动增长,以后也会付出代价。经济周期尚未消失,证据显示我们处于一个周期的后期。我们最好为下一次经济衰退做好准备,因为衰退真正来临时经济学家还是预测不出来。 当市场和经济不可避免地转向时,会像所有变化一样变成机会。不光股票会恐慌抛售,公司经理也要记住,经济状况不好时各行业的竞争状况比经济好时变化更大。 头脑清醒的投资者和领导者很早就面对现实,所以能安然度过低迷期。而且在经济状况好的时候,他们就已未雨绸缪。(财富中文网) 本文的另一版本刊载于2018年8月1日《财富》杂志,标题为《终结即将来临》。 译者:Pessy 审校:夏林 |

Two of the best investors alive think there’s even a chance of a brief market leap before sanity returns. Ray Dalio is watching for “one last spurt in equities prices,” which he considers a key element of “the classic top.” Fund manager Jeremy Grantham, who spotted the dotcom and housing bubbles well in advance, calls it a “melt-up,” a final, rapturous delirium of buying that signals a bull market’s decisive end. See the last three months of 1999 for a dramatic example. Exactly how and when a bull market will expire is unknowable, but signs are piling up that this bull market, now in its 10th year, has about run its course. Dalio and other sophisticated investors say they can’t find stocks worth buying. CNBC’s latest Millionaires Survey reveals that rich investors are moving out of stocks and into cash or near-cash investments. Nobel Prize–winning economist Robert Shiller of Yale regularly surveys investors on their confidence that stocks are not overvalued; the latest reading is the lowest since 1999. Yet those Wall Street analysts are having none of it. “It’s kind of like we’re in 1928 at the moment,” says Shiller. “There’s still all this optimism and a sense that it would be unpatriotic to disturb it.” So Don’t Just Beware, Prepare FROTHY STOCKS, economic indicators pointing down, financial stability flashing red, trade war, and more—it’s a lot to worry about. It doesn’t necessarily mean calamity is just ahead. For all we know, stocks could resume rising or even “melt up,” as Grantham says. The economy may well grow impressively this year. But we don’t have to look much further out to get more nervous. No one except the Council of Economic Advisers seems to think GDP can grow at 3% over the long term, and if the recent stimulus turbocharges growth, it does so at a price that will have to be paid afterward. The economic cycle hasn’t been abolished; all evidence says we’re in the latter stages of one. And we had better be ready for the next recession, because when it arrives, economists will not have predicted it. When the markets and the economy inevitably do turn, it will be, like all change, an opportunity. Stocks will be on sale, and corporate managers should remember that the competitive order in any industry always changes more in adversity than in smooth sailing. Clearheaded investors and leaders come through downturns fine because they confront reality early—and in the best of times, they prepare for the worst. A version of this article appears in the August 1, 2018 issue of Fortune with the headline “The End is Near.” |

请打开财富Plus APP