美联储主席鲍威尔:美国楼市泡沫期结束

2005年的时候,美联储主席格林斯潘曾对国会表示:“美国整体上不太可能出现房价泡沫。”但是事实上,当时房地产泡沫不但已经形成了,而且就在格林斯潘在国会传达这一信息时,泡沫已接近了顶峰。

时间快进到2022年,正是因为大家对上次泡沫心有余悸,所以这一次,经济学家们并不害怕承认泡沫的存在——即便他们觉得这次泡沫或许没有上一次那么危险。

上周二,全世界最有影响力的经济学家就是这样做的——美联储主席杰罗姆·鲍威尔在布鲁金斯学会的一次活动中表示,美国在疫情期间的房价上涨就符合“房地产泡沫”的定义。

“由于疫情的缘故,当时的抵押贷款利率非常低,人们都想买房,而且是想离开城市,在郊区买房,所以美国确实出现了房地产泡沫,房价上涨到了非常不可持续的水平,出现了过热等问题。所以,现在的房地产市场将迎来泡沫的另一阶段,希望它的供需关系能达到一个更好的状态。”鲍威尔说。

结合鲍威尔以往的发言,美国房地产的“平衡”进程应该已经开始了。今年6月份,鲍威尔曾表示,抵押贷款利率的大幅上涨将有助于“重置”美国的房地产市场。9月份鲍威尔曾对记者表示,美国已经正式进入了一个“艰难的房地产市场调整期”,它将恢复市场的“平衡”。

在鲍威尔承认有“泡沫”之前,达拉斯联储银行在11月份发表了一篇题为《消除美国房地产泡沫是一项微妙而艰巨的任务》的文章。文章认为,美国的政策制定者应该努力让泡沫缩水,而不是戳破它。

达拉斯联储银行的马丁内斯·加西亚在文中指出:“在当前的环境下,当住房需求出现疲软迹象时,货币政策需要很小心地起到穿针引线的作用,既要下调通胀,同时也不能引发房价的螺旋式下跌——也就是不能引起住房市场的大抛售,那将加剧经济下行。”加西亚还表示:“虽然形式充满挑战,但是灾难性的崩盘并非不可避免,在缩小房市泡沫的同时实现美联储软着陆目标的机会窗口仍然是存在的。”

为了更好地理解下一步房地产市场下一步将何去何从,我们可以深入研究一下鲍威尔关于房地产市场的言论。

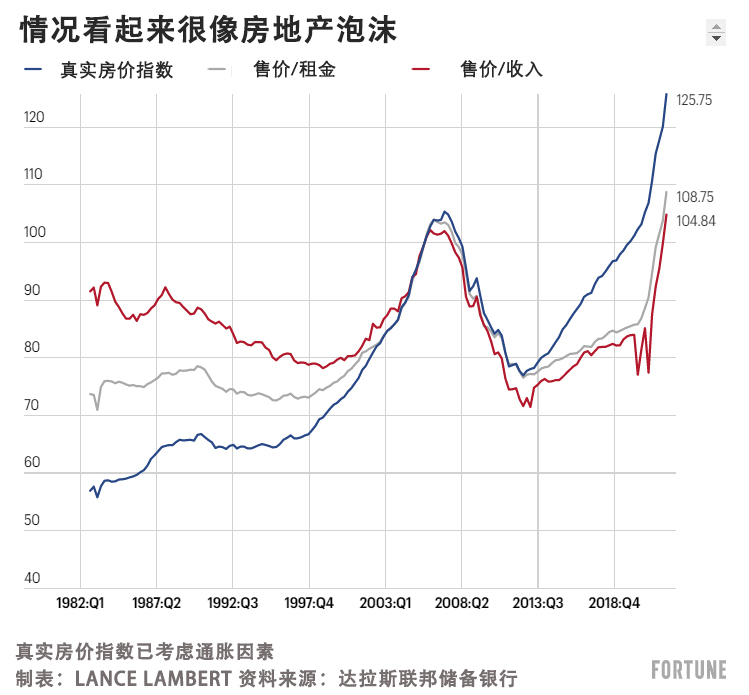

客观地说,美国房地产市场在疫情期间的确出现了泡沫。达拉斯联储银行的数据显示,2022年的美国房价实陆上比2005年和2008年更加脱离基本面。

未来一年内,房价与基本面的撕裂应该会有所愈合,这也是摩根士丹利、Zonda、毕马威、约翰伯恩斯房地产咨询、穆迪分析、高盛、富国、房利美和泽尔曼联合公司等多家业内分析机构的共同意见。这些公司认为,随着消费者的负担压力变大(在美国房价飙升40%之后,美国的抵押贷款利率也大幅上涨3%),美国的房价将在2023年进一步下跌。如果美国房价(目前已从2022年6月的最高点下跌2.2%)继续下跌,而收入继续上涨,则基本面将确实开始回归现实。

不过,美联储的官员们并不认为目前的楼市调整是2008年的重演。

“从金融稳定性的角度来看,我们在这个周期内并未看到上次金融危机前的那种大规模的不良信贷。现在的贷款机构对住房信贷的管理要谨慎得多。所以2022年的情况是完全不同的,目前看来不存在金融稳定性的问题。但是我们也确实明白,房地产是影响我们政策的一个很大的方面。”鲍威尔在11月初对记者表示。

而上一次房地产泡沫则是另一幅景象。在上次房地产泡沫期间,贪婪的借贷机构会向有不良信贷记录的借款人发放抵押贷款(更确切地说,是次级抵押贷款)。贷款的涌入促进了房地产市场的繁荣和房价上涨。但是随着美联储收紧贷币政策,美国在2006年出现了市场调整,房地产市场迅速出现供应过剩的局面,大量不良贷款无法偿还,很多房子只能法拍了事。这种供给过剩和大量法拍房并存的局面,导致美国房价在2007年至2012年期间足足下跌了26%。

虽然美联储官员承认,美国房价有可能出现“实质性调整”,但他们并不认为这轮调整的破坏性会达到2008年的规模。原因是美联储认为未来几年,我们不必担心出现大规模的法拍房危机或者大规模的供给过剩。

由于房地产市场的高销量和供应链问题叠加,导致疫情期间美国有大量住房项目未能按时交付。一方面,由于房地产商急于交房,这可能会加剧2023年的房价下行压力。另一方面,这些房子尚不足以解决美国的住房短缺问题。鲍威尔也在上周三的讲话中承认了这一点。

鲍威尔表示:“这些(批进行中的住房调整)都不会带来影响长期的问题,因为美国是一个发达国家,建设中的住房数量是难以满足公众的需求的,所以住房短缺的情况长期看来仍然存在。”

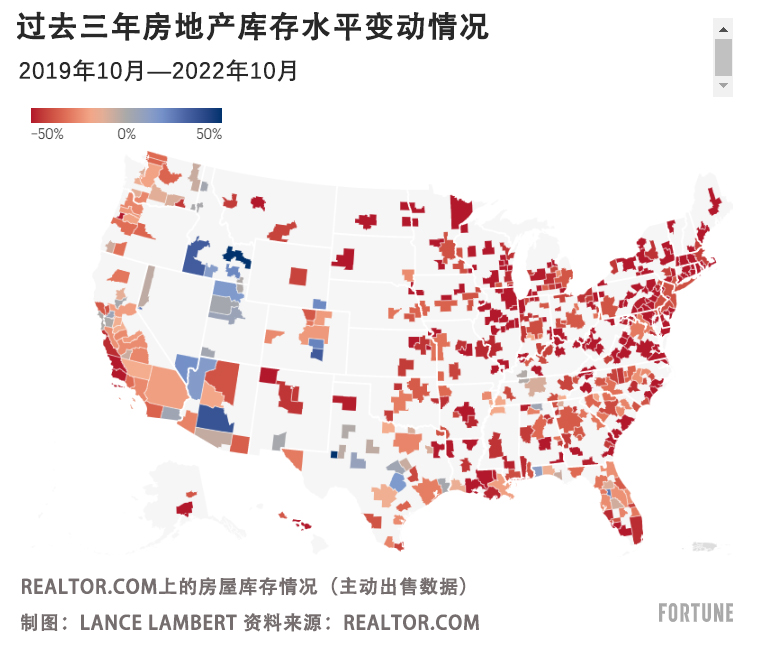

因此,尽管抵押贷款利率的大幅上涨,有可能通过压低房价的方式,给房地产市场带来“平衡”,并且给进一步增长带来一些去库的空间,但是从长期看来,市场的轨迹可能仍然不利于买方。

我们还要明确一点——没有人知道所谓的“房地产市场调整”将如何展开。需要解答的问题太多了。比如美国的通胀是否会快速下降,并且同时拉低抵押贷款利率?抑或通胀具有相当的粘性,因此还需要在更长的时间内维持较高的利率?

但有一点可以肯定,那就是根据历史经验,下一步的走向肯定是因地而异的。

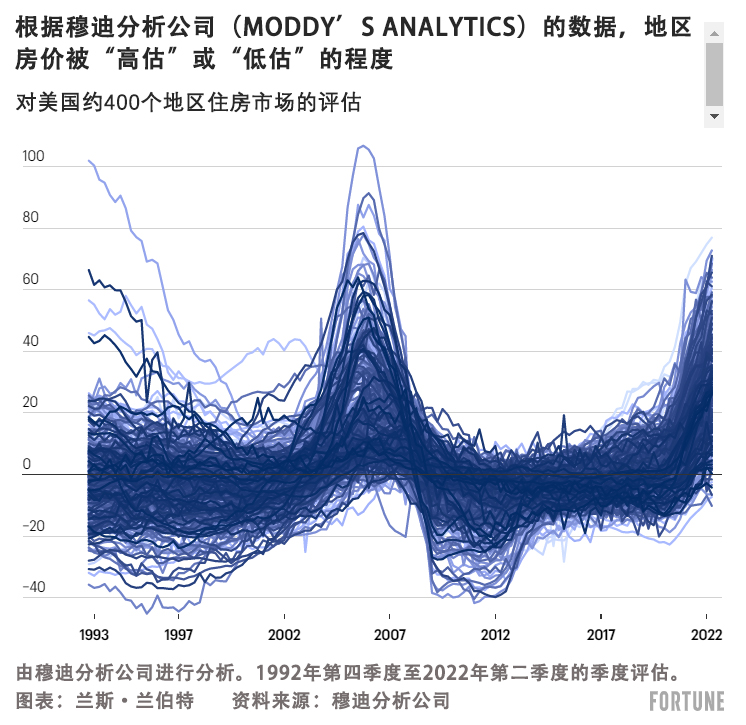

这样说的一个重要原因是,不同地区的基本面差异很大。以克利夫兰和奥斯汀为例,前者在疫情期间出现了房地产繁荣,后者的房价更是飙升了70%以上。当然现在两地的房地产市场已经发生了变化,奥斯汀已经出现了大幅回调(穆迪分析认为该地房价被“高估”了61%),而克里夫兰只是房价增速略有放缓(穆迪分析认为该地房价被高估了15%)。

简单地说就是,房地产市场的基本面仍然是很重要的。(财富中文网)

译者:朴成奎

2005年的时候,美联储主席格林斯潘曾对国会表示:“美国整体上不太可能出现房价泡沫。”但是事实上,当时房地产泡沫不但已经形成了,而且就在格林斯潘在国会传达这一信息时,泡沫已接近了顶峰。

时间快进到2022年,正是因为大家对上次泡沫心有余悸,所以这一次,经济学家们并不害怕承认泡沫的存在——即便他们觉得这次泡沫或许没有上一次那么危险。

上周二,全世界最有影响力的经济学家就是这样做的——美联储主席杰罗姆·鲍威尔在布鲁金斯学会的一次活动中表示,美国在疫情期间的房价上涨就符合“房地产泡沫”的定义。

“由于疫情的缘故,当时的抵押贷款利率非常低,人们都想买房,而且是想离开城市,在郊区买房,所以美国确实出现了房地产泡沫,房价上涨到了非常不可持续的水平,出现了过热等问题。所以,现在的房地产市场将迎来泡沫的另一阶段,希望它的供需关系能达到一个更好的状态。”鲍威尔说。

结合鲍威尔以往的发言,美国房地产的“平衡”进程应该已经开始了。今年6月份,鲍威尔曾表示,抵押贷款利率的大幅上涨将有助于“重置”美国的房地产市场。9月份鲍威尔曾对记者表示,美国已经正式进入了一个“艰难的房地产市场调整期”,它将恢复市场的“平衡”。

在鲍威尔承认有“泡沫”之前,达拉斯联储银行在11月份发表了一篇题为《消除美国房地产泡沫是一项微妙而艰巨的任务》的文章。文章认为,美国的政策制定者应该努力让泡沫缩水,而不是戳破它。

达拉斯联储银行的马丁内斯·加西亚在文中指出:“在当前的环境下,当住房需求出现疲软迹象时,货币政策需要很小心地起到穿针引线的作用,既要下调通胀,同时也不能引发房价的螺旋式下跌——也就是不能引起住房市场的大抛售,那将加剧经济下行。”加西亚还表示:“虽然形式充满挑战,但是灾难性的崩盘并非不可避免,在缩小房市泡沫的同时实现美联储软着陆目标的机会窗口仍然是存在的。”

为了更好地理解下一步房地产市场下一步将何去何从,我们可以深入研究一下鲍威尔关于房地产市场的言论。

客观地说,美国房地产市场在疫情期间的确出现了泡沫。达拉斯联储银行的数据显示,2022年的美国房价实陆上比2005年和2008年更加脱离基本面。

未来一年内,房价与基本面的撕裂应该会有所愈合,这也是摩根士丹利、Zonda、毕马威、约翰伯恩斯房地产咨询、穆迪分析、高盛、富国、房利美和泽尔曼联合公司等多家业内分析机构的共同意见。这些公司认为,随着消费者的负担压力变大(在美国房价飙升40%之后,美国的抵押贷款利率也大幅上涨3%),美国的房价将在2023年进一步下跌。如果美国房价(目前已从2022年6月的最高点下跌2.2%)继续下跌,而收入继续上涨,则基本面将确实开始回归现实。

不过,美联储的官员们并不认为目前的楼市调整是2008年的重演。

“从金融稳定性的角度来看,我们在这个周期内并未看到上次金融危机前的那种大规模的不良信贷。现在的贷款机构对住房信贷的管理要谨慎得多。所以2022年的情况是完全不同的,目前看来不存在金融稳定性的问题。但是我们也确实明白,房地产是影响我们政策的一个很大的方面。”鲍威尔在11月初对记者表示。

而上一次房地产泡沫则是另一幅景象。在上次房地产泡沫期间,贪婪的借贷机构会向有不良信贷记录的借款人发放抵押贷款(更确切地说,是次级抵押贷款)。贷款的涌入促进了房地产市场的繁荣和房价上涨。但是随着美联储收紧贷币政策,美国在2006年出现了市场调整,房地产市场迅速出现供应过剩的局面,大量不良贷款无法偿还,很多房子只能法拍了事。这种供给过剩和大量法拍房并存的局面,导致美国房价在2007年至2012年期间足足下跌了26%。

虽然美联储官员承认,美国房价有可能出现“实质性调整”,但他们并不认为这轮调整的破坏性会达到2008年的规模。原因是美联储认为未来几年,我们不必担心出现大规模的法拍房危机或者大规模的供给过剩。

由于房地产市场的高销量和供应链问题叠加,导致疫情期间美国有大量住房项目未能按时交付。一方面,由于房地产商急于交房,这可能会加剧2023年的房价下行压力。另一方面,这些房子尚不足以解决美国的住房短缺问题。鲍威尔也在上周三的讲话中承认了这一点。

鲍威尔表示:“这些(批进行中的住房调整)都不会带来影响长期的问题,因为美国是一个发达国家,建设中的住房数量是难以满足公众的需求的,所以住房短缺的情况长期看来仍然存在。”

因此,尽管抵押贷款利率的大幅上涨,有可能通过压低房价的方式,给房地产市场带来“平衡”,并且给进一步增长带来一些去库的空间,但是从长期看来,市场的轨迹可能仍然不利于买方。

我们还要明确一点——没有人知道所谓的“房地产市场调整”将如何展开。需要解答的问题太多了。比如美国的通胀是否会快速下降,并且同时拉低抵押贷款利率?抑或通胀具有相当的粘性,因此还需要在更长的时间内维持较高的利率?

但有一点可以肯定,那就是根据历史经验,下一步的走向肯定是因地而异的。

这样说的一个重要原因是,不同地区的基本面差异很大。以克利夫兰和奥斯汀为例,前者在疫情期间出现了房地产繁荣,后者的房价更是飙升了70%以上。当然现在两地的房地产市场已经发生了变化,奥斯汀已经出现了大幅回调(穆迪分析认为该地房价被“高估”了61%),而克里夫兰只是房价增速略有放缓(穆迪分析认为该地房价被高估了15%)。

简单地说就是,房地产市场的基本面仍然是很重要的。(财富中文网)

译者:朴成奎

In 2005, Fed Chair Alan Greenspan told Congress that a “bubble in home prices for the nation as a whole does not appear likely.” Of course, not only had a housing bubble formed, it was nearing its peak just as Greenspan delivered that message on Capitol Hill.

Fast forward to 2022, and the scars of the last bubble have clearly made economists less afraid to acknowledge a housing bubble—even if they believe the bubble could be less dangerous than the one that formed in the early 2000s.

On Tuesday, the most powerful economist in the world did just that: Speaking at a Brookings Institute event, Fed Chair Jerome Powell told the audience that the run-up in home prices during the Pandemic Housing Boom qualifies a “housing bubble.”

“Coming out of the pandemic, [mortgage] rates were very low, people wanted to buy houses, they wanted to get out of the cities and buy houses in the suburbs because of COVID. So you really had a housing bubble, you had housing prices going up [at] very unsustainable levels and overheating and that kind of thing. So, now the housing market will go through the other side of that and hopefully come out in a better place between supply and demand,” Powell said.

According to past statements by Powell, that process of bringing “balance” to the U.S. housing market has already begun. In June, Powell said spiked mortgage rates would help to “reset” the U.S. housing market. Then in September, Powell told reporters that we had officially entered into a “difficult [housing] correction” that would restore “balance” to the market.

That “bubble” acknowledgment by Powell comes on the heels of an article published in November by the Federal Reserve Bank of Dallas with the title “Skimming U.S. Housing Froth a Delicate, Daunting Task.” The article argued that policymakers should try to deflate the bubble rather than burst it.

“In the current environment, when housing demand is showing signs of softening, monetary policy needs to carefully thread the needle of bringing inflation down without setting off a downward house-price spiral—a significant housing sell-off—that could aggravate an economic downturn,” writes Martínez-García at the Dallas Fed. “A severe housing bust from the frothy pandemic run-up isn’t inevitable. Although the situation is challenging, there remains a window of opportunity to deflate the housing bubble while achieving the Fed’s preferred outcome of a soft landing.”

To better understand where we might head next, let’s take a deeper examination of Powell’s housing comments.

The U.S. housing market got objectively bubbly during the pandemic. In fact, data produced by the Dallas Fed (see chart above) finds that home prices in 2022 are actually more detached from underlying fundamentals than they were 2005 and 2008.

Over the coming year, those detached fundamentals should begin to heal a bit. That's a view held by firms like Morgan Stanley, Zonda, KPMG, John Burns Real Estate Consulting, Moody's Analytics, Goldman Sachs, Wells Fargo, Fannie Mae, and Zelman & Associates. Those firms believe that "pressurized" affordability (i.e. mortgage rates spiking 3 percentage points just after U.S. home prices soared 40%) will see home prices fall further in 2023. If U.S. home prices—which are already down 2.2% from their June 2022 peak—continue to fall and incomes continue to rise, fundamentals would indeed begin to come back down to earth.

That said, Fed officials don't think the ongoing housing correction is a 2008 repeat.

"From a financial stability standpoint, we didn't see in this cycle the kinds of poor underwriting credit that we saw before the Great Financial Crisis. Housing credit was much more carefully managed by the lenders. It's a very different situation [in 2022], it doesn't present potential, [well] it doesn't appear to present financial stability issues. But we do understand that [housing] is where a very big effect of our policies is," Powell told reporters earlier in November.

See, the last housing bubble was fundamentally a different story. Back in the aughts, zealous lenders were giving out mortgages (or better put, subprime mortgages) to folks who historically wouldn’t have qualified. As that credit rushed in, it helped to drive both a building boom and a home price boom. However, once Fed tightening set off a housing market correction in 2006, that building boom turned into a supply glut and those bad loans turned into a foreclosure crisis. That combination of oversupply and "forced selling" saw U.S. home prices fall a staggering 26% between 2007 and 2012.

While Fed officials acknowledge that we could see a "material correction" in home prices, they don't believe it'd be as damaging as the 2008 crash. The reason? In the years ahead, the Fed believes we shouldn't have to worry about a foreclosure crisis nor a massive supply glut.

A combination of high sales and supply chain issues saw home builders build-up quite a backlog of unfinished projects during the pandemic. On one hand, as homebuilders rush to offload these homes that could put downward pressure on home prices in 2023. On the other hand, this simply isn't enough homes to solve the nation's housing shortage. Powell acknowledged as much on Wednesday.

"None of this [the ongoing housing correction] affects the longer run issue, which is that we got a built-up country and it's hard to get zoning and hard to get housing built in sufficient quantities to meet the public's demand," Powell. "There's a longer run housing shortage."

So while spiked mortgage rates may help to bring "balance" to the housing market by pushing home prices lower and giving inventory (see chart above) breathing room to grow, the trajectory of the market might not favor buyers for long.

Let's be clear: No one really knows how the ongoing housing correction will actually unfold. There are simply too many question marks. Does inflation come down quickly and bring mortgage rates down with it? Or does inflation prove sticky, and thus require higher rates for longer?

But we can say, based on past history, whatever comes next will surely vary by housing market.

One big reason that it'll vary is that fundamentals vary so much by market. Look no further than Cleveland and Austin. The former saw a modest housing boom during the pandemic, while the latter saw home prices soar over 70%. Of course, now that the housing market has shifted, Austin (which Moody's Analytics estimates is "overvalued" by 61%) has already slipped into a sharp correction while Cleveland (which is "overvalued" by 15%) has simply slowed down.

Simply put: Housing fundamentals still matter.