美国各地楼市两极分化,涨多跌少

Lance Lambert

2023-04-26

大多数房价出现下跌的市场位于美国的西部地区。

文本设置

文本设置

Plus(0条)

Plus(0条)

2022年的抵押贷款利率冲击来得如此突然,以至于Zillow的研究人员别无选择,只能再三地大幅下调未来12个月的房价预期。2022年3月,Zillow曾经预计未来12个月房价将上涨17.8%。然而,到2022年12月,这一数字被大幅下调至预期下跌1.1%。

快进到2023年4月,不仅抵押贷款利率在今年春天稳定在6.5%左右,而且房市修正也失去了动力。这就解释了为什么Zillow不再下调预测,而是开始上调预期。

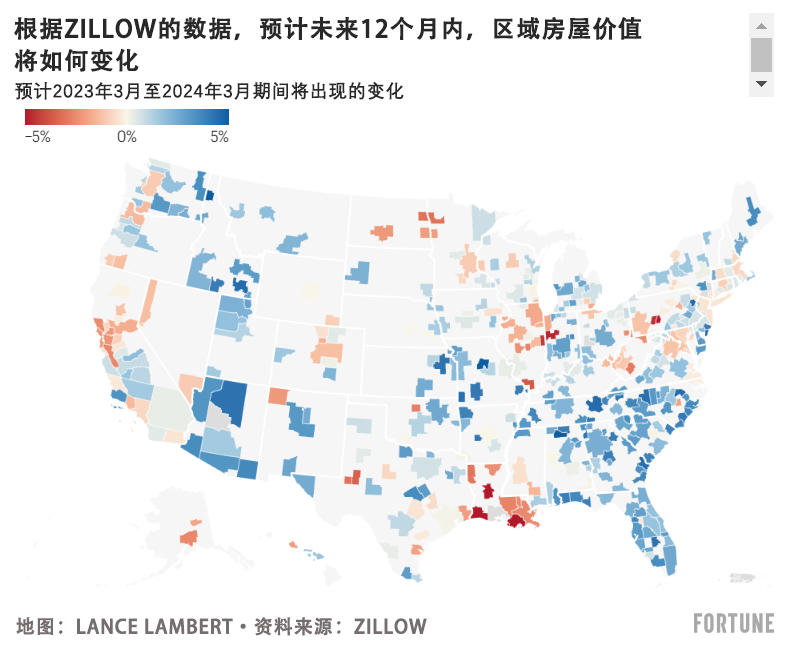

展望未来,Zillow的经济学家预计,在2023年3月至2024年3月期间,Zillow房屋价值指数(Zillow Home Value Index)追踪的美国房屋价值将上涨1.7%。

然而,这是全国性预期。如果说房地产市场修正出现的两极分化——西部地区房市震荡剧烈,而东部地区房市震荡温和——进一步强化了任何态势的话,那就是房地产的地方性得到进一步强化。

在Zillow跟踪的400个最大的房地产市场中,该公司预计,在2023年3月至2024年3月期间,294个市场的房价将上涨,预计4个市场将保持平稳,102个市场的房价将在未来12个月内下跌。

就在一个月前,Zillow预计在2023年2月至2024年2月期间,238个市场的房价将上涨,而156个市场将在同一时间段内下跌。

让我们进一步了解一下Zillow的最新预测。

Zillow预计,在2023年3月至2024年3月期间,田纳西州诺克斯维尔(预计房价上涨4.5%)、佐治亚州萨凡纳(预计房价上涨4.5%)、北卡罗来纳州温斯顿-塞勒姆(预计房价上涨4.4%)、田纳西州约翰逊市(预计房价上涨4.2%),以及北卡罗来纳州威明顿市(预计房价上涨4.1%)等市场的房价涨幅最大。简而言之:Zillow的预测模型预计美国东南部地区的房价将出现强劲上涨。

Zillow的高级经济学家杰夫·塔克在最近的一份报告里写道:“许多市场的价格可能已经触底,价格下跌可能有助于吸引更多买家在今年春天买房。库存水平非常低可能是[一些市场]房价再次开始回升的一大主要原因。”

然而,Zillow的经济学家预计,在2023年3月至2024年3月期间,旧金山(预计房价下跌2.6%)、科罗拉多州博尔德(预计房价下跌1.6%)、丹佛(预计房价下跌1.3%)、内华达州里诺(预计房价下跌1.3%)和拉斯维加斯(预计房价下跌1%)等市场的房价将出现下跌。

相对于穆迪分析(Moody's Analytics)和房利美(Fannie Mae)的经济学家,Zillow的团队持乐观态度。穆迪分析预计2023年全美房价将下跌4.2%,房利美预计2023年全美房价将下跌1.2%。

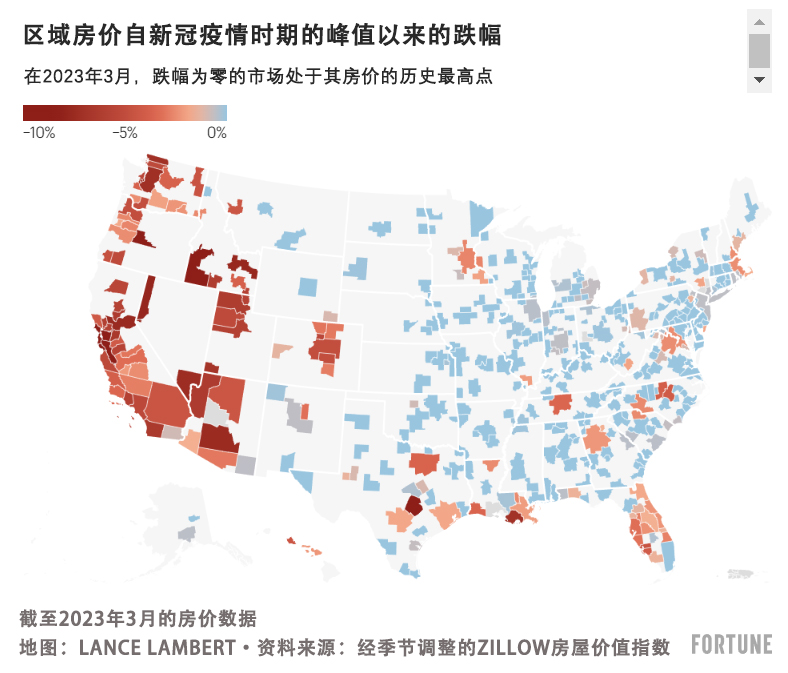

在Zillow跟踪的400个最大的区域房地产市场中,182个市场的房价仍然低于2022年的峰值,而截至2023年3月,218个市场已经回到(或者高于)2022年的峰值。

大多数房价出现下跌的市场位于美国的西部地区。

原因很简单:西部地区的房地产市场对利率非常敏感。

正如《财富》杂志此前报道的那样,对利率敏感的科技公司高度集中在西部地区,而且西部地区房价过热,容易受到抵押贷款利率飙升的影响。如果西部地区的买家在抵押贷款利率很低的时候就已经开始透支了,那么当抵押贷款利率飙升时,他们最终会推迟进入房地产市场,这才是合理的。这暗示着房价会下跌。(财富中文网)

译者:中慧言-王芳

2022年的抵押贷款利率冲击来得如此突然,以至于Zillow的研究人员别无选择,只能再三地大幅下调未来12个月的房价预期。2022年3月,Zillow曾经预计未来12个月房价将上涨17.8%。然而,到2022年12月,这一数字被大幅下调至预期下跌1.1%。

快进到2023年4月,不仅抵押贷款利率在今年春天稳定在6.5%左右,而且房市修正也失去了动力。这就解释了为什么Zillow不再下调预测,而是开始上调预期。

展望未来,Zillow的经济学家预计,在2023年3月至2024年3月期间,Zillow房屋价值指数(Zillow Home Value Index)追踪的美国房屋价值将上涨1.7%。

然而,这是全国性预期。如果说房地产市场修正出现的两极分化——西部地区房市震荡剧烈,而东部地区房市震荡温和——进一步强化了任何态势的话,那就是房地产的地方性得到进一步强化。

在Zillow跟踪的400个最大的房地产市场中,该公司预计,在2023年3月至2024年3月期间,294个市场的房价将上涨,预计4个市场将保持平稳,102个市场的房价将在未来12个月内下跌。

就在一个月前,Zillow预计在2023年2月至2024年2月期间,238个市场的房价将上涨,而156个市场将在同一时间段内下跌。

让我们进一步了解一下Zillow的最新预测。

Zillow预计,在2023年3月至2024年3月期间,田纳西州诺克斯维尔(预计房价上涨4.5%)、佐治亚州萨凡纳(预计房价上涨4.5%)、北卡罗来纳州温斯顿-塞勒姆(预计房价上涨4.4%)、田纳西州约翰逊市(预计房价上涨4.2%),以及北卡罗来纳州威明顿市(预计房价上涨4.1%)等市场的房价涨幅最大。简而言之:Zillow的预测模型预计美国东南部地区的房价将出现强劲上涨。

Zillow的高级经济学家杰夫·塔克在最近的一份报告里写道:“许多市场的价格可能已经触底,价格下跌可能有助于吸引更多买家在今年春天买房。库存水平非常低可能是[一些市场]房价再次开始回升的一大主要原因。”

然而,Zillow的经济学家预计,在2023年3月至2024年3月期间,旧金山(预计房价下跌2.6%)、科罗拉多州博尔德(预计房价下跌1.6%)、丹佛(预计房价下跌1.3%)、内华达州里诺(预计房价下跌1.3%)和拉斯维加斯(预计房价下跌1%)等市场的房价将出现下跌。

相对于穆迪分析(Moody's Analytics)和房利美(Fannie Mae)的经济学家,Zillow的团队持乐观态度。穆迪分析预计2023年全美房价将下跌4.2%,房利美预计2023年全美房价将下跌1.2%。

在Zillow跟踪的400个最大的区域房地产市场中,182个市场的房价仍然低于2022年的峰值,而截至2023年3月,218个市场已经回到(或者高于)2022年的峰值。

大多数房价出现下跌的市场位于美国的西部地区。

原因很简单:西部地区的房地产市场对利率非常敏感。

正如《财富》杂志此前报道的那样,对利率敏感的科技公司高度集中在西部地区,而且西部地区房价过热,容易受到抵押贷款利率飙升的影响。如果西部地区的买家在抵押贷款利率很低的时候就已经开始透支了,那么当抵押贷款利率飙升时,他们最终会推迟进入房地产市场,这才是合理的。这暗示着房价会下跌。(财富中文网)

译者:中慧言-王芳

Last year’s mortgage rate shock was so abrupt that researchers at Zillow had no choice but to repeatedly issue sharp downward revisions for their 12-month home price outlook. In March 2022, Zillow had been expecting home prices to rise 17.8% over the next 12 months. By December 2022, however, that was slashed all the way down to a forecasted decline of 1.1%.

Fast-forward to April 2023, and not only have mortgage rates stabilized around 6.5% this spring but the housing correction has also lost steam. That explains why Zillow stopped issuing downward forecast revisions, and is actually starting to raise its outlook.

Heading forward, Zillow economists expect U.S. home values as tracked by the Zillow Home Value Index (ZHVI) to rise 1.7% between March 2023 and March 2024.

However, that’s its national outlook. If the bifurcated housing market correction—which has been sharp out West and mild in the East—has reinforced anything it’s that real estate is indeed local.

Among the 400 largest housing markets tracked by Zillow, the company expects 294 markets to see positive home price growth between March 2023 and March 2024, while it expects four markets to remain flat and home prices to fall over the next 12 months in 102 markets.

Just one month ago, Zillow expected 238 markets to rise between February 2023 and February 2024, while it expected 156 markets to decline during that same span.

Let’s take a closer look at Zillow’s latest forecast.

Between March 2023 and March 2024, Zillow expects some of the biggest home price upticks to occur in markets like Knoxville, Tenn. (+4.5% forecasted home price growth), Savannah, Ga. (+4.5%), Winston-Salem, N.C. (+4.4%), Johnson City, Tenn. (+4.2%), and Wilmington, N.C. (+4.1%). Simply put: Zillow's forecast model expects a great deal of strength in the U.S. Southeast.

"Many markets may have already seen prices bottom out, and those price declines may be helping entice more buyers this spring," wrote Jeff Tucker, senior economist at Zillow, in a recent report. "The very low [levels of] inventory is likely a major reason that home prices [in some markets] have begun to rise again."

However, Zillow economists do expect home price declines to occur between March 2023 and March 2024 in markets like San Francisco (-2.6% forecasted decline), Boulder, Colo. (-1.6%), Denver (-1.3%), Reno, Nev. (-1.3%), and Las Vegas (-1%).

Relative to economists at Moody's Analytics (which expects national home prices to fall 4.2% in 2023) and Fannie Mae (which expects national home prices to fall 1.2% in 2023), Zillow's team is on the optimistic side.

Among the 400 largest regional housing markets tracked by Zillow, 182 remain below their 2022 peak price, while 218 markets, as of March 2023, are back to (or above) their 2022 peak price.

Among the down markets, the majority are located in the Western half of the country.

The reason is pretty straightforward: Western housing markets are hyper rate-sensitive.

As Fortune has previously reported, Not only does the West have a high concentration of rate-sensitive tech employers, but it also has overheated home prices that are vulnerable to mortgage rate spikes. If Western buyers were already stretching themselves then (see here) while mortgage rates were low, it only makes sense that they'd finally push back once mortgage rates spiked. Cue falling home prices.

请打开财富Plus APP