硅谷银行倒闭后,美国房地产市场面临两大变化

Lance Lambert

2023-03-17

硅谷银行的倒闭可能意味着旧金山、博伊西和西雅图等以科技行业主导的房地产市场将受到更大的冲击。

文本设置

文本设置

Plus(0条)

Plus(0条)

最近硅谷银行(Silicon Valley Bank)的倒闭对房地产行业产生了严重冲击,建筑商和房产中介都想弄清楚此次危机对抵押贷款利率和整体经济的影响。

3月14日,Zillow公司的首席经济学家斯凯拉·奥尔森发表了一篇文章,从两方面预测了硅谷银行倒闭对2023年美国房地产市场的影响。

以下是他预测的两种可能。

1. 硅谷银行倒闭可能导致抵押贷款利率下降

他预测的第一种情况是,如果美联储(Federal Reserve)未来停止他所写的“几周前刚刚发生的”加息,抵押贷款利率就可能下降。

金融市场已经使平均30年期固定抵押贷款利率从上周最高的7.05%下降到6.75%。如果美联储在3月不再加息,有分析师认为抵押贷款利率就可能进一步下降。

奥尔森写道:“最近几个月,购房人对抵押贷款利率的变化反应非常激烈;本月早些时候,抵押贷款利率重新上涨超过7%,逆转了今年年初利率下降时所形成的势头。现在,抵押贷款利率下降可能令相当冷淡的春季购房季迎来春暖花开。对现在的购房者而言,尤其是在房价较高的地区,利率持续下降将有利于大幅提升可负担性,但他们依旧需要为利率波动做好计划。”

尽管如此,奥尔森指出,如果说硅谷银行的倒闭预示着2023年迫在眉睫的经济衰退,那么抵押贷款利率下降提高的可负担性,可能因为经济镇痛无法发挥效果。

奥尔森说:“在可负担性方面,更低的利率有利于捉襟见肘的购房人,但如果说硅谷银行的倒闭预示着更广泛的问题,即将发生的经济衰退的严重程度和持续时间就可能超出预期。在经济压力集中的房地产市场,收入损失或失业将有更大概率开始对房地产市场造成影响。”

2. 硅谷银行破产后,科技中心将受到更大冲击

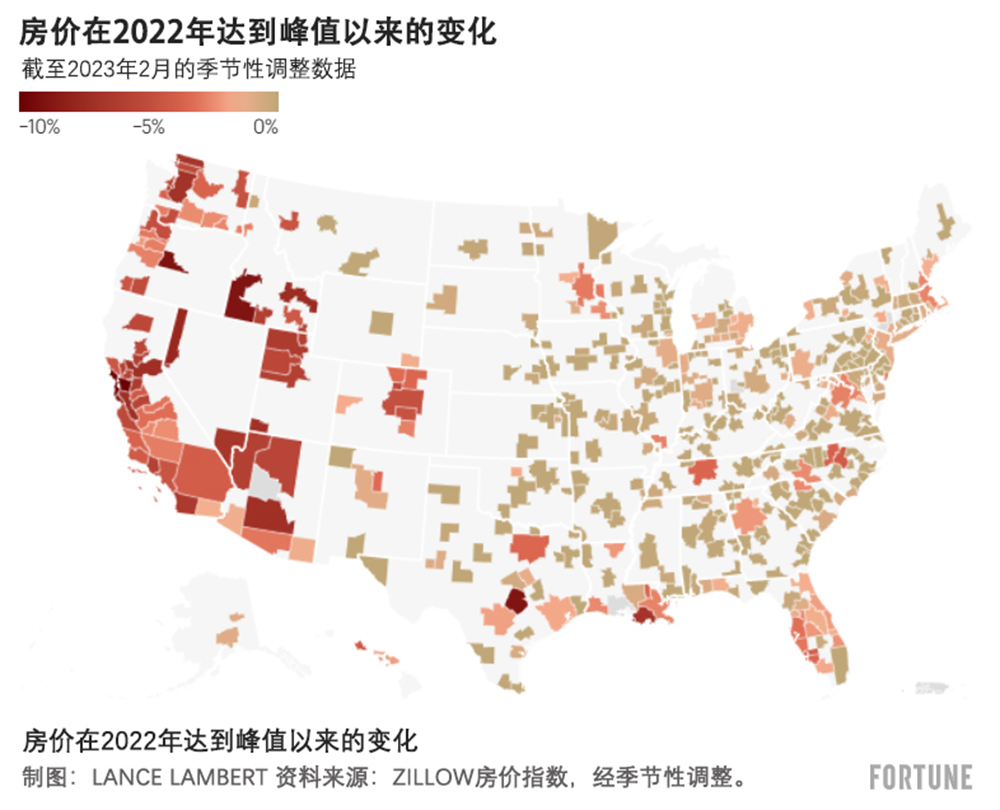

奥尔森预测,硅谷银行的倒闭可能意味着,旧金山、博伊西和西雅图等以科技行业主导的房地产市场将受到更大的冲击。位于美国西部的这些高房价市场,已经因为美联储应对通胀的持续努力而受到严重影响,硅谷银行的倒闭可能会雪上加霜。

正如奥尔森写道:“旧金山湾区和西雅图等房地产市场或许对科技行业的整体低迷有切身感受。科技行业的就业与股价都对这些市场有巨大的影响。多年来,在高收入和股价上涨的支撑下,这些市场房价高企。但随着可以承受高房价的购房人减少,这些市场可能陷入萧条,房价下跌。”

对西部科技中心市场甚至全美的购房人和卖房人来说,未来几个月将充满挑战。

虽然更低抵押贷款利率在短期内能够提高可负担性,受人们欢迎,但与整体经济问题有关的长期风险不容忽视。奥尔森建议:“现在购房人应该在一个地方定居下来,买一套至少希望在未来几年可以保有的住房,以免房屋积累净值需要太长时间。”

最后,硅谷银行的倒闭也提醒我们,面对广泛的经济变化和挑战,房地产市场并不能够免于影响。在当前快速变化的市场环境下,购房人和卖房人必须仔细规划,并且具备长远眼光。(财富中文网)

译者:刘进龙

审校:汪皓

最近硅谷银行(Silicon Valley Bank)的倒闭对房地产行业产生了严重冲击,建筑商和房产中介都想弄清楚此次危机对抵押贷款利率和整体经济的影响。

3月14日,Zillow公司的首席经济学家斯凯拉·奥尔森发表了一篇文章,从两方面预测了硅谷银行倒闭对2023年美国房地产市场的影响。

以下是他预测的两种可能。

1. 硅谷银行倒闭可能导致抵押贷款利率下降

他预测的第一种情况是,如果美联储(Federal Reserve)未来停止他所写的“几周前刚刚发生的”加息,抵押贷款利率就可能下降。

金融市场已经使平均30年期固定抵押贷款利率从上周最高的7.05%下降到6.75%。如果美联储在3月不再加息,有分析师认为抵押贷款利率就可能进一步下降。

奥尔森写道:“最近几个月,购房人对抵押贷款利率的变化反应非常激烈;本月早些时候,抵押贷款利率重新上涨超过7%,逆转了今年年初利率下降时所形成的势头。现在,抵押贷款利率下降可能令相当冷淡的春季购房季迎来春暖花开。对现在的购房者而言,尤其是在房价较高的地区,利率持续下降将有利于大幅提升可负担性,但他们依旧需要为利率波动做好计划。”

尽管如此,奥尔森指出,如果说硅谷银行的倒闭预示着2023年迫在眉睫的经济衰退,那么抵押贷款利率下降提高的可负担性,可能因为经济镇痛无法发挥效果。

奥尔森说:“在可负担性方面,更低的利率有利于捉襟见肘的购房人,但如果说硅谷银行的倒闭预示着更广泛的问题,即将发生的经济衰退的严重程度和持续时间就可能超出预期。在经济压力集中的房地产市场,收入损失或失业将有更大概率开始对房地产市场造成影响。”

2. 硅谷银行破产后,科技中心将受到更大冲击

奥尔森预测,硅谷银行的倒闭可能意味着,旧金山、博伊西和西雅图等以科技行业主导的房地产市场将受到更大的冲击。位于美国西部的这些高房价市场,已经因为美联储应对通胀的持续努力而受到严重影响,硅谷银行的倒闭可能会雪上加霜。

正如奥尔森写道:“旧金山湾区和西雅图等房地产市场或许对科技行业的整体低迷有切身感受。科技行业的就业与股价都对这些市场有巨大的影响。多年来,在高收入和股价上涨的支撑下,这些市场房价高企。但随着可以承受高房价的购房人减少,这些市场可能陷入萧条,房价下跌。”

对西部科技中心市场甚至全美的购房人和卖房人来说,未来几个月将充满挑战。

虽然更低抵押贷款利率在短期内能够提高可负担性,受人们欢迎,但与整体经济问题有关的长期风险不容忽视。奥尔森建议:“现在购房人应该在一个地方定居下来,买一套至少希望在未来几年可以保有的住房,以免房屋积累净值需要太长时间。”

最后,硅谷银行的倒闭也提醒我们,面对广泛的经济变化和挑战,房地产市场并不能够免于影响。在当前快速变化的市场环境下,购房人和卖房人必须仔细规划,并且具备长远眼光。(财富中文网)

译者:刘进龙

审校:汪皓

The recent collapse of Silicon Valley Bank has sent shock waves through the real estate industry as builders and agents alike scramble to understand what it means for mortgage rates and the economy at large.

In an article published on March 14, Zillow chief economist Skylar Olsen gave two predictions for how the shutdown of Silicon Valley Bank could impact the U.S. housing market in 2023.

Let’s take a look.

1. It could push mortgage rates down

The first prediction is that mortgage rates could fall if the Federal Reserve backs off from future rate hikes, which Olsen writes “appeared imminent just weeks ago.”

Already, financial markets have pushed the average 30-year fixed mortgage rate to 6.75%—down from last week’s peak of 7.05%. If the Fed doesn’t issue a rate hike in March, some analysts think mortgage rates would sink even further.

“Home buyers have been very responsive to mortgage rates in recent months; when rates climbed back above 7% earlier this month, it stifled momentum that had been building as rates originally drifted down to start the year. Today, falling mortgage rates could thaw what was shaping up to be a fairly frozen spring home shopping season,” wrote Olsen. “For buyers shopping now—especially in high-priced areas—a sustained rate drop will be a welcome boost to affordability, but they should still plan on rate volatility.”

That said, if Silicon Valley Bank’s collapse forewarns of a looming 2023 recession, Olsen writes, the affordability gains from lower mortgage rates could be muted by economic pain.

“Lower rates would help home buyers who are stretched thin when it comes to affordability, but if SVB’s troubles are indicative of wider issues, a coming recession could be deeper and longer-lasting than expected. That raises the odds that income or job loss could start affecting housing markets where the economic stress is concentrated,” wrote Olsen.

2. Tech hubs should brace for more pain in the wake of Silicon Valley Bank’s collapse

The downfall of Silicon Valley Bank, Olsen predicts, might mean more pain awaits tech-dominated housing markets like San Francisco, Boise, and Seattle. These Western high-cost markets have already been heavily affected by the Fed’s ongoing inflation fight, and the collapse of Silicon Valley Bank could exacerbate existing challenges.

As Olsen notes, “A widespread tech downturn might be felt in housing markets like the San Francisco Bay Area and Seattle, where tech employment and stock prices have an outsized effect. With fewer home buyers in these markets able to afford the elevated prices that have been supported over the years by high incomes and stock growth, it’s likely these markets would chill and prices would come down.”

For buyers and sellers in these Western tech-hub markets, as well as across the U.S. more broadly, the coming months are likely to be challenging.

While lower mortgage rates could provide a welcome boost to affordability in the short term, longer-term risks associated with wider economic issues cannot be ignored. As Olsen advises, "Buyers today should be looking to put down roots and find a home they’ll want to keep for at least the next several years in case it takes awhile to build equity."

Ultimately, the fallout from SVB's collapse serves as a reminder that the housing market is not immune to wider economic shifts and challenges. As buyers and sellers navigate this rapidly evolving landscape, careful planning and a long-term perspective will be essential.

请打开财富Plus APP