被裁之后个人资金管理的五大注意事项

Kaitlyn Koterbski

2023-01-12

如果你收到公司通知,成为了大规模裁员的对象之一,那么你就有必要立即制定计划,为下岗之后即将出现的重大经济状况变化做好准备。

文本设置

文本设置

Plus(0条)

Plus(0条)

如果你收到公司通知,成为了大规模裁员的对象之一,那么你就有必要立即制定计划,为下岗之后即将出现的重大经济状况变化做好准备。

被裁之后在资金管理方面应注意的五件事情

根据《职工调整与再培训通知法》(Worker Adjustment and Retraining Notification Act),某些公司,比如员工规模超过100名的公司,如果其员工的工作会因为大规模裁员或工厂关闭而受到影响,则至少应该提前60天告知员工。提前告知的初衷便是让员工能够有时间做好失业期间个人财务方面的准备。

失业后,管理自身资金的一些最佳方式包括:联系公司人力资源部门,索要可行的遣散费方案;申请失业救助,以补充自己的应急储蓄金;以及制定保险和401(K)计划应对策略。人们还有必要评估当前的开支习惯,并在颗粒无收之时削减不必要的开支。

联系人力资源部门

当你成为裁员对象之后,你的雇主会通知你是否有资格获得遣散补偿方案,该方案会列出解聘的资金补偿条款,包括按照员工被裁之前在该公司工作年限计算的遣散费和福利,还可能包括未使用的带薪假期或员工寻找新工作的补贴。

大多数雇员并没有意识到,遣散补偿方案与聘用方案一样,都是可以协商的。例如,如果你认为自己的应得补偿高于公司提供的补偿,你也能够要求公司提高补偿。你的雇主可以同意你的要求,也能够让公司按照最初的方案金额发放。

在接受之前,人们有必要认真地审核其遣散补偿方案,并了解其条款。接受遣散补偿协议可能意味着放弃以不当解聘为由起诉公司,或申请失业保险。通常,人们在接受协议之前有21天的考虑期。

值得一提的是,没有联邦或州法律要求雇主给雇员提供遣散补偿,除非员工加入了工会,或员工的聘用合同中列明了这一点。

申请失业保险

在失业之后,失业保险可以在你寻找新工作时帮助补充你的应急储蓄。你所在的州可能需要数周的时间来批准你的申请,因此,人们有必要在得知即将失业之时尽快申请该保险。

失业保险的资质要求和申请批准时限会根据申请人所在州的不同而发生变化,但各州往往对员工在某个公司的工作年限或收入金额有最低要求。你所在的州可能会使用这一信息来计算你的应得福利。

大多数州会提供高达26周的失业金,并要求希望继续获取失业金的人每周进行申报。一些州还可能会提出额外的资质要求,包括在领取补助时积极寻找新工作。因此,在申请之前请了解所在州的申领资质要求。

更新保险计划

如果你的保险计划是由雇主代缴的,那么你的保险福利通常在被裁后就会终止。

作为应对举措,联邦政府出台了《统一综合预算协调法案》(Consolidated Omnibus Budget Reconciliation Act),在员工被裁之后限时延长员工获取前雇主医疗保险的时限,通常最多延长36个月。然而,按照《统一综合预算协调法案》,下岗员工需要支付一笔保险费用,并另行支付2%的管理费,才有资格获取保险,其价格通常高于普通的保险计划。

如果不愿意为了延长当前的保险而支付高额费用,那么人们可能就有资格使用《平价医疗法案》(Affordable Care Act)提供的保险,该法案征收的保费更低,通常以收入水平为基础计算。如果失业员工不满26岁,还可以使用配偶或父母的保险。

评估401(k)计划

在失业之后评估如何处理401(K)计划时,有多个做法能够考虑,包括将资金留在当前计划,将你的计划转存至新雇主或个人退休账户,或全部取现。不同的选择可能会产生额外的税赋。

维持当前的计划:如果你的401(K)计划账户中的金额达到了5,000美元或以上,你就可以将资金留在当前的计划。即便你获准保留该计划,但你在72岁之前将无法再缴纳或提取资金。等到了72岁,无论你是在工作还是退休,你都得从计划中领取最低的分配额。

这意味着,如果你希望继续在退休前往里面存钱,你就必须开设新的401(K)计划或个人退休账户。此外,如果在下岗后出现经济紧张的状况,你将无法使用你的退休储蓄金。

将计划转存至新雇主:如果你在下岗后找到了新工作,那么你就能够以相对简单的方式,通过联系此前计划的管理方,并完成要求的手续,将前雇主的计划转存至新雇主的计划,Mountain Wealth Planning的注册金融策划师艾米·滨崎说道。

需要注意的是,你的新401(K)计划可能拥有不同的规则、投资选项和费用。在决定转存资金之前请认真评估新雇主的计划,以确保它可以符合你的投资需求。

将你的计划转存至个人退休账户:如果你并不希望使用新雇主的401(K)计划,或新雇主并不提供类似计划,那么你就能够通过联系你的前计划管理机构,并要求它们将资金支付给个人退休账户管理机构,从而将退休储蓄金转移至个人退休账户。

你可以选择罗斯个人退休账户(Roth IRA)和传统个人退休账户,但此举可能会带来额外的税赋。例如,如果你的退休储蓄金在传统的401(K)计划中属于延迟纳税,那么转存至罗斯个人退休账户将被视作应税行为。

直接取现:如果你没有应急储蓄金,而且马上需要使用现金,你也能够把钱从你的401(K)计划中取出来。然而,这应该作为你在评估其他方法之后的最后一个手段,因为你必须支付普通收入所得税,而且如果你的岁数没有达到59.5岁,还得额外支付10%的提前取现罚金。

你还会损失资金原本在投资退休账户过程中累积的所有复利,而且从长期来看会对你的整个退休储蓄金带来负面影响。滨崎称:“在将401(K)计划变现之后,要达到此前水平所需的时间要长得多。”

削减开支

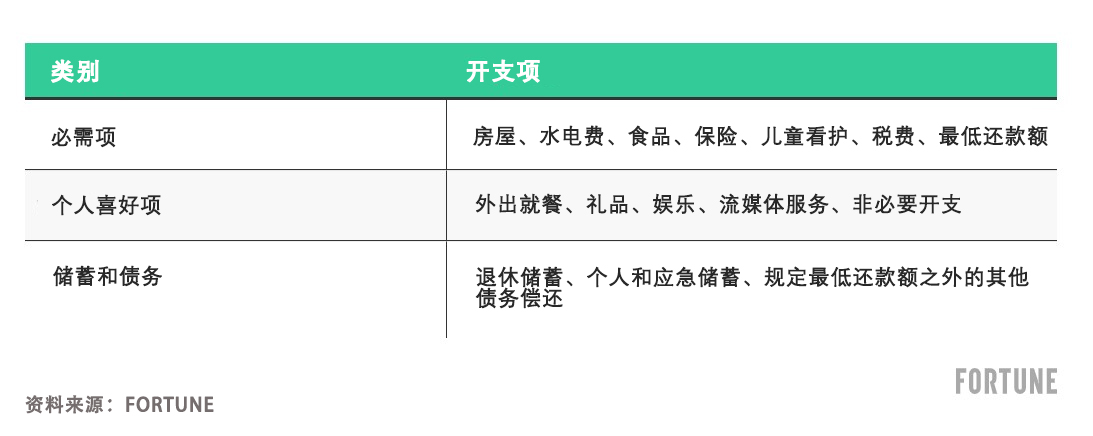

制定简单的预算并贯彻执行。如果你在被裁后依靠应急储蓄或可变收益来维持生活,你就应该评估自己的开支,并将其分为三个大类,以帮助削减不必要的开支。

必需项:很大一部分预算应该被用于支付账单,包括你的抵押贷款或租金支付、水电费、食物、燃油、最低还款额以及保险。这其中还包括学生贷款还款,但目前已经暂停,可以延期至2023年6月30日。

换句话说,你的必需项包括每个月的固定支出。这些支出应该成为你的首要考虑事项,尤其是在资金有限的情况下。

个人喜好项:预算的一小部分能够用于购买你想要购买的物品,比如在假日期间回家探望家人,或者购买新服装参加工作面试。然而,如果你近期成为了被裁对象,则应该减少自己以往在自由支配开支方面的花费。

滨崎表示:“我们首先必须考虑支付固定支出,因为在失业后,人们真的得勒紧裤腰带过日子。”这可能意味着在家做饭而不是去豪华餐厅,或者重新调整自己的假日购物计划。

储蓄和偿还债务:如果手头没有潜在的新工作,人们可能就得一边找新工作,一边延长应急储蓄的使用时间。如果出现这种情况,则应该把手头所有剩余资金放回储蓄中,以供今后使用。此外,如果你有信用卡或消费贷债务,不妨在最低还款额的基础上偿还更多的资金,以降低利息费用。

如果预算允许,不妨考虑采用50/30/20准则,也就是将50%的税后收入用于必需项开支,将30%用于个人喜好项,20%用于储蓄或减债。

例如,如果你的应急储蓄可以应付6个月的开支,每个月共计花费4,000美元。则应把2,000美元用于固定支出,1,200美元用于个人喜好项,800美元用于储蓄或减债。

要点

如果雇主提前通知你,你的工作会受到大规模裁员的影响,那么你就有必要立即制定财务计划,以便为失业带来的各种变化做好准备。

充分评估你的遣散补偿方案,不要害怕协商相关条款,比如根据《统一综合预算协调法案》要求对医疗保险福利进行延期,以避免支付高昂保险费。如果你的雇主并不提供遣散补偿,则能够考虑申请失业保险,以满足自身眼下的财务需求。

滨崎说:“很少有雇主希望其员工与其商讨[遣散补偿方案]。如果他们感到此举将让其陷入不利的境地,不管是法律责任还是因为你的被迫离职感到后悔,那么你就会拥有更大的话语权和协商余地。”(财富中文网)

译者:冯丰

审校:夏林

2022年,为了应对创数十年来新高的通胀率以及随即可能出现的经济衰退,科技和媒体行业的多家巨头,例如推特(Twitter)、Meta和微软(Microsoft),均宣布了大规模的裁员计划。包括食品、交通和零售在内的其他行业则相继效仿,员工也开始担心自己的工作是否会受到影响。

如果你收到公司通知,成为了大规模裁员的对象之一,那么你就有必要立即制定计划,为下岗之后即将出现的重大经济状况变化做好准备。

被裁之后在资金管理方面应注意的五件事情

根据《职工调整与再培训通知法》(Worker Adjustment and Retraining Notification Act),某些公司,比如员工规模超过100名的公司,如果其员工的工作会因为大规模裁员或工厂关闭而受到影响,则至少应该提前60天告知员工。提前告知的初衷便是让员工能够有时间做好失业期间个人财务方面的准备。

失业后,管理自身资金的一些最佳方式包括:联系公司人力资源部门,索要可行的遣散费方案;申请失业救助,以补充自己的应急储蓄金;以及制定保险和401(K)计划应对策略。人们还有必要评估当前的开支习惯,并在颗粒无收之时削减不必要的开支。

联系人力资源部门

当你成为裁员对象之后,你的雇主会通知你是否有资格获得遣散补偿方案,该方案会列出解聘的资金补偿条款,包括按照员工被裁之前在该公司工作年限计算的遣散费和福利,还可能包括未使用的带薪假期或员工寻找新工作的补贴。

大多数雇员并没有意识到,遣散补偿方案与聘用方案一样,都是可以协商的。例如,如果你认为自己的应得补偿高于公司提供的补偿,你也能够要求公司提高补偿。你的雇主可以同意你的要求,也能够让公司按照最初的方案金额发放。

在接受之前,人们有必要认真地审核其遣散补偿方案,并了解其条款。接受遣散补偿协议可能意味着放弃以不当解聘为由起诉公司,或申请失业保险。通常,人们在接受协议之前有21天的考虑期。

值得一提的是,没有联邦或州法律要求雇主给雇员提供遣散补偿,除非员工加入了工会,或员工的聘用合同中列明了这一点。

申请失业保险

在失业之后,失业保险可以在你寻找新工作时帮助补充你的应急储蓄。你所在的州可能需要数周的时间来批准你的申请,因此,人们有必要在得知即将失业之时尽快申请该保险。

失业保险的资质要求和申请批准时限会根据申请人所在州的不同而发生变化,但各州往往对员工在某个公司的工作年限或收入金额有最低要求。你所在的州可能会使用这一信息来计算你的应得福利。

大多数州会提供高达26周的失业金,并要求希望继续获取失业金的人每周进行申报。一些州还可能会提出额外的资质要求,包括在领取补助时积极寻找新工作。因此,在申请之前请了解所在州的申领资质要求。

更新保险计划

如果你的保险计划是由雇主代缴的,那么你的保险福利通常在被裁后就会终止。

作为应对举措,联邦政府出台了《统一综合预算协调法案》(Consolidated Omnibus Budget Reconciliation Act),在员工被裁之后限时延长员工获取前雇主医疗保险的时限,通常最多延长36个月。然而,按照《统一综合预算协调法案》,下岗员工需要支付一笔保险费用,并另行支付2%的管理费,才有资格获取保险,其价格通常高于普通的保险计划。

如果不愿意为了延长当前的保险而支付高额费用,那么人们可能就有资格使用《平价医疗法案》(Affordable Care Act)提供的保险,该法案征收的保费更低,通常以收入水平为基础计算。如果失业员工不满26岁,还可以使用配偶或父母的保险。

评估401(k)计划

在失业之后评估如何处理401(K)计划时,有多个做法能够考虑,包括将资金留在当前计划,将你的计划转存至新雇主或个人退休账户,或全部取现。不同的选择可能会产生额外的税赋。

维持当前的计划:如果你的401(K)计划账户中的金额达到了5,000美元或以上,你就可以将资金留在当前的计划。即便你获准保留该计划,但你在72岁之前将无法再缴纳或提取资金。等到了72岁,无论你是在工作还是退休,你都得从计划中领取最低的分配额。

这意味着,如果你希望继续在退休前往里面存钱,你就必须开设新的401(K)计划或个人退休账户。此外,如果在下岗后出现经济紧张的状况,你将无法使用你的退休储蓄金。

将计划转存至新雇主:如果你在下岗后找到了新工作,那么你就能够以相对简单的方式,通过联系此前计划的管理方,并完成要求的手续,将前雇主的计划转存至新雇主的计划,Mountain Wealth Planning的注册金融策划师艾米·滨崎说道。

需要注意的是,你的新401(K)计划可能拥有不同的规则、投资选项和费用。在决定转存资金之前请认真评估新雇主的计划,以确保它可以符合你的投资需求。

将你的计划转存至个人退休账户:如果你并不希望使用新雇主的401(K)计划,或新雇主并不提供类似计划,那么你就能够通过联系你的前计划管理机构,并要求它们将资金支付给个人退休账户管理机构,从而将退休储蓄金转移至个人退休账户。

你可以选择罗斯个人退休账户(Roth IRA)和传统个人退休账户,但此举可能会带来额外的税赋。例如,如果你的退休储蓄金在传统的401(K)计划中属于延迟纳税,那么转存至罗斯个人退休账户将被视作应税行为。

直接取现:如果你没有应急储蓄金,而且马上需要使用现金,你也能够把钱从你的401(K)计划中取出来。然而,这应该作为你在评估其他方法之后的最后一个手段,因为你必须支付普通收入所得税,而且如果你的岁数没有达到59.5岁,还得额外支付10%的提前取现罚金。

你还会损失资金原本在投资退休账户过程中累积的所有复利,而且从长期来看会对你的整个退休储蓄金带来负面影响。滨崎称:“在将401(K)计划变现之后,要达到此前水平所需的时间要长得多。”

削减开支

制定简单的预算并贯彻执行。如果你在被裁后依靠应急储蓄或可变收益来维持生活,你就应该评估自己的开支,并将其分为三个大类,以帮助削减不必要的开支。

必需项:很大一部分预算应该被用于支付账单,包括你的抵押贷款或租金支付、水电费、食物、燃油、最低还款额以及保险。这其中还包括学生贷款还款,但目前已经暂停,可以延期至2023年6月30日。

换句话说,你的必需项包括每个月的固定支出。这些支出应该成为你的首要考虑事项,尤其是在资金有限的情况下。

个人喜好项:预算的一小部分能够用于购买你想要购买的物品,比如在假日期间回家探望家人,或者购买新服装参加工作面试。然而,如果你近期成为了被裁对象,则应该减少自己以往在自由支配开支方面的花费。

滨崎表示:“我们首先必须考虑支付固定支出,因为在失业后,人们真的得勒紧裤腰带过日子。”这可能意味着在家做饭而不是去豪华餐厅,或者重新调整自己的假日购物计划。

储蓄和偿还债务:如果手头没有潜在的新工作,人们可能就得一边找新工作,一边延长应急储蓄的使用时间。如果出现这种情况,则应该把手头所有剩余资金放回储蓄中,以供今后使用。此外,如果你有信用卡或消费贷债务,不妨在最低还款额的基础上偿还更多的资金,以降低利息费用。

如果预算允许,不妨考虑采用50/30/20准则,也就是将50%的税后收入用于必需项开支,将30%用于个人喜好项,20%用于储蓄或减债。

例如,如果你的应急储蓄可以应付6个月的开支,每个月共计花费4,000美元。则应把2,000美元用于固定支出,1,200美元用于个人喜好项,800美元用于储蓄或减债。

要点

如果雇主提前通知你,你的工作会受到大规模裁员的影响,那么你就有必要立即制定财务计划,以便为失业带来的各种变化做好准备。

充分评估你的遣散补偿方案,不要害怕协商相关条款,比如根据《统一综合预算协调法案》要求对医疗保险福利进行延期,以避免支付高昂保险费。如果你的雇主并不提供遣散补偿,则能够考虑申请失业保险,以满足自身眼下的财务需求。

滨崎说:“很少有雇主希望其员工与其商讨[遣散补偿方案]。如果他们感到此举将让其陷入不利的境地,不管是法律责任还是因为你的被迫离职感到后悔,那么你就会拥有更大的话语权和协商余地。”(财富中文网)

译者:冯丰

审校:夏林

Several major corporations in tech and media industries, such as Twitter, Meta, and Microsoft, have announced massive layoffs in 2022 in response to decades-high inflation rates that hint toward the possibility of a recession. Other industries including food, transportation, and retail have followed suit, which leaves workers wondering if their role will be impacted.

If you were informed that your job is among those impacted by a mass layoff, it’s important to create a plan right away so you can prepare for the major financial changes that come with being laid off.

5 things to do with your money when you’re laid off

Certain businesses—such as those that employ 100-plus workers—are required to provide employees a minimum of 60 days’ notice that their role will be impacted by a mass layoff or plant closing under the Worker Adjustment and Retraining Notification (WARN) Act. The hope in providing advance notice is that employees have time to prepare themselves financially in the event they are unemployed for a period of time.

Some of the best ways to manage your money after a layoff include contacting your human resources department for available severance packages, filing for unemployment to supplement your emergency savings, and having a strategy for dealing with your insurance and 401(k) plans. It’s also important to review your current spending habits and cut back unnecessary purchases while you are without income.

Contact HR

When you are laid off, your employer will inform you whether you will be entitled to a severance package which outlines the financial terms of your termination. This generally includes severance pay and benefits based on how long you were employed by your company before you were laid off. It also may include unused paid time off or assistance in finding a new job.

Most employees are unaware that severance packages can be negotiated the same way an employment offer can be. For instance, if you believe you are entitled to a larger severance payment than your company is offering, you may make a request to increase the payout. Your employer has the option to agree to your offer or hold firm on the original payout amount.

It’s important to throroughly review your severance package and understand the terms of the agreement before accepting it. Accepting your severance agreement may waive your right to file a wrongful termination suit or file for unemployment insurance. Typically, you will have up to 21 days to accept the agreement.

It’s important to note that there is no federal or state law that requires employers to provide employees with a severance package—unless you belong to a union or your employment contract states otherwise.

File for unemployment insurance

If you are laid off, unemployment insurance can help supplement your emergency savings while you look for a new job. It may take up to several weeks for your state to approve your application, so it is important to apply as soon as possible once you know your role will be terminated.

Unemployment insurance eligibility requirements and application approval timelines vary depending on which state you reside in, but it is typical for states to require you to have worked for a minimum amount of time or made a minimum amount of income to qualify. Your state may also use this information to calculate how much benefit you qualify for.

Most states provide unemployment benefits for up to 26 weeks and require you to file a weekly claim to continue receiving payments. Some states may also have additional qualification requirements, including that you actively look for new employment while you receive the benefit. Review your state’s eligibility requirements before applying.

Update your insurance plans

If your insurance plans are through your employer, your insurance benefits typically end when you are laid off.

To combat this, the federal government created the Consolidated Omnibus Budget Reconciliation Act (COBRA) to provide extended access to your previous employer’s health care plan for a limited time after you are laid off, usually lasting up to 36 months. But, you are required to pay a premium and an additional 2% administrative fee to qualify for insurance under COBRA, which usually is more expensive than a typical insurance plan.

Instead of paying high fees to extend your current coverage, you may be eligible to enroll in coverage under the Affordable Care Act, which typically offers lower premiums based on your income level. You may also qualify for coverage under a spouse’s or parent’s plan—if you are under 26 years old.

Review your 401(k) plan

There are several options to consider when evaluating what to do with your 401(k) plan when you are laid off, including leaving the funds in your current plan, rolling your plan over to a new employer or IRA, or cashing out entirely. Depending on which you choose, there may be additional tax implications.

Stick with your current plan: If you have $5,000 or more in your 401(k) plan, you may be able to leave the funds in your current plan. Even though you are allowed to keep the plan, you will no longer be able to contribute or withdraw funds until you hit age 72, which is when you will be required to take minimum distributions from the plan regardless of your employment or retirement status.

This means you will have to open a new 401(k) plan or IRA if you want to continue saving toward retirement. Additionally, you will not be able to dip into your retirement savings if you face financial turmoil while you are laid off.

Roll over your plan to a new employer: If you find a new job after being laid off, you can roll over your previous employer’s plan into your new employer’s plan relatively easily by contacting your previous plan’s administrator and completing required paperwork, says Amy Hamasaki, certified financial planner at Mountain Wealth Planning.

It’s important to note that your new 401(k) plan may have different rules, investment options, and fees. Review your new employer’s plan thoroughly to ensure it aligns your investment needs before deciding to rollover your funds.

Roll over your plan to an IRA: If you don’t want to use your new employer’s 401(k) plan or it does not offer one, you can transfer your retirement savings into an IRA by contacting your previous plan’s administrator and requesting they disburse the funds to your IRA administrator.

You can choose between a Roth IRA and a traditional IRA, but there may be additional tax consequences in doing so. For instance, if your retirement savings have been growing tax-deferred in your traditional 401(k) plan, a Roth IRA rollover would be considered a taxable event.

Cash out your plan: If you do not have an emergency savings built up and are in immediate need of cash, you may be able to cash out the funds from your 401(k). But this should be a last resort after evaluating other alternatives since you will be required to pay ordinary income taxes on the funds and an additional 10% early withdrawal penalty if you have not reached age 59½.

You also lose out on any compounding interest you would have accumulated if the funds remained invested in a retirement account and will adversely affect your overall retirement savings in the long run. “If you cash out of a 401(k), it is going to take you a lot longer to catch up to where you once were,” says Hamasaki.

Dial back on spending

Create a simple budget and stick to it. If you are living off your emergency savings or a variable income to support you following a layoff, you should review your expenses and break them down into three major categories to help you dial back on unnecessary spending.

Must-haves: A significant portion of your budget should be allocated to paying your bills, which include your mortgage or rent payments, utilities, food, gas, minimum loan payments, and insurance. This also includes student loan payments, which are currently on pause until no later than June 30, 2023.

In other words, your must-haves include your fixed expenses that you pay every month. These expenses should be your main priority, especially if you have limited funds.

Wants: A smaller portion of your budget may go toward paying for things you want, such as traveling home to visit your family during the holidays or purchasing a new outfit to attend a job interview. But you should reduce the amount you typically spend on discretionary expenses if you have recently been laid off.

“We’re really focusing on paying off the fixed expenses first because when the sky is falling down, you want to really tighten your belt a little bit,” says Hamasaki. This might mean eating in instead of going out to lavish restaurants or readjusting your holiday shopping plans.

Savings and paying off debt: If you do not have a job lined up, you may need to stretch your emergency savings to last a longer period of time while you search for a new role. If this is the case, it may be beneficial to put any excess back into your savings for a later date. Additionally, if you have credit card or consumer loan debt, you might want to make additional payments beyond your minimum payment to reduce interest charges.

If your budget allows, consider following the 50/30/20 rule, which allocates 50% of your after-tax income to must-have expenses, 30% to wants, and 20% to savings or paying down debt.

For instance, let’s say you have six months of expenses saved up in your emergency savings, totaling $4,000 per month. You should spend $2,000 on your fixed expenses, $1,200 on wants, and $800 on savings or paying down debt.

The takeaway

If your employer has given you advance notice that your job will be impacted by a mass layoff, it’s important to create a financial plan right away so you can be prepared for the changes that come along with losing your job.

Thoroughly review your severance package and don’t be afraid to negotiate the terms, such as requesting an extension of your health insurance benefits to avoid paying high premiums under COBRA. If your employer will not be providing severance pay, consider applying for unemployment insurance to meet your immediate financial needs.

“Not too many employers expect anyone to negotiate with them [on their severance package],” says Hamasaki. “But if they feel that this is putting them in a precarious situation, whether it’s a legal liability or they feel remorseful that they had to let you go, there could be more room for power and negotiation.”

请打开财富Plus APP