选择机器人为你管钱之前,要考虑什么?

Kevin L. Matthews II

2022-10-08

机器人顾问很擅长跑直线,但真人顾问可能更擅长转弯。

文本设置

文本设置

Plus(0条)

Plus(0条)

直到最近,股票市场门槛才低到许多人都可以入市。曾经有几十年,投资者需要打电话给经纪人来买卖股票或获取最新的股票报价。但随着在线交易应用和机器人顾问的兴起,几乎任何人都比以往任何时候更容易进行投资。

第一个机器人顾问于2010年问世,自那以后这一领域得到了显著发展:根据德勤(Deloitte)的一份报告,预计到2025年,机器人顾问管理的资产将超过16万亿美元。虽然这项技术仍然相当新,但对于投资者来说,了解机器人顾问是什么、它是如何工作的,以及在使用机器人顾问投资股市之前需要考虑什么是很重要的。

机器人顾问是什么?

机器人顾问是一种在线金融服务,根据您在设置账户或注册服务时共享的信息,提供投资建议和自动投资组合管理。

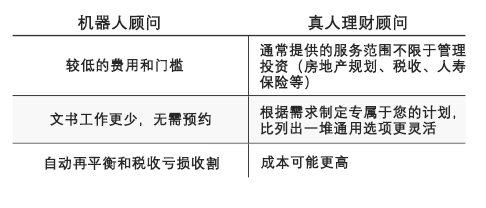

与一些传统咨询公司相比,机器人顾问提供这些服务的成本很低,这使它们成为有吸引力的选择。而在传统咨询公司那里,客户要拥有2.5万至20万美元甚至更多的资金才能开立账户,并获得专家的投资管理建议。

机器人顾问是如何工作的?

有超过100种不同的机器人顾问可供选择,其中大多数都遵循相同的基本工作流程。机器人顾问要求新用户在设置账户时填写一份简短的问卷,然后根据这些答案,利用算法自动选择投资项目。

问卷通常会询问用户的年龄、风险承受能力、退休前计划工作多长时间,以及评估其对股市涨跌的反应。所有这些数据点都用于确定投资组合的资产配置,通常包括股票、债券和仍能获得固定回报的未投资现金的组合。

然后,机器人顾问将选择投资项目并管理投资,并随着时间的推移对投资组合进行定期调整,这通常包括重新平衡投资组合和税收亏损收割。这个过程将自动进行,几乎不需要用户进行任何操作。

除了创建自动化投资组合外,机器人顾问还有以下优势:

• 与传统财务顾问相比,费用更低

• 较低的开户资金要求

• 避免人为错误和偏见

• 自动再平衡

• 无需安排会议或担心日程安排

• 可以自动从外部帐户中提取信息,以便您可以在一处查看所有信息

“它们的最大优势是低成本。”Pashman Financial公司的所有者、注册理财规划师马克斯·帕什曼(Max Pashman)说。他还表示:“与真人顾问通常收取1%或更多的平均费率相比,您可以以非常低的管理费管理您的投资组合。通过机器人顾问开户通常没有最低要求,文书工作和研究也更少,这对新投资者来说是一个很好的起点。”

机器人顾问的费用取决于您选择的公司,但费用通常包括……

• 管理费:这是直接支付给机器人顾问的费用。

• 费用比率:机器人顾问为您选择的基金也可能要收取费用。

管理费通常为每年0.25%左右,也就是说,每投资1,000美元收取5美元的管理费。有些机器人顾问根本不收取管理费。

费用比率包含在为您的投资组合选择的每个特定ETF(交易所交易基金)中,并从ETF创建者那里收取,而不是从机器人顾问那里收取。机器人顾问提供的大多数ETF的费用比率每年从0.05%到0.25%不等,即每投资1,000美元收取0.50美元到2.50美元。有少数机器人顾问不收取费用比率。

一些机器人顾问提供咨询真人顾问的选项,每月额外收费约30美元。

机器人顾问与真人顾问之比较

有多种方法可以衡量帮助您管理财务的最佳选择是机器人顾问还是真人顾问。如果您正在寻找一种自动化的、低成本的理财方式,那么机器人顾问可能会更适合您。对于那些想要一对一的关注和更有针对性的策略的人来说,真人顾问可能是更好的选择。以下是两者之间的其他方面的比较。

真人理财顾问的一个被低估的优势是,当市场低迷时,他们可以为您提供帮助,避免您做出任何有悖于传统投资智慧的草率决定。

帕什曼说:“受市场恐慌的影响,投资者可能会试图自己撤出所有资金。通过先咨询真人顾问,顾问可以安抚客户,防止他们过早抛售,而事实证明,这种情况比我们想的更常见。”

在尝试机器人顾问之前要考虑什么

在选择机器人顾问还是传统顾问之前,您可能需要盘点一下自己的财务状况。可以在哪些领域接受更多的指导或自动化处理? 您对顾问的期望是什么?

“在这里,人们应该更多考虑投资组合以外的领域;当真人理财顾问帮助您度过艰难的财务转型时,您会产生一种情感联系。”Wealth Enhancement Group的理财顾问、注册理财规划师帕特里克•博宾斯(Patrick Bobbins)表示。“所有这些情感和身体特征都应该被考虑在内,而不是只考虑由计算机算法生成的最佳资产配置。”

请记住,您的选择并不是一成不变的,随着时间的推移,您的财务状况会发生变化,您可以选择最有效的方案。

•财务目标:了解自己的目标可能是在机器人顾问和真人顾问之间做出选择的最重要的决定因素之一。虽然机器人顾问可以有效地管理您的投资决策,但真人顾问可能最适合做更复杂的决策,比如帮助您选择合适的学生贷款还款计划或比较新工作的薪酬待遇。

•成本:如果成本是一个考虑因素,机器人顾问通常会胜出。但一定要量化您从这个成本中获得的价值,以及任何所需的最低成本。

•投资风格:您是喜欢“一劳永逸”模式的放任型投资者吗?还是您更喜欢投资股票?考虑到机器人顾问平台在投资选择方面的局限性,很有必要考虑这些问题。

• 专业化:您是否有可能影响您理财的特殊考虑?例如,企业主有不同的退休计划选择和房产规划考虑。

要点

在真人顾问和机器人顾问之间进行选择取决于您财务状况的复杂程度。对于那些有更直接目标的人来说,机器人顾问可能是一个不错的选择。

但对于那些有复杂财务需求并想要更多私人接触的人来说,真人顾问可能是最好的选择。

换句话说,机器人顾问很擅长跑直线,但真人顾问可能更擅长转弯。(财富中文网)

编辑披露:本文中包含的建议、意见或排名出自Fortune Recommends™编辑团队。本内容未经任何合作伙伴或其他第三方审查,也未得到任何合作伙伴或其他第三方认可。

译者:中慧言-王芳

直到最近,股票市场门槛才低到许多人都可以入市。曾经有几十年,投资者需要打电话给经纪人来买卖股票或获取最新的股票报价。但随着在线交易应用和机器人顾问的兴起,几乎任何人都比以往任何时候更容易进行投资。

第一个机器人顾问于2010年问世,自那以后这一领域得到了显著发展:根据德勤(Deloitte)的一份报告,预计到2025年,机器人顾问管理的资产将超过16万亿美元。虽然这项技术仍然相当新,但对于投资者来说,了解机器人顾问是什么、它是如何工作的,以及在使用机器人顾问投资股市之前需要考虑什么是很重要的。

机器人顾问是什么?

机器人顾问是一种在线金融服务,根据您在设置账户或注册服务时共享的信息,提供投资建议和自动投资组合管理。

与一些传统咨询公司相比,机器人顾问提供这些服务的成本很低,这使它们成为有吸引力的选择。而在传统咨询公司那里,客户要拥有2.5万至20万美元甚至更多的资金才能开立账户,并获得专家的投资管理建议。

机器人顾问是如何工作的?

有超过100种不同的机器人顾问可供选择,其中大多数都遵循相同的基本工作流程。机器人顾问要求新用户在设置账户时填写一份简短的问卷,然后根据这些答案,利用算法自动选择投资项目。

问卷通常会询问用户的年龄、风险承受能力、退休前计划工作多长时间,以及评估其对股市涨跌的反应。所有这些数据点都用于确定投资组合的资产配置,通常包括股票、债券和仍能获得固定回报的未投资现金的组合。

然后,机器人顾问将选择投资项目并管理投资,并随着时间的推移对投资组合进行定期调整,这通常包括重新平衡投资组合和税收亏损收割。这个过程将自动进行,几乎不需要用户进行任何操作。

除了创建自动化投资组合外,机器人顾问还有以下优势:

• 与传统财务顾问相比,费用更低

• 较低的开户资金要求

• 避免人为错误和偏见

• 自动再平衡

• 无需安排会议或担心日程安排

• 可以自动从外部帐户中提取信息,以便您可以在一处查看所有信息

“它们的最大优势是低成本。”Pashman Financial公司的所有者、注册理财规划师马克斯·帕什曼(Max Pashman)说。他还表示:“与真人顾问通常收取1%或更多的平均费率相比,您可以以非常低的管理费管理您的投资组合。通过机器人顾问开户通常没有最低要求,文书工作和研究也更少,这对新投资者来说是一个很好的起点。”

机器人顾问的费用取决于您选择的公司,但费用通常包括……

• 管理费:这是直接支付给机器人顾问的费用。

• 费用比率:机器人顾问为您选择的基金也可能要收取费用。

管理费通常为每年0.25%左右,也就是说,每投资1,000美元收取5美元的管理费。有些机器人顾问根本不收取管理费。

费用比率包含在为您的投资组合选择的每个特定ETF(交易所交易基金)中,并从ETF创建者那里收取,而不是从机器人顾问那里收取。机器人顾问提供的大多数ETF的费用比率每年从0.05%到0.25%不等,即每投资1,000美元收取0.50美元到2.50美元。有少数机器人顾问不收取费用比率。

一些机器人顾问提供咨询真人顾问的选项,每月额外收费约30美元。

机器人顾问与真人顾问之比较

有多种方法可以衡量帮助您管理财务的最佳选择是机器人顾问还是真人顾问。如果您正在寻找一种自动化的、低成本的理财方式,那么机器人顾问可能会更适合您。对于那些想要一对一的关注和更有针对性的策略的人来说,真人顾问可能是更好的选择。以下是两者之间的其他方面的比较。

真人理财顾问的一个被低估的优势是,当市场低迷时,他们可以为您提供帮助,避免您做出任何有悖于传统投资智慧的草率决定。

帕什曼说:“受市场恐慌的影响,投资者可能会试图自己撤出所有资金。通过先咨询真人顾问,顾问可以安抚客户,防止他们过早抛售,而事实证明,这种情况比我们想的更常见。”

在尝试机器人顾问之前要考虑什么

在选择机器人顾问还是传统顾问之前,您可能需要盘点一下自己的财务状况。可以在哪些领域接受更多的指导或自动化处理? 您对顾问的期望是什么?

“在这里,人们应该更多考虑投资组合以外的领域;当真人理财顾问帮助您度过艰难的财务转型时,您会产生一种情感联系。”Wealth Enhancement Group的理财顾问、注册理财规划师帕特里克•博宾斯(Patrick Bobbins)表示。“所有这些情感和身体特征都应该被考虑在内,而不是只考虑由计算机算法生成的最佳资产配置。”

请记住,您的选择并不是一成不变的,随着时间的推移,您的财务状况会发生变化,您可以选择最有效的方案。

•财务目标:了解自己的目标可能是在机器人顾问和真人顾问之间做出选择的最重要的决定因素之一。虽然机器人顾问可以有效地管理您的投资决策,但真人顾问可能最适合做更复杂的决策,比如帮助您选择合适的学生贷款还款计划或比较新工作的薪酬待遇。

•成本:如果成本是一个考虑因素,机器人顾问通常会胜出。但一定要量化您从这个成本中获得的价值,以及任何所需的最低成本。

•投资风格:您是喜欢“一劳永逸”模式的放任型投资者吗?还是您更喜欢投资股票?考虑到机器人顾问平台在投资选择方面的局限性,很有必要考虑这些问题。

• 专业化:您是否有可能影响您理财的特殊考虑?例如,企业主有不同的退休计划选择和房产规划考虑。

要点

在真人顾问和机器人顾问之间进行选择取决于您财务状况的复杂程度。对于那些有更直接目标的人来说,机器人顾问可能是一个不错的选择。

但对于那些有复杂财务需求并想要更多私人接触的人来说,真人顾问可能是最好的选择。

换句话说,机器人顾问很擅长跑直线,但真人顾问可能更擅长转弯。

编辑披露:本文中包含的建议、意见或排名出自Fortune Recommends™编辑团队。本内容未经任何合作伙伴或其他第三方审查,也未得到任何合作伙伴或其他第三方认可。(财富中文网)

译者:中慧言-王芳

It wasn’t until fairly recently that investing in the stock market became accessible to so many people. For decades, investors would need to call up a broker to buy and sell stocks or to get the most up-to-date stock quote. But with the rise of online trading apps and robo-advisors, it’s easier than ever for practically anyone to invest.

The first robo-advisor was introduced in 2010, and the space has grown notably since: It’s predicted to manage over $16 trillion by 2025, according to a report by Deloitte. While this technology still fairly new, it’s important for investors to understand what a robo-advisor is, how it works, and the factors to consider before using one to invest in the stock market.

What is a robo-advisor?

A robo-advisor is an online financial service that offers investment advice and automated portfolio management based on the information you share when you set up your account or sign up for the service.

Robo-advisors provide these services at a low cost, which makes them an attractive option when compared with some traditional advisory firms that can require clients to have anywhere between $25,000 and $200,000 or more to open an account and have access to an expert who will help you manage your investments.

How do robo-advisors work?

There are more than 100 different robo-advisors to choose from, with most following the same basic working structure. Robo-advisors ask new users to fill out a short questionnaire when setting up their account, and based on those answers, automatically select investments using an algorithm.

The questionnaire will typically ask for your age, risk tolerance, and how long you plan to work before retirement, as well as gauge how you might react to the ups and downs of the stock market. All these data points are used to determine your portfolio’s asset allocation, which typically includes a combination of stocks, bonds, and uninvested cash that will still earn a fixed return.

From there, the robo-advisor will select and manage your investments with periodic adjustments to your portfolio over time, which generally includes rebalancing the portfolio and tax-loss harvesting. This process will take place automatically, with little to no action required on your part.

In addition to creating an automated portfolio, robo-advisors can also offer their customers the following benefits:

• Lower fees compared with a traditional financial advisor

• Lower capital required to start

• The ability to avoid human error and bias

• Automatic rebalancing

• No need to set up meetings or worry about scheduling

• Can pull information from outside accounts automatically so you can see them all in one place

“The biggest advantage they provide is low cost,” says Max Pashman, a CFP and owner of Pashman Financial. “You can have your portfolio managed for a very low management fee compared to the average rate of an advisor that typically charges 1% or more to invest [your] money,” he says. “There is generally no required minimum to open an account with a robo-advisor and less paperwork and research, making it a good starting point for new investors.”

The cost of a robo-advisor depends on the company you choose, but any fees will usually include…

• A management fee: This is a fee that is paid directly to the robo-advisor.

• An expense ratio: There may also be a fee for the funds the robo-advisor selects on your behalf.

Management fees are typically around 0.25% per year, which would amount to $5 for every $1,000 invested. There are some robo-advisors that do not charge a management fee at all.

Expense ratios are built into each of the specific ETFs (exchange-traded funds) that are selected for your portfolio and collected from the creator of the ETF, not the robo-advisor. Expense ratios for most of the ETFs provided by robo-advisors can range from 0.05% to 0.25% each year, which is between $0.50 and $2.50 for every $1,000 invested. There are a handful of robo-advisors that do not charge expense ratios.

Some robo-advisors offer optional access to human advisors for an additional fee of about $30 per month.

Robo-advisor vs. human advisor

There are multiple ways to gauge whether a robo-advisor or a human advisor is best to help you manage your finances. If you’re looking for an automated, low-cost way to manage your finances, a robo-advisor might feel like a natural fit. For those who want the one-on-one attention and a more tailored approach, a human financial advisor may prove the better option. Below are additional comparisons between the two.

One understated advantage of a human financial advisor is they could help you avoid making any rash decisions that override conventional investing wisdom when the market is experiencing a downturn.

“An investor may be tempted to pull all their funds out on their own, influenced by fear in the market,” says Pashman. “By consulting with a human advisor first, the advisor can calm the client and prevent them from prematurely selling off too soon, which turns out to be more common than we’d like.”

What to consider before trying a robo-advisor

Before making the choice between a robo-advisor and a traditional advisor you may want to take inventory of your finances. What are the areas where you could use more guidance or automation? What are your expectations for an advisor?

“What people should consider here is more outside the realm of what the investment portfolio looks like; it is the emotional connection you have when a real-life advisor helps walk you through a tough financial transition,” says Patrick Bobbins, CFA, a financial advisor at Wealth Enhancement Group. “All of these more emotional and physical characteristics should be considered—not what optimal asset allocation is generated by the computer algorithm.”

Keep in mind that your choice isn’t set in stone, and as your financial situation changes over time you can switch to the option that works best.

• Financial goals: Knowing your goals can be one of the most important determining factors in deciding between a robo-advisor and a human one. While a robo-advisor can be efficient in managing your investing decisions, a human advisor may be best for more complex decisions like helping you choose the right student loan repayment plan or comparing compensation packages for a new job.

• Cost: If cost is a factor, robo-advisors typically win out here. But make sure you quantify the value you’re getting for that cost as well as any required minimums.

• Investment style: Are you a hands-off investor who enjoys the “set it and forget it” model? Or do you prefer to invest in stocks? These questions are important to consider given the limitations of what robo-advisor platforms offer in terms of investment options.

• Specialization: Do you have special considerations that could impact your finances? For example, business owners have different retirement plan options and estate planning considerations.

The takeaway

Choosing between a human advisor and robo-advisor comes down to the level of complexity in your financial situation. For those who have more straightforward goals, a robo-advisor may be a good fit.

But for those who have complex financial needs and want more of a personal touch, a human advisor may prove the best option.

In other words, robo-advisors are great for running in a straight line, but human advisors may be better at turning corners.

EDITORIAL DISCLOSURE: The advice, opinions, or rankings contained in this article are solely those of the Fortune Recommends™ editorial team. This content has not been reviewed or endorsed by any of our affiliate partners or other third parties.

请打开财富Plus APP