股价暴跌、大裁员,这家线上二手车交易平台何去何从?

JACOB CARPENTER

2022-06-04

在疫情期间业绩暴涨的Carvana如今陷入困境。

文本设置

文本设置

Plus(0条)

Plus(0条)

美国最大的线上二手车交易商Carvana在过去十年中一直在铆足马力向前冲。

这家公司借助人们对亚马逊式购车体验的强劲需求,帮助客户规避了到访车场以及与固执销售人员打交道的种种不便。

然后,新冠疫情爆发了,尽管人们在疫情初期一片恐慌,但Carvana的业务却一路高歌,因为在全球芯片短缺、汽车产量下滑的大环境下,买家很难买到新车。

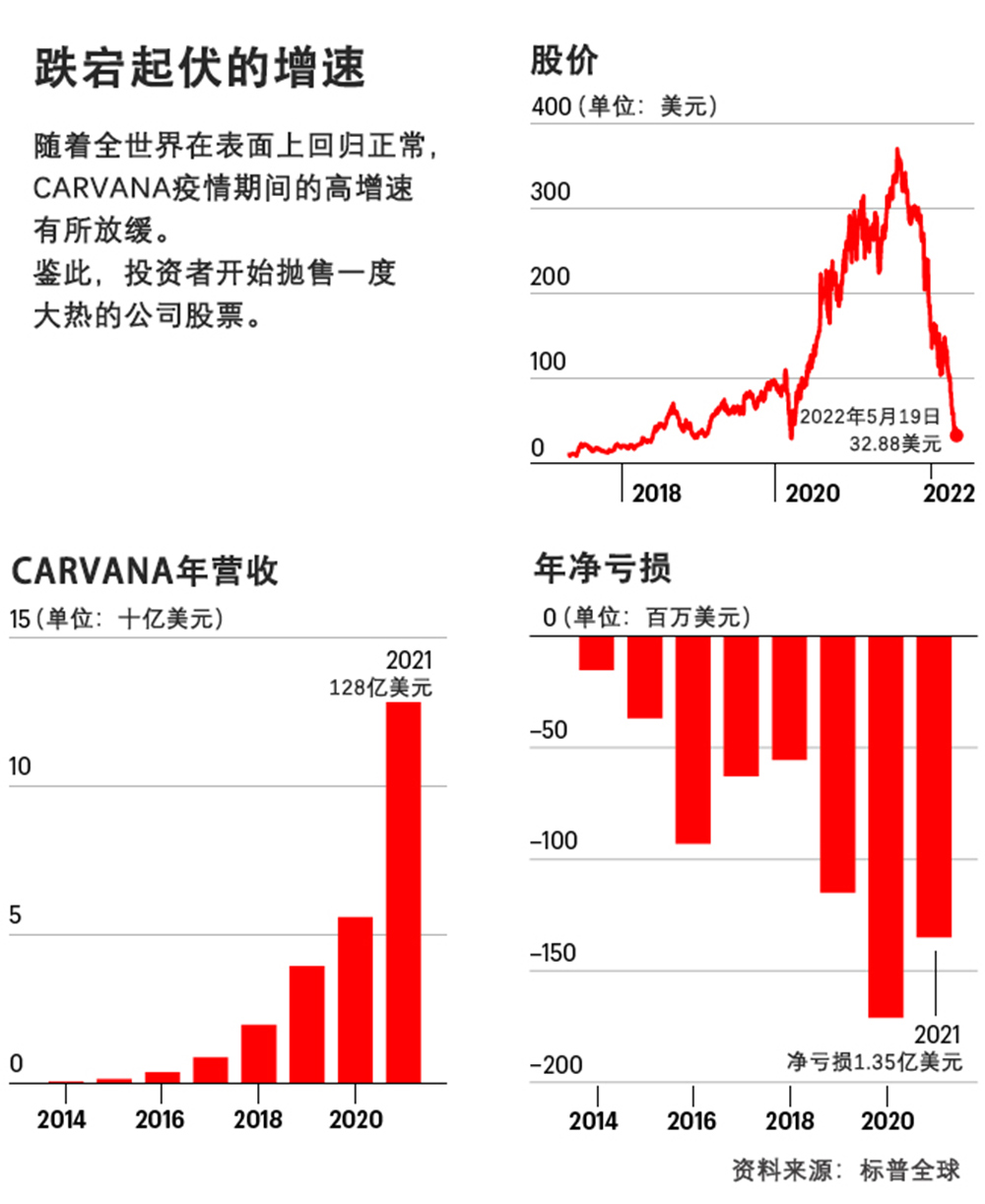

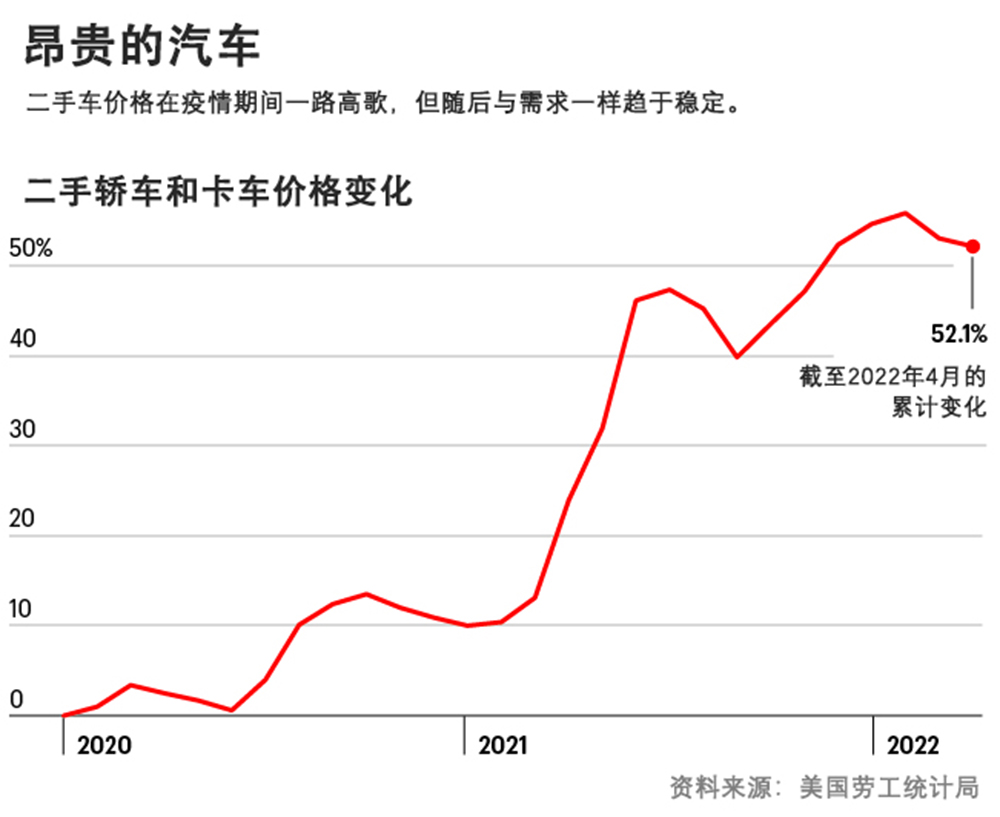

然而从2021年底开始,Carvana的好景却戛然而止。随着疫情退潮,很多购车者开始再次光顾当地汽车经销商。与此同时,居高不下的二手车价格,不断上涨的车贷款利率,以及宏观经济通胀导致钱包见底,让很多人不得不重新考虑是否花钱购买一辆新车。

突然间,Carvana因对未来快速增长的预期而开展的疯狂招聘,以及庞大的汽车库存,让公司反受其害。在过去三个季度中,公司总亏损扩大至3.81亿美元。

前些年,投资者对Carvana因发展成本而造成的亏损并不在意。确实,在他们的帮助下,公司的股价从2020年3月的低点飙升至2021年8月的顶峰,增长了12倍。然而最近,市场疯了:截至5月,公司的股价从其高点暴跌了90%,华尔街也开始怀疑,当前的重挫到底是一个小小的失足,还是一蹶不振的惨败。

Carvana首席执行官欧内斯特·加西亚三世对《财富》说:“全世界都在质问我们,质问经济,质问整个行业。这都没什么,也是必然的。我们的工作是最大化地利用涌现出来的各种机遇,并尽自己所能进行调整。如果我们做到了,而且我们在过去做到过,那么故事的结局将是美好的,并不是负面的。”

加西亚的父亲创建了Carvana的前身DriveTime,后者是一家实体二手车经销商和融资机构。Carvana是该公司的线上业务,最终独立成为了一家自营公司。该公司最为知名的莫过于令人眼前一亮的玻璃“贩卖机”,客户可通过放入定制的客户币来取走车辆。(Carvana也提供送货上门服务。)

对于加西亚的员工来说,如今的挑战在于如何迅速地削减公司的开支,并在2023年之前回归盈利。去年,Carvana实现了两个季度的盈利(不计某些费用),这在公司历史上尚属首次。

面对新局势,Carvana在五月采取了初步举措,宣布裁员12%(2500人)。高管还计划削减薪酬、广告和物流开支。

Carvana过紧日子的举措恰逢其在5月以22亿美元收购ADESA这个糟糕时机,后者是一家领先的车辆批发拍卖公司。Carvana计划使用ADESA的56个设施来翻新和存储车辆,继而实现新市场的业务增长。然而,分析师担心,公司为资助收购而发行的高利率债券将在未来数年蚕食掉Carvana现有的大部分现金。

尽管Carvana似乎在短期内前景黯淡,但分析师表示,Carvana也并非是软柿子,它是线上二手车市场中的主导零售商,去年卖出了42.52万辆车,是仅次于其后的纯线上竞争对手Vroom的几乎六倍。

相对于意欲进军线上市场的传统二手车经销商,Carvana也有着很大的优势。例如,知名竞争对手中规模最大的CarMax在线上的销售量仅占其总销量的9%,还不到8.77万辆。

基于公司去年强劲的业绩,Carvana在新发布的《财富》500强榜单中的名次有了大幅提升。公司营收增长了129%,达到128亿美元,让公司在榜单中的名次跃升了193个,至290位,是今年以来排名上升第三快的公司。

即便在经历了过去十年的快速增长之后,Carvana在二手车市场依然仅占有1%的市场份额。公司高管认为年销量200万辆是一个可以实现的目标。

Wedbush Securities的分析师赛斯·巴沙姆预测,Carvana在现金用完之前便会扭亏为盈(扣除某些费用之后),但投资者要止血的话可能得等到2024年。

巴沙姆表示:“即便是最有力的竞争对手依然难以望其项背。我认为当前的局势最终并不会让该公司大幅偏离其努力实现的目标。”(财富中文网)

译者:冯丰

审校:夏林

美国最大的线上二手车交易商Carvana在过去十年中一直在铆足马力向前冲。

这家公司借助人们对亚马逊式购车体验的强劲需求,帮助客户规避了到访车场以及与固执销售人员打交道的种种不便。

然后,新冠疫情爆发了,尽管人们在疫情初期一片恐慌,但Carvana的业务却一路高歌,因为在全球芯片短缺、汽车产量下滑的大环境下,买家很难买到新车。

然而从2021年底开始,Carvana的好景却戛然而止。随着疫情退潮,很多购车者开始再次光顾当地汽车经销商。与此同时,居高不下的二手车价格,不断上涨的车贷款利率,以及宏观经济通胀导致钱包见底,让很多人不得不重新考虑是否花钱购买一辆新车。

突然间,Carvana因对未来快速增长的预期而开展的疯狂招聘,以及庞大的汽车库存,让公司反受其害。在过去三个季度中,公司总亏损扩大至3.81亿美元。

前些年,投资者对Carvana因发展成本而造成的亏损并不在意。确实,在他们的帮助下,公司的股价从2020年3月的低点飙升至2021年8月的顶峰,增长了12倍。然而最近,市场疯了:截至5月,公司的股价从其高点暴跌了90%,华尔街也开始怀疑,当前的重挫到底是一个小小的失足,还是一蹶不振的惨败。

Carvana首席执行官欧内斯特·加西亚三世对《财富》说:“全世界都在质问我们,质问经济,质问整个行业。这都没什么,也是必然的。我们的工作是最大化地利用涌现出来的各种机遇,并尽自己所能进行调整。如果我们做到了,而且我们在过去做到过,那么故事的结局将是美好的,并不是负面的。”

加西亚的父亲创建了Carvana的前身DriveTime,后者是一家实体二手车经销商和融资机构。Carvana是该公司的线上业务,最终独立成为了一家自营公司。该公司最为知名的莫过于令人眼前一亮的玻璃“贩卖机”,客户可通过放入定制的客户币来取走车辆。(Carvana也提供送货上门服务。)

对于加西亚的员工来说,如今的挑战在于如何迅速地削减公司的开支,并在2023年之前回归盈利。去年,Carvana实现了两个季度的盈利(不计某些费用),这在公司历史上尚属首次。

面对新局势,Carvana在五月采取了初步举措,宣布裁员12%(2500人)。高管还计划削减薪酬、广告和物流开支。

Carvana过紧日子的举措恰逢其在5月以22亿美元收购ADESA这个糟糕时机,后者是一家领先的车辆批发拍卖公司。Carvana计划使用ADESA的56个设施来翻新和存储车辆,继而实现新市场的业务增长。然而,分析师担心,公司为资助收购而发行的高利率债券将在未来数年蚕食掉Carvana现有的大部分现金。

尽管Carvana似乎在短期内前景黯淡,但分析师表示,Carvana也并非是软柿子,它是线上二手车市场中的主导零售商,去年卖出了42.52万辆车,是仅次于其后的纯线上竞争对手Vroom的几乎六倍。

相对于意欲进军线上市场的传统二手车经销商,Carvana也有着很大的优势。例如,知名竞争对手中规模最大的CarMax在线上的销售量仅占其总销量的9%,还不到8.77万辆。

基于公司去年强劲的业绩,Carvana在新发布的《财富》500强榜单中的名次有了大幅提升。公司营收增长了129%,达到128亿美元,让公司在榜单中的名次跃升了193个,至290位,是今年以来排名上升第三快的公司。

即便在经历了过去十年的快速增长之后,Carvana在二手车市场依然仅占有1%的市场份额。公司高管认为年销量200万辆是一个可以实现的目标。

Wedbush Securities的分析师赛斯·巴沙姆预测,Carvana在现金用完之前便会扭亏为盈(扣除某些费用之后),但投资者要止血的话可能得等到2024年。

巴沙姆表示:“即便是最有力的竞争对手依然难以望其项背。我认为当前的局势最终并不会让该公司大幅偏离其努力实现的目标。”(财富中文网)

译者:冯丰

审校:夏林

Carvana, the nation’s largest online used auto dealer, has spent most of its 10-year journey with its accelerator punched to the floor.

The company capitalized on strong demand for an Amazon-like car shopping experience, helping customers avoid the inconveniences of visiting vehicle lots and haggling with pushy salespeople.

Then the COVID pandemic hit, and despite initial fears, Carvana’s business surged as buyers struggled to find new vehicles amid a global chip shortage that slowed production.

But starting in late 2021, Carvana’s joyride came to an abrupt halt. With the pandemic ebbing, many shoppers once again felt comfortable visiting local auto dealers. Meanwhile sky-high used car prices, rising interest rates on auto loans, and pinched pocketbooks caused by inflation across the broader economy made many people reconsider splurging on a new ride.

Suddenly Carvana’s aggressive hiring and its large inventory of cars—all pursued in anticipation of rapid future growth—backfired. Over the past three quarters, total losses ballooned to $381 million.

In previous years, investors were willing to shrug off Carvana’s losses as the cost of growth; indeed, they sent shares up 13-fold from their March 2020 low to their August 2021 peak. But recently the markets have lost their nerve: As of late May, the company’s stock was down 90% from its high, leaving Wall Street to wonder whether the current setback is a minor detour or an unrecoverable crash.

“The world is asking questions about us, about the economy, about the industry. And that’s fine. That’s going to happen,” Carvana CEO Ernie Garcia III tells Fortune. “Our job is to make the most of every opportunity that shows up and try to adjust the best we can. If we do, which we have in the past—in the end this story will be a positive one, not a negative one.”

Garcia’s father founded Carvana’s predecessor, DriveTime, a brick-and-mortar used car dealer and financier. That business spawned online arm Carvana, which was ultimately spun out into its own company. It’s perhaps best known for eye-catching glass-walled “vending machines,” where customers can pick up vehicles by inserting a custom coin. (Carvana also makes home deliveries.)

For Garcia’s crew, the challenge now is to quickly trim the company’s spending and return to profitability by 2023. Last year, Carvana reported two profitable quarters excluding certain expenses, its first in company history.

An initial step toward the new reality came in mid-May, when Carvana announced layoffs totaling 12% of its workforce, or 2,500 employees. Executives also plan to cut spending on compensation, advertising, and logistics.

Carvana’s commitment to belt-tightening coincides with an arguably ill-timed acquisition of ADESA, a leading wholesale vehicle auction company, for $2.2 billion in May. Carvana plans to use ADESA’s 56 facilities to refurbish and store vehicles, enabling growth into new markets. Analysts, however, fear the high-interest bonds issued to finance the purchase will eat up a large part of Carvana’s available cash for years to come.

While Carvana’s short-term prospects appear dim, analysts say the company is no lemon. It’s the dominant online used car retailer, selling 425,200 vehicles last year—nearly six times as many as its nearest online-only competitor, Vroom.

Carvana also has a big lead over traditional used car dealers that are trying to push online. For example, CarMax, the largest of the established rivals, sold only 9% of its cars online, or no more than 87,700 vehicles.

Based on its strong business last year, Carvana rose spectacularly on the latest Fortune 500. Revenue grew 129%, to $12.8 billion, vaulting the company 193 spots to No. 290 on the list—the third-biggest leap for any company this year.

Even after its rapid growth over the past decade, Carvana still owns only 1% of the used car market. Company officials believe annual sales of 2 million vehicles is a realistic target.

Wedbush Securities analyst Seth Basham forecasts that Carvana will turn the corner in terms of profits—excluding certain expenses—before it runs out of money, though investors may have to wait until 2024 for the bleeding to stop.

“They’re still way ahead of even the best competition out there,” Basham says. “I don’t think what’s happening now is ultimately going to lead to them arriving at a place much different than where they were headed.”

请打开财富Plus APP