世界大型企业联合会最新CEO调查:面对动荡的商业环境,企业如何维持繁荣发展

Anke Schrader, Charles Mitchell, 世界大型企业联合会

2022-04-01

中国的CEO们表示,未来,乌克兰危机和始终无法结束的新冠疫情只会让他们面临的许多压力更加恶化。许多公司和行业的组织结构与经营模式曾经大获成功,但当前的破坏性因素正在将它们淘汰,对人们的工作方式产生了深远影响。中国公司也不例外。

文本设置

文本设置

Plus(0条)

Plus(0条)

是什么让中国CEO们彻夜难眠?

新冠疫情已经进入了第三个年头,显然它是一场马拉松,而不是一次短跑比赛。在中国,疫情的负面后果仍然在持续给中国的经济和营商环境带来压力。

据世界大型企业联合会(The Conference Board)的年度企业高管前景展望调查显示,早在乌克兰危机之前,经济衰退风险、消费者行为变化、通胀加剧、全球政治动荡、全球贸易中断和利润缩水,是中国CEO们认为2022年影响最大的事件。每一个事件都与疫情的进展直接相关,需要公司紧急采取措施,包括经营模式转型、现金流管理、成本控制、供应链灵活性和旨在打造更有韧性、更灵活的团队的人力资源管理创新等。这都是中国CEO们认为急需执行的措施。俄乌冲突的影响将加剧中国企业面临的许多压力,使公司更迫切地需要采取措施减缓这些事件的影响。

然而,中国和全球的CEO们很少有人相信,面对从新疫情到通胀、气候变化和供应链中断等未来危机,他们的公司做好了充分准备。

中国人消费模式改变所带来的挑战:复杂的变化

新冠疫情改变了中国大多数地区消费者的购物行为,刺激了网络购物繁荣,给企业带来了挑战,迫使它们不得不转变经营模式,以跟上这种趋势。事实上,约40%的中国CEO将消费者行为改变列为公司在2022年面临的具有巨大影响的问题之一,这个比例是在美国和欧洲的CEO的两倍。但在中国,消费者行为的改变远比表面看起来更加复杂。

中国政府将电子商务视为未来经济增长的关键引擎,在疫情期间,电商业务繁荣发展,并且一直持续至今。新冠疫情使家庭消费模式从非必需品消费转变为食物等必需品消费。在疫情之前,城市家庭消费日益倾向于非必需品消费,而必需品消费的增长速度较慢;必需品消费在消费总额中的比例不断缩小。自疫情爆发以来,非必需品消费的增长速度显著下降。可支配收入增长放缓、相对疲软的劳动市场和为控制疫情执行的严格出行管制,正在抑制非必需品消费。2021年第4季度,线上零售额同比增长3.9%,远低于实现中国政府提出的2025年线上零售额增长目标需要达到的7%的年增长率。虽然今年1月和2月的数据令人振奋,但病例数增加和相关商业中断,将继续带来消费下行风险。

从商业的角度,针对消费者行为和态度的变化及其对业务的潜在影响,实时提供数据驱动的洞察极具挑战性。

导致通胀上升的原因及其持续时间:CEO们的观点

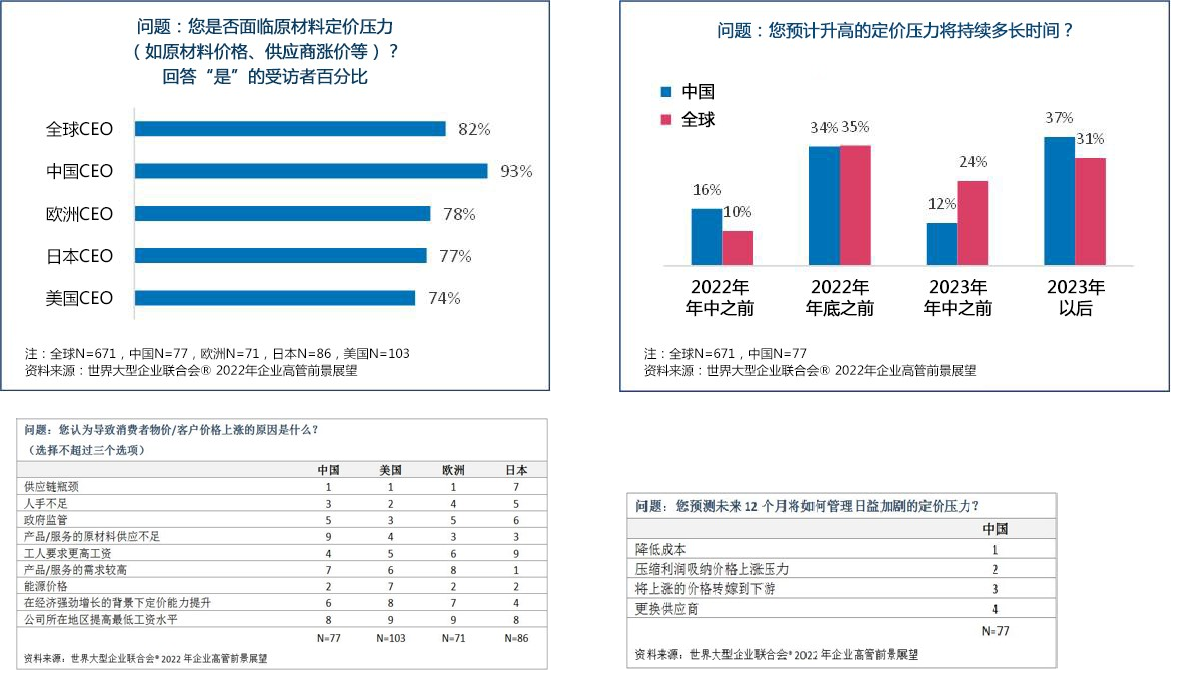

虽然中国公布的通胀率与其他国家相比相对较低,但中国CEO们早在乌克兰危机爆发之前,就已经在日益担忧物价和成本上涨问题。超过四分之一的中国CEO将高通胀列为2022年具有重大影响的问题,比去年增加了一倍。约93%的中国CEO们表示,公司的投入,包括原材料和工资,都面临价格上涨的压力,并且他们认为这一趋势在短时间内不会改变。约一半的CEO认为价格上涨压力将持续到2023年年中甚至更长时间,而这还是他们在乌克兰危机爆发之前的观点。他们认为物价上涨的主要原因是供应链瓶颈和飙升的能源价格。

CEO们对通货膨胀的担忧并非杞人忧天。世界大型企业联合会预计,中国的消费物价上涨速度目前较低,但未来几个月将会加速。乌克兰危机导致全球能源价格上涨,影响了中国玉米、小麦和化肥等农作物的进口。这些因素显著增加了中国的通胀压力。中国将很难维持目前确定的2022年3%的整体CPI目标(代表CPI适度上涨)。消费物价上涨以及收入增长放缓、疫情防控限制措施和就业创造速度放慢,将影响2022年的家庭支出增长,并拖累整体经济增长。有趣的是,相比其他国家的CEO,有更多的中国CEO表示愿意承受价格上涨的压力。

工作方式将被重新定义:远程办公日益普及

中国CEO们表示人力资源面临的主要挑战是如何打造一支更有韧性的团队,建立更具创新力的文化,培养更灵活的团队。

在疫情停工期间,远程办公对许多公司至关重要,这种办公形式将在全世界继续存在下去。在中国也不例外,但远程办公在中国的普及程度相对较低。全球有三分之一的CEO预测,疫情结束之后,至少40%的员工将远程办公,相比疫情之前的17%大幅增加。虽然中国CEO预测员工远程办公的比例较低,但他们依旧认为中国的工作方式将发生显著变化。只有17%的中国CEO表示,计划在疫情结束一年后,至少40%的员工将远程办公(美国的比例为53%)。这比疫情之前的11%有所提高,但远低于疫情期间的33%。尽管后疫情时代中国远程办公的员工绝对数相对较低,但在疫情之前远程办公的员工占11%至20%的公司有15%,到疫情之后将增加到33%,增加了超过一倍。公司对远程办公的认可,对员工的工作效率有重要影响,并将影响公司的招聘方式、领导模式和如何培养混合工作场所文化。优秀人才们现在可以合理期望自己有机会在喜欢的时间和地点办公,如果他们的要求被拒绝,就能够准备跳槽到其他公司。一个被越来越多人接受的现实是,在知识经济时代,工作应该与地点脱钩,员工不需要在指定的地点办公。人们可以在任何地点办公,在零工经济中,人们还能够选择办公时间。大多数行业将不再受物理空间的限制。

约42%的中国CEO认为远程办公只是权宜之计,从长远来看难以持续执行,这在全球CEO中比例最高。无论接受短期还是长期混合办公模式,都将给企业带来巨大挑战:超过一半的中国CEO认为,混合办公模式将增加人才竞争,给传统人力资源模式带来更多压力,而且他们认为这种模式会增加完成项目需要的时间。中国CEO还担心混合办公模式会降低员工的工作效率和内部人际关系的质量,削弱企业文化的优势,降低培养工作技能的效率。积极的一面是:有接近一半的中国CEO预计混合办公模式会促进创新和外部协作。

落实混合办公并不容易。超过四分之三的中国CEO表示,高效的混合办公模式需要大幅修改企业文化,提高内部沟通效率,团队领导者和企业高管必须学习新的管理技能,还需要重新设计薪酬结构。这都需要企业在执行混合办公模式时,要有战略眼光。企业领导者需要明确并果断决定多少人可以远程办公,哪些工作岗位适合远程办公,如何管理混合办公模式,如何确定员工薪酬,以及员工能够在哪些地点办公等。

环境、社会与治理问题的重点

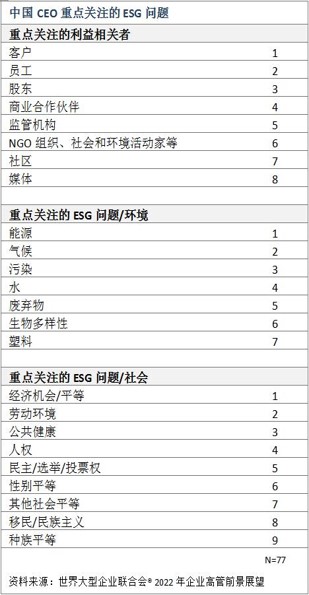

中国CEO们将提高可持续性列为2022年最紧迫的第二大内部问题。为了实现这个目标,企业必须更加重视环境、社会与治理(ESG)问题。我们的调查发现,企业最关注的环境问题是能源和气候变化,最关注的社会问题是改善经济发展机会、公平和劳动环境,均符合政府提出的“共同富裕”的目标。

对下一次危机准备不足

我们很难预测明年可能会发生哪些新的危机。但企业通过富有远见的预测和投资,可以减少风险,并通过超前部署减轻影响,从而避免遭到严重破坏。中国和全球的CEO们普遍承认对未来的冲击准备不足,让人们对许多企业的韧性产生疑问。许多企业的气候变化、网络安全和业务连续性策略尚未成形。

有哪些企业做好了准备?

• 欧洲65%的CEO和美国55%的CEO表示其所在企业做好了应对未来疫情相关危机的充分或非常充分的准备,而中国和日本的CEO的比例分别只有28%和27%。

• 大多数美国和欧洲的CEO(分别为53%和54%)还表示,他们做好了迎接金融动荡相关危机的妥善准备,而相比之下,中国和日本的CEO的比例分别只有32%和24%。

• 全球不到40%的CEO表示,面对通货膨胀、网络安全、自然灾害、供应链中断和气候变化等未来危机可能带来的各种挑战,其所在企业已经做好了充分准备。中国CEO的比例更低:

通货膨胀33%

网络安全29%

自然灾害22%

供应链中断29%

气候变化21%

社会动荡19%

• 虽然中国企业相对而言准备不足,但中国CEO们仅将更新危机应急计划排在2022年内部工作重点的第14位(共24个选项)。

未来的重重挑战

在中国和全球许多CEO所经营的企业内,包括高管在内的所有人从未经历过如此严重的地缘政治动荡或通货膨胀。在这种动荡的环境下,保持灵活性将是公司继续繁荣发展的关键。在之前的高管挑战调查中,CEO们认为一家灵活企业的关键品质包括:高效敬业的改革领导者;有韧性、能够适应变化的员工;开放透明、鼓励畅所欲言的文化;在所有组织层面持续进行透明地沟通;有效利用大数据分析指导决策。如今,企业需要重整旗鼓,并重新构想如何在动荡不安的全球环境下保持繁荣发展,因此这些品质变得更加重要。问题是CEO和他们的企业能否完成这项任务?(财富中文网)

(编者注:本文基于世界大型企业联合会2021年10月和11月在全球开展的《企业高管前景展望调查》的结果以及调查报告《2022年企业高管前景展望:重整旗鼓与重新构想》。欢迎登陆www.conference-board.org查看和下载完整报告。世界大型企业联合会是一家全球性的会员制独立智库,致力于在开展公益的同时,对未来发展趋势提供值得信任的洞察。)

安克·施拉德现任世界大型企业联合会亚洲研究总监,负责亚洲地区的研究项目。她还负责亚洲可持续性、ESG、公民责任和可持续发展研究与企业参与。安克毕业于德国康斯坦茨大学,取得公共政策与管理硕士学位。

查尔斯·米切尔现任世界大型企业联合会内容质量执行董事,负责保证该机构研究项目的客观性、独立性、准确性和商业相关性。他近几年在亚太地区投入大量时间,与我们的理事会合作开发针对亚太地区的内容。米切尔曾出版数本探讨国际商业文化、风俗习惯和商业礼仪的书籍,取得了美国宾夕法尼亚大学经济学学士学位。

翻译:刘进龙

审校:汪皓

是什么让中国CEO们彻夜难眠?

新冠疫情已经进入了第三个年头,显然它是一场马拉松,而不是一次短跑比赛。在中国,疫情的负面后果仍然在持续给中国的经济和营商环境带来压力。

据世界大型企业联合会(The Conference Board)的年度企业高管前景展望调查显示,早在乌克兰危机之前,经济衰退风险、消费者行为变化、通胀加剧、全球政治动荡、全球贸易中断和利润缩水,是中国CEO们认为2022年影响最大的事件。每一个事件都与疫情的进展直接相关,需要公司紧急采取措施,包括经营模式转型、现金流管理、成本控制、供应链灵活性和旨在打造更有韧性、更灵活的团队的人力资源管理创新等。这都是中国CEO们认为急需执行的措施。俄乌冲突的影响将加剧中国企业面临的许多压力,使公司更迫切地需要采取措施减缓这些事件的影响。

然而,中国和全球的CEO们很少有人相信,面对从新疫情到通胀、气候变化和供应链中断等未来危机,他们的公司做好了充分准备。

影响最大的10个外部问题

中国人消费模式改变所带来的挑战:复杂的变化

新冠疫情改变了中国大多数地区消费者的购物行为,刺激了网络购物繁荣,给企业带来了挑战,迫使它们不得不转变经营模式,以跟上这种趋势。事实上,约40%的中国CEO将消费者行为改变列为公司在2022年面临的具有巨大影响的问题之一,这个比例是在美国和欧洲的CEO的两倍。但在中国,消费者行为的改变远比表面看起来更加复杂。

中国政府将电子商务视为未来经济增长的关键引擎,在疫情期间,电商业务繁荣发展,并且一直持续至今。新冠疫情使家庭消费模式从非必需品消费转变为食物等必需品消费。在疫情之前,城市家庭消费日益倾向于非必需品消费,而必需品消费的增长速度较慢;必需品消费在消费总额中的比例不断缩小。自疫情爆发以来,非必需品消费的增长速度显著下降。可支配收入增长放缓、相对疲软的劳动市场和为控制疫情执行的严格出行管制,正在抑制非必需品消费。2021年第4季度,线上零售额同比增长3.9%,远低于实现中国政府提出的2025年线上零售额增长目标需要达到的7%的年增长率。虽然今年1月和2月的数据令人振奋,但病例数增加和相关商业中断,将继续带来消费下行风险。

从商业的角度,针对消费者行为和态度的变化及其对业务的潜在影响,实时提供数据驱动的洞察极具挑战性。

导致通胀上升的原因及其持续时间:CEO们的观点

虽然中国公布的通胀率与其他国家相比相对较低,但中国CEO们早在乌克兰危机爆发之前,就已经在日益担忧物价和成本上涨问题。超过四分之一的中国CEO将高通胀列为2022年具有重大影响的问题,比去年增加了一倍。约93%的中国CEO们表示,公司的投入,包括原材料和工资,都面临价格上涨的压力,并且他们认为这一趋势在短时间内不会改变。约一半的CEO认为价格上涨压力将持续到2023年年中甚至更长时间,而这还是他们在乌克兰危机爆发之前的观点。他们认为物价上涨的主要原因是供应链瓶颈和飙升的能源价格。

CEO们对通货膨胀的担忧并非杞人忧天。世界大型企业联合会预计,中国的消费物价上涨速度目前较低,但未来几个月将会加速。乌克兰危机导致全球能源价格上涨,影响了中国玉米、小麦和化肥等农作物的进口。这些因素显著增加了中国的通胀压力。中国将很难维持目前确定的2022年3%的整体CPI目标(代表CPI适度上涨)。消费物价上涨以及收入增长放缓、疫情防控限制措施和就业创造速度放慢,将影响2022年的家庭支出增长,并拖累整体经济增长。有趣的是,相比其他国家的CEO,有更多的中国CEO表示愿意承受价格上涨的压力。

通胀示意图

工作方式将被重新定义:远程办公日益普及

中国CEO们表示人力资源面临的主要挑战是如何打造一支更有韧性的团队,建立更具创新力的文化,培养更灵活的团队。

在疫情停工期间,远程办公对许多公司至关重要,这种办公形式将在全世界继续存在下去。在中国也不例外,但远程办公在中国的普及程度相对较低。全球有三分之一的CEO预测,疫情结束之后,至少40%的员工将远程办公,相比疫情之前的17%大幅增加。虽然中国CEO预测员工远程办公的比例较低,但他们依旧认为中国的工作方式将发生显著变化。只有17%的中国CEO表示,计划在疫情结束一年后,至少40%的员工将远程办公(美国的比例为53%)。这比疫情之前的11%有所提高,但远低于疫情期间的33%。尽管后疫情时代中国远程办公的员工绝对数相对较低,但在疫情之前远程办公的员工占11%至20%的公司有15%,到疫情之后将增加到33%,增加了超过一倍。公司对远程办公的认可,对员工的工作效率有重要影响,并将影响公司的招聘方式、领导模式和如何培养混合工作场所文化。优秀人才们现在可以合理期望自己有机会在喜欢的时间和地点办公,如果他们的要求被拒绝,就能够准备跳槽到其他公司。一个被越来越多人接受的现实是,在知识经济时代,工作应该与地点脱钩,员工不需要在指定的地点办公。人们可以在任何地点办公,在零工经济中,人们还能够选择办公时间。大多数行业将不再受物理空间的限制。

中国疫情之前/期间/之后的远程办公百分比

约42%的中国CEO认为远程办公只是权宜之计,从长远来看难以持续执行,这在全球CEO中比例最高。无论接受短期还是长期混合办公模式,都将给企业带来巨大挑战:超过一半的中国CEO认为,混合办公模式将增加人才竞争,给传统人力资源模式带来更多压力,而且他们认为这种模式会增加完成项目需要的时间。中国CEO还担心混合办公模式会降低员工的工作效率和内部人际关系的质量,削弱企业文化的优势,降低培养工作技能的效率。积极的一面是:有接近一半的中国CEO预计混合办公模式会促进创新和外部协作。

落实混合办公并不容易。超过四分之三的中国CEO表示,高效的混合办公模式需要大幅修改企业文化,提高内部沟通效率,团队领导者和企业高管必须学习新的管理技能,还需要重新设计薪酬结构。这都需要企业在执行混合办公模式时,要有战略眼光。企业领导者需要明确并果断决定多少人可以远程办公,哪些工作岗位适合远程办公,如何管理混合办公模式,如何确定员工薪酬,以及员工能够在哪些地点办公等。

环境、社会与治理问题的重点

中国CEO们将提高可持续性列为2022年最紧迫的第二大内部问题。为了实现这个目标,企业必须更加重视环境、社会与治理(ESG)问题。我们的调查发现,企业最关注的环境问题是能源和气候变化,最关注的社会问题是改善经济发展机会、公平和劳动环境,均符合政府提出的“共同富裕”的目标。

ESG重点问题列表

对下一次危机准备不足

我们很难预测明年可能会发生哪些新的危机。但企业通过富有远见的预测和投资,可以减少风险,并通过超前部署减轻影响,从而避免遭到严重破坏。中国和全球的CEO们普遍承认对未来的冲击准备不足,让人们对许多企业的韧性产生疑问。许多企业的气候变化、网络安全和业务连续性策略尚未成形。

有哪些企业做好了准备?

• 欧洲65%的CEO和美国55%的CEO表示其所在企业做好了应对未来疫情相关危机的充分或非常充分的准备,而中国和日本的CEO的比例分别只有28%和27%。

• 大多数美国和欧洲的CEO(分别为53%和54%)还表示,他们做好了迎接金融动荡相关危机的妥善准备,而相比之下,中国和日本的CEO的比例分别只有32%和24%。

• 全球不到40%的CEO表示,面对通货膨胀、网络安全、自然灾害、供应链中断和气候变化等未来危机可能带来的各种挑战,其所在企业已经做好了充分准备。中国CEO的比例更低:

通货膨胀33%

网络安全29%

自然灾害22%

供应链中断29%

气候变化21%

社会动荡19%

• 虽然中国企业相对而言准备不足,但中国CEO们仅将更新危机应急计划排在2022年内部工作重点的第14位(共24个选项)。

未来的重重挑战

在中国和全球许多CEO所经营的企业内,包括高管在内的所有人从未经历过如此严重的地缘政治动荡或通货膨胀。在这种动荡的环境下,保持灵活性将是公司继续繁荣发展的关键。在之前的高管挑战调查中,CEO们认为一家灵活企业的关键品质包括:高效敬业的改革领导者;有韧性、能够适应变化的员工;开放透明、鼓励畅所欲言的文化;在所有组织层面持续进行透明地沟通;有效利用大数据分析指导决策。如今,企业需要重整旗鼓,并重新构想如何在动荡不安的全球环境下保持繁荣发展,因此这些品质变得更加重要。问题是CEO和他们的企业能否完成这项任务?(财富中文网)

(编者注:本文基于世界大型企业联合会2021年10月和11月在全球开展的《企业高管前景展望调查》的结果以及调查报告《2022年企业高管前景展望:重整旗鼓与重新构想》。欢迎登陆www.conference-board.org查看和下载完整报告。世界大型企业联合会是一家全球性的会员制独立智库,致力于在开展公益的同时,对未来发展趋势提供值得信任的洞察。)

安克·施拉德现任世界大型企业联合会亚洲研究总监,负责亚洲地区的研究项目。她还负责亚洲可持续性、ESG、公民责任和可持续发展研究与企业参与。安克毕业于德国康斯坦茨大学,取得公共政策与管理硕士学位。

查尔斯·米切尔现任世界大型企业联合会内容质量执行董事,负责保证该机构研究项目的客观性、独立性、准确性和商业相关性。他近几年在亚太地区投入大量时间,与我们的理事会合作开发针对亚太地区的内容。米切尔曾出版数本探讨国际商业文化、风俗习惯和商业礼仪的书籍,取得了美国宾夕法尼亚大学经济学学士学位。

翻译:刘进龙

审校:汪皓

What Is Keeping CEOs in China Up at Night?

Now in its third year, the COVID-19 pandemic is clearly a marathon, not a sprint. In China, the negative consequences of the pandemic continue to exert pressure on the Chinese economy and business environment.

Even before the Ukraine crisis, recession risk, changing consumer behaviors, rising inflation, global political instability, global trade disruptions, and margin compression were at the top of high-impact events in 2022 for CEOs in China according to The Conference Board’s annual C-Suite Outlook survey. Each is directly tied to the pandemic’s course and requires urgent action across business model transformation, cash flow management, cost containment, supply chain flexibility, and innovative human capital management aimed at building a more resilient and agile workforce. All of these are priority actions on the radar of CEOs in China. The fallout from the situation in Ukraine will make many of these stress points more intense and the actions to mitigate their impact more urgent.

However, few CEOs globally and in China believe their organizations are well prepared to deal with future crises from new pandemics to inflation to climate change and supply chain disruption.

The Challenge of Changing Chinese Consumption Patterns: A Complex Story

As in most places, the COVID pandemic has shifted Chinese consumer buying behaviors, producing a boom in online sales and challenging firms to modify their business models to keep up. Indeed, almost 40% of CEOs in China cite changes in consumer behavior as a significant high impact issue for their organizations in 2022 — double the number of CEOs in the US and Europe. But in China, the story of consumer behavior is more complex than it appears on the surface.

E-commerce, which the government considers to be a key engine of future growth, has boomed throughout the pandemic period in China — until recently. The COVID pandemic has shifted previous household spending patterns away from discretionary spending towards non-discretionary necessities like food. Before the pandemic, urban households were allocating a growing share of their spending to discretionary categories while spending on necessities grew at a much slower pace; its share in total consumption shrinking. Since the start of the pandemic, growth rates for discretionary spending categories have slowed down significantly. Slower disposable income growth, a relatively weak labor market, and strict mobility controls for COVID containment are holding back discretionary spending. Q4 2021 online retail sales growth was 3.9 percent year-over-year, substantially below the 7 percent annual growth needed to hit the government’s official 2025 online retail sales growth targets. January and February data surprised to the upside, but rising COVID cases and associated commercial disruptions will continue to pose downside risks for consumption.

From a business perspective, providing real-time data-driven insights on changing consumer behaviors and attitudes and their potential impact on the business is a critical challenge.

What’s Driving Inflation and How Long Will It Last: the CEO View

While reported inflation rates in China are relatively low compared to the rest of the world, there was growing concern among CEOs in China about rising prices and costs even before the Ukraine crisis. More than a quarter of China CEOs cite rising inflation as a high impact issue in our 2022 survey—more than double the percentage from just a year earlier. Some 93% of CEOs in China say they are facing upward pricing pressures for inputs, including raw materials and wages — and it’s not going away anytime soon in their view. Almost half believe this pressure will persist until mid-2023 and beyond—and that was before the Ukraine crisis. They see the main drivers as supply chain bottle necks and soaring energy prices.

CEO concerns about inflation are justified. The Conference Board expects the currently low inflation in consumer prices in China to climb in the coming months. The Ukraine crisis is causing a rise in global energy prices and disruptions to China’s imports of agricultural products such as corn, wheat, and fertilizer. All add significantly to inflationary pressure. The current headline CPI target of 3% (implying modest CPI growth) in 2022 will be challenging to maintain. Rising consumer price inflation, combined with slow income growth, COVID restrictions, and slow job creation, will weigh on household expenditure growth in 2022 and drag on growth. Interestingly, more CEOs in China say they are willing to absorb price increases than their colleagues globally.

How Work Will Get Redefined: Remote Work Expected to Grow

CEOs in China say that the main human resource challenges ahead are building a more resilient workforce, establishing a more innovative culture, and developing more agile teams.

Remote work, vital to many firms during pandemic-related shutdowns, is here to stay globally. So too for China, but to a lesser extent. A third of CEOs globally expect that at least 40% of employees will work remotely after the pandemic subsides compared to 17% prepandemic. While the percentages in China are smaller, they still signal a significant change within the local context. In China, just 17% of CEOs say they are planning for at least 40% of employees to be remote one year after the pandemic subsides (compared to 53% in the US). That number is up from just 11% pre-pandemic in China, but down from 33% during the pandemic. Despite a relatively low absolute number of remote employees in a post-pandemic China, the firms that had between 11% and 20% of employees working remotely before the pandemic will more than double from 15% to 33% post pandemic. This newfound embrace of remote work carries important implications for worker productivity and how organizations hire, lead, and foster a hybrid workplace culture. Talented people can now reasonably expect opportunities to work when and where they like—and may be prepared to seek employment elsewhere if these choices are denied to them. The growing reality is that, in the knowledge economy, work has been decoupled from location and employees no longer must be in a specific place to do a job. Talent can work from anywhere, and in the gig economy at any time. Physical space is no longer a constraint for most industries.

Some 42% of CEOs in China see remote work only as a temporary fix that is unsustainable in the long run— by the far the highest percentage of CEOs with this view globally. Embracing a hybrid work mode, either in the short-term or for the long haul presents significant challenges: more than half of China CEOs believe a hybrid model will increase the competition for talent putting added pressure on traditional HR practices and they believe projects will take longer to complete. Collectively, they fear that it will also decrease worker productivity, the quality of internal relationships, the strength of corporate culture, and the pace of skill building. On the positive side: just under half expect to see improvements in innovation and external collaboration.

Getting it right will take work. More than three-quarters of China CEOs say a high performing hybrid work model requires significant change in corporate culture, more effective internal communication, new management skills for team leaders and executives, and a rethink of total rewards structures. All of this requires a strategic approach to implementing hybrid work models. Business leaders need to be clear and decisive about how much remote work will be allowed and in what types of jobs, how hybrid work models will be managed, how workers will be compensated, and where workers can be located.

A Look at ESG Priorities

CEOs in China cite becoming more sustainable as their second highest internal priority for 2022. Achieving this will require greater focus on environmental, social, and governance (ESG) issues. According to our survey their top environmental priorities are energy and climate change, and their top social issues are improving economic opportunity, equality and labor conditions – all in line with the government’s “Common Prosperity” campaign.

Shocking Lack of Preparedness for the Next Crisis

What new crises may emerge in the coming year is impossible to predict. But with some foresight and investment, crippling disruptions can be prevented by reducing risk exposures and taking preemptive measures to mitigate their impacts. The generally admitted lack of preparedness for future shocks among CEOs both in China and globally raises questions about the resilience of many organizations. For many, climate change, cyber security and business continuity strategies remain formative.

Who is ready for what?

• A total of 65% of CEOs in Europe and 55% in the U.S. say their organizations are well or very well prepared to handle a future pandemic-related crisis, compared to just 28% in China and 27% in Japan.

• A majority of US and European CEOs (53% and 54% respectively) also say they are well prepared to meet a crisis related to financial instability compared to just 32% in China and 24% in Japan.

• Globally less than 40% of CEOs say their organizations are well prepared to meet challenges posed by future crisis related to inflation, cybersecurity, natural disasters, supply chain disruptions, and climate change. The numbers are worse for China:

inflation 33%

cybersecurity 29%

natural disasters 22%

supply chain disruptions 29%

climate change 21%

civil unrest 19%

• Despite this relative lack of preparedness, update crises contingency plans ranks just 14th (out of 24 choices) as an internal focus for CEOs in China in 2022.

So Many Challenges Ahead

Many CEOs in China and globally are running organizations where their workforce, including key C-suite executives, have never experienced such elevated levels of geopolitical instability or such inflationary conditions. Agility will be a critical factor to thrive in such a turbulent environment. In our previous C-Suite Challenge surveys, CEOs identified the critical traits that make an agile organization as: effective and engaged change leaders; resilient employees/individuals that adapt to change; an open and transparent speak-up culture; communicating consistently and transparently at all organizational level and effective use of big data analytics to inform decision making. All of these traits are now more essential than ever as organizations reset and reimagine to thrive in the unquietly turbulent global environment ahead. The question is: are CEOs and their organizations up to the task?

(Editor’s Note: This article is based on the findings of The Conference Board C-Suite Outlook Survey which was fielded globally in October and November of 2021 and reported in “C-Suite Outlook 2022: Reset and Reimagine”. Please visit www.conference-board.org to learn more and to download the full report. The Conference Board is a global, independent member-driven think tank that delivers trusted insights for what’s ahead while working in the public interest.

Anke Schrader, Research Director, The Conference Board Asia, oversees research programs for the Asia region. She also leads research and corporate engagement on sustainability, ESG, citizenship, and sustainable development for Asia. Anke graduated from the University of Konstanz, Germany with a master’s degree in Public Policy and Management.

Charles Mitchell, the Executive Director, Content Quality at The Conference Board, is responsible for ensuring the objectivity, independence, accuracy, and business relevance of the organization’s research. In recent years he has spent considerable time in Asia-Pacific, working with our Councils to develop region-specific content. He is the author of several books dealing with international business cultures, customs, and etiquette and holds a bachelor’s degree in economics from the University of Pennsylvania in the US.

请打开财富Plus APP