现在多少美国人能马上拿出1000美元?

MEGAN LEONHARDT

2022-01-29

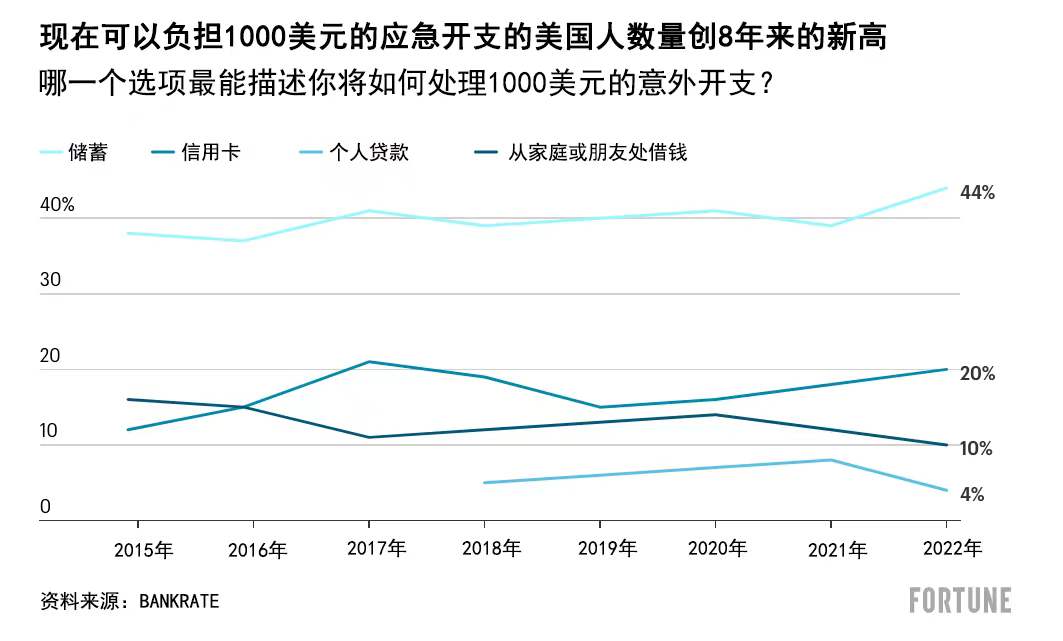

约44%的人表示,他们可以在不使用信用卡或借钱的情况下拿出1000美元应急开支。

文本设置

文本设置

Plus(0条)

Plus(0条)

更多的美国人现在能够负担1000美元的应急开支,但对于大多数美国家庭来说,这一目标仍然遥不可及。

根据消费金融服务公司Bankrate在1月19日发布的一份针对1000多名美国成年人的调查,约44%的人表示,他们可以在不使用信用卡或借钱的情况下负担这一水平的应急开支。

这是Bankrate开展这项调查的8年来,自称有能力处理意外账单的美国人所占比例最高的一次,甚至超过2020年和2021年,刺激支票、失业津贴和儿童税收抵免付款等一系列联邦资助相继到账时的水平。

美国人支付1000美元应急开支的能力有所增强,可能是拜以下几个因素所赐:来自2021年联邦资助项目的剩余储蓄、美国经济反弹,以及失业率下降。Bankrate的首席金融分析师格雷格·麦克布莱德对《财富》杂志表示,人们正在重返工作岗位,工资也在持续上涨。

但并不全是经济因素在发挥作用。这场新冠疫情改变了美国人对储蓄的重视程度,尤其是考虑到2020年的高失业率。“新冠疫情也凸显了应急储蓄的重要性。因此,人们更加专注地重建他们在疫情期间失去的东西,就连那些此前没有储蓄的人也开始攒钱了。”他说。

并非每个人的储蓄都足以缓冲意外开支

尽管更多的美国人能够用自己的储蓄来应对重大的计划外支出,但仍然有超过三分之一的人需要借钱。约35%的受访者表示,他们将不得不通过信用卡、个人贷款或从亲朋好友那里借钱来支付这笔费用。

在所有的年龄段中,26岁至32岁的千禧一代是最有可能用信用卡支付1000美元意外支出的。麦克布莱德指出,在新冠疫情期间,年轻工人备受收入中断和失业的冲击。他们开始积累储蓄的时间也比年长的工人更短。

然而,即使对更年长的美国人而言,目前的储蓄缓冲也不太可能持续下去,因为高通胀让人们更加难以存钱。麦克布莱德告诉《财富》杂志:“对于我们能否在未来12个月复制过去12个月的成功,我并没有那么乐观。”

大多数美国人也不太可能像新冠疫情早期那样,继续享受远程工作带来的好处——新冠疫情早期阶段的封锁措施,大幅减少了人们在交通和餐饮方面的支出。在许多情况下,这意味着美国人有了更多的预算资金,从而更容易增加储蓄。

“我们原以为这场疫情是短期的,所以人们没有消费,而是把更多的钱存下来。”麦克布莱德说,“两年过去了,很多家庭正在把没有花在旅游、外出就餐或去听音乐会上的钱花在其他地方,比如家居装修,购买其他必需品,而这方面的成本正在增长。”

美国经济分析局(Bureau of Economic Analysis)的最新数据显示,自2020年4月达到33.8%的历史高点以来,美国的个人储蓄占其可支配收入的比例已经大幅下降,在2021年11月降至6.9%。

半数美国人表示,通货膨胀正在侵蚀其储蓄能力

专家建议,通常情况下,大多数美国人最好存下三到六个月的生活费。

尽管一些美国人或许有一笔充足的应急储蓄,但事实可能会证明,一旦被花掉,再存下这样一笔钱就更难了。这是因为通货膨胀开始侵蚀储蓄率。

在Bankrate的调查报告中,约49%的受访者表示,通货膨胀导致他们的储蓄减少,三分之一的人表示没有受到影响。约2%的受访者坦言,他们一开始就没有能力储蓄。

“通货膨胀正在使家庭预算变得越来越紧张。”麦克布莱德说。

“这次通胀的涉及面非常广泛。”他补充说,通胀对食品和房租等非自由裁量支出的影响很大。2021年12月的消费者价格指数(Consumer Price Index)显示,在过去12个月,食品价格上涨了6.5%,租金上涨约3.3%。

麦克布莱德表示,只有到家庭收入的增长跑赢通胀,并且通胀确实回落的时候,家庭储蓄或许才会真正取得进展。但这很难预测;许多专家认为,高通胀将持续到2022年年底。

如何在通胀飙升的情况下存钱

对于那些想存钱的人,麦克布莱德建议利用商家的忠诚计划,充分利用折扣、优惠券和返利来降低日常开支。甚至用完信用卡公司提供的现金回馈,或者收藏起来的礼品卡,也是有所助益的。

麦克布莱德指出,有可能的话,现在或许是专注于增加收入的好机会。要求加薪,或者找一份新工作。精力够的话,不妨找一份兼职,做一些零工,哪怕只是做很短时间。

“劳动力市场目前有数百万个空缺职位,你可以充分利用这一点。这能够给你留出时间来重建应急储蓄,或者一劳永逸地还清信用卡债务。”他说。

然而,最好的存钱方式仍然是将薪水直接存入一个专门的储蓄账户。“这可以确保你存一点钱,并且迫使你围绕实得工资制定预算。”但他随即指出,考虑到生活成本持续攀升,很多人或许很难做到这一点。

“今时不同往日,你不能等到月底时,看看还剩下多少再试着存一点钱了。”麦克布莱德说,“在生活成本持续攀升的当下,根本就没有‘余粮’可言。即使有,也是缺乏稳定性的。”(财富中文网)

译者:任文科

更多的美国人现在能够负担1000美元的应急开支,但对于大多数美国家庭来说,这一目标仍然遥不可及。

根据消费金融服务公司Bankrate在1月19日发布的一份针对1000多名美国成年人的调查,约44%的人表示,他们可以在不使用信用卡或借钱的情况下负担这一水平的应急开支。

这是Bankrate开展这项调查的8年来,自称有能力处理意外账单的美国人所占比例最高的一次,甚至超过2020年和2021年,刺激支票、失业津贴和儿童税收抵免付款等一系列联邦资助相继到账时的水平。

美国人支付1000美元应急开支的能力有所增强,可能是拜以下几个因素所赐:来自2021年联邦资助项目的剩余储蓄、美国经济反弹,以及失业率下降。Bankrate的首席金融分析师格雷格·麦克布莱德对《财富》杂志表示,人们正在重返工作岗位,工资也在持续上涨。

但并不全是经济因素在发挥作用。这场新冠疫情改变了美国人对储蓄的重视程度,尤其是考虑到2020年的高失业率。“新冠疫情也凸显了应急储蓄的重要性。因此,人们更加专注地重建他们在疫情期间失去的东西,就连那些此前没有储蓄的人也开始攒钱了。”他说。

并非每个人的储蓄都足以缓冲意外开支

尽管更多的美国人能够用自己的储蓄来应对重大的计划外支出,但仍然有超过三分之一的人需要借钱。约35%的受访者表示,他们将不得不通过信用卡、个人贷款或从亲朋好友那里借钱来支付这笔费用。

在所有的年龄段中,26岁至32岁的千禧一代是最有可能用信用卡支付1000美元意外支出的。麦克布莱德指出,在新冠疫情期间,年轻工人备受收入中断和失业的冲击。他们开始积累储蓄的时间也比年长的工人更短。

然而,即使对更年长的美国人而言,目前的储蓄缓冲也不太可能持续下去,因为高通胀让人们更加难以存钱。麦克布莱德告诉《财富》杂志:“对于我们能否在未来12个月复制过去12个月的成功,我并没有那么乐观。”

大多数美国人也不太可能像新冠疫情早期那样,继续享受远程工作带来的好处——新冠疫情早期阶段的封锁措施,大幅减少了人们在交通和餐饮方面的支出。在许多情况下,这意味着美国人有了更多的预算资金,从而更容易增加储蓄。

“我们原以为这场疫情是短期的,所以人们没有消费,而是把更多的钱存下来。”麦克布莱德说,“两年过去了,很多家庭正在把没有花在旅游、外出就餐或去听音乐会上的钱花在其他地方,比如家居装修,购买其他必需品,而这方面的成本正在增长。”

美国经济分析局(Bureau of Economic Analysis)的最新数据显示,自2020年4月达到33.8%的历史高点以来,美国的个人储蓄占其可支配收入的比例已经大幅下降,在2021年11月降至6.9%。

半数美国人表示,通货膨胀正在侵蚀其储蓄能力

专家建议,通常情况下,大多数美国人最好存下三到六个月的生活费。

尽管一些美国人或许有一笔充足的应急储蓄,但事实可能会证明,一旦被花掉,再存下这样一笔钱就更难了。这是因为通货膨胀开始侵蚀储蓄率。

在Bankrate的调查报告中,约49%的受访者表示,通货膨胀导致他们的储蓄减少,三分之一的人表示没有受到影响。约2%的受访者坦言,他们一开始就没有能力储蓄。

“通货膨胀正在使家庭预算变得越来越紧张。”麦克布莱德说。

“这次通胀的涉及面非常广泛。”他补充说,通胀对食品和房租等非自由裁量支出的影响很大。2021年12月的消费者价格指数(Consumer Price Index)显示,在过去12个月,食品价格上涨了6.5%,租金上涨约3.3%。

麦克布莱德表示,只有到家庭收入的增长跑赢通胀,并且通胀确实回落的时候,家庭储蓄或许才会真正取得进展。但这很难预测;许多专家认为,高通胀将持续到2022年年底。

如何在通胀飙升的情况下存钱

对于那些想存钱的人,麦克布莱德建议利用商家的忠诚计划,充分利用折扣、优惠券和返利来降低日常开支。甚至用完信用卡公司提供的现金回馈,或者收藏起来的礼品卡,也是有所助益的。

麦克布莱德指出,有可能的话,现在或许是专注于增加收入的好机会。要求加薪,或者找一份新工作。精力够的话,不妨找一份兼职,做一些零工,哪怕只是做很短时间。

“劳动力市场目前有数百万个空缺职位,你可以充分利用这一点。这能够给你留出时间来重建应急储蓄,或者一劳永逸地还清信用卡债务。”他说。

然而,最好的存钱方式仍然是将薪水直接存入一个专门的储蓄账户。“这可以确保你存一点钱,并且迫使你围绕实得工资制定预算。”但他随即指出,考虑到生活成本持续攀升,很多人或许很难做到这一点。

“今时不同往日,你不能等到月底时,看看还剩下多少再试着存一点钱了。”麦克布莱德说,“在生活成本持续攀升的当下,根本就没有‘余粮’可言。即使有,也是缺乏稳定性的。”(财富中文网)

译者:任文科

More Americans can now afford a $1,000 emergency expense, but that goal still remains out of reach to the majority of U.S. households.

Around 44% of people in the U.S. say they would be able to cover that level of emergency expense without putting it on a credit card or borrowing money, according to a survey released on January 19 by Bankrate of just over 1,000 U.S. adults.

That’s the highest proportion of Americans who said they could handle unexpected bills in the eight years that Bankrate has been conducting the survey, topping even 2020 and 2021 levels when federal programs like stimulus checks, enhanced unemployment benefits and child tax credit payments were in place.

The increased ability to cover that $1,000 expense could be due to a few things: remaining savings from federal programs from last year, a rebounding U.S. economy, and a fall in unemployment. People are getting back to work and wage growth has been on the rise, Greg McBride, chief financial analyst for Bankrate, tells Fortune.

But it’s not all economic factors at play. The pandemic changed Americans’ priorities around saving, especially in light of the high unemployment seen in 2020. “The pandemic also underscored the importance of emergency savings, so there's a greater focus on rebuilding what was lost during the pandemic, but also accumulating savings for those that previously hadn't done so,” he says.

Not everyone has a robust savings cushion

Despite a higher number of Americans able to pay for a major unplanned expense using their savings, more than a third would still have to borrow the money. About 35% of those surveyed said they’d have to finance the expense using a credit card, personal loan, or by taking money from family and friends.

Younger millennials, ages 26 to 32, were the most likely of all age groups to finance an unplanned $1,000 expense with a credit card. Younger workers were predominantly hit by income disruptions and joblessness during the pandemic, McBride says. They’ve also had less time than older workers to even begin to build up their savings.

Even among older Americans, however, the current savings cushion is unlikely to last because high inflation is making it harder to save. “I'm not as optimistic that we're going to replicate the success of the last 12 months over the next 12 months,” McBride tells Fortune.

It’s also unlikely that most Americans are still reaping the rewards of working remotely like they were when lockdowns were in place during the early days of the pandemic, which led to less spending on transportation costs and restaurants. In many cases, this meant Americans had more money in their budgets and found it easier to put more away in savings.

“We were expecting [the pandemic] to be short term, so people weren't spending, they were saving more,” McBride says. “Two years in, for a lot of households, the money that doesn't get spent on travel, dining out or going to a concert is just getting spent someplace else—whether it’s on home improvements, or just other necessities that are increasing in cost.”

Americans’ personal saving rates as a percentage of their disposable personal income have already dropped since the all-time high of 33.8% in April 2020, hitting 6.9% in November, according to the latest data available from the Bureau of Economic Analysis.

Half of Americans say inflation is eating into their ability to save

Typically experts recommend most Americans have between three to six months of living expenses saved up.

And while some Americans may have a fully-funded emergency savings cushion, it may now prove harder to build it back up once it’s been spent. That’s because inflation is starting to eat into savings rates.

About 49% of those surveyed by Bankrate report that inflation is causing them to save less, while a third say it’s having no impact. About 2% of respondents say they were never able to save to begin with.

“Inflation is stretching the household budget further and further,” McBride says.

“This inflation is very broad based,” he adds, saying that it’s affecting non-discretionary spending such as food and rent in big ways. Grocery food prices rose 6.5% over the last 12 months while rents increased by about 3.3%, according to the December Consumer Price Index.

If household income growth outpaces inflation—and if inflation does come back down, McBride says maybe then households could truly make headway with their savings. But that’s difficult to predict and many experts are predicting that high inflation will stick around through 2022.

How to save with soaring inflation

For those who are looking to save, McBride recommends utilizing loyalty programs and taking full advantage of discounts, coupons and rebates to help keep spending costs down. Even using up your cash back rewards or that stash of gift cards tucked away helps.

If possible, McBride says now might be a good opportunity to focus on increasing your income. Ask for raise or perhaps seek out a new job. Or, if you've got the bandwidth to take on a second job, do some gig work even just for a brief period of time.

“You can capitalize on this labor market where there are millions of open unfilled jobs and that can give you this window of time to rebuild your emergency savings or pay off that credit card debt once and for all,” he says.

The best step toward building savings, however, is still to set up a direct deposit from your paycheck into a dedicated savings account. “It makes sure that the savings happens—it forces you to build a budget around your take home pay,” he says, but adds that may be difficult for many in light of rising costs.

“Now more than ever, you can't try to save by waiting until the end of the month to see what's left over,” McBride says. “At a time when costs are going up the way they are, there just isn't money left over. And even when there is, there's no consistency to that.”

请打开财富Plus APP