美国楼市即将崩溃?为时尚早

Lance Lambert

2021-09-06

目前已经有越来越多的悲观主义者指出,美国的房地产泡沫又到了快要被戳破的时候。

文本设置

文本设置

Plus(0条)

Plus(0条)

美国疫情带火了房地产市场,自从去年美国新冠疫情爆发以来,美国的中位房价已经创纪录地上涨了24%。但最近几周,购房者开始面对飙升的房价望而却步,美国的这一波房市有了冷却的势头。简而言之,美国房地产市场正在放缓。

目前已经有越来越多的悲观主义者指出,美国的房地产泡沫又到了快要被戳破的时候。在他们看来,美国近期房价的上涨速度太快了,现在必然面临回落。知名投资人彼得·布克瓦上周在接受美国消费者新闻与商业频道(CNBC)采访时说:“我为那些在过去一年里买房的人感到难过,因为他们就是在房价高位接盘的人。”

那么,数据怎么说?如果你深入研究的话,你就会发现,2008年的房地产泡沫,和2021年的房地产牛市是截然不同的。有几个原因可以解释为什么美国房市不会马上崩盘,其中有一个原因尤其重要。

在回答这个问题之前,让我们先看看上次房市的崩盘。

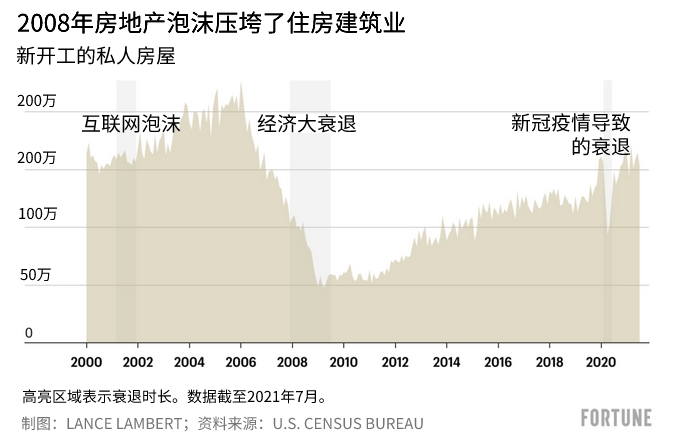

在金融危机爆发之前的那几年,美国房地产市场陷入了彻底的疯狂。为了捞钱,房地产商开始了疯狂的建设。因此,一旦房地产市场在2006年开始放缓,新建设项目的过剩就会迅速对房价施加负面压力。加上大量购房者因为断贷而被收房,房市供大于求的局面愈发突出。美国花了很多年才消化了这些过剩的房源。

那么2021年的情况又是如何呢?简而言之,大不相同,甚至截然相反。在2008年经济危机中劫后余生的房地产商们近几年可以说是极其保守的。在经济危机之前的8年里,美国平均每月开工170万套住房。而从2013年到2021年,美国平均每月只开工了120万套住房。看出来问题了吗?近几年美国房地产开工的速度还赶不上人口的增长速度。根据房地美(Freddie Mac)的数据,美国目前的住宅缺口大约达到了380万套。

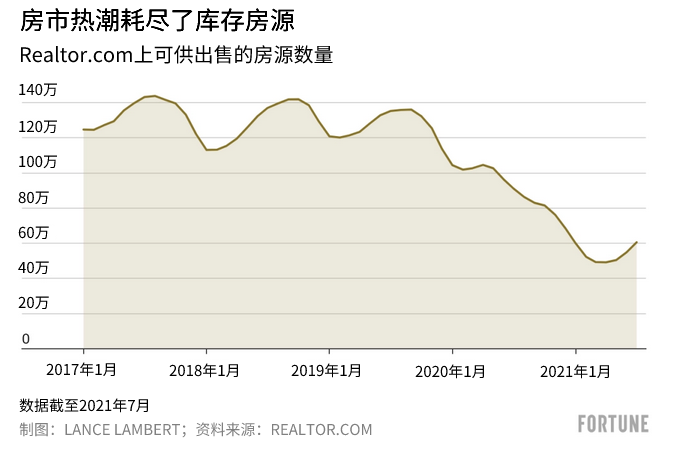

一方面是房地产的开工率不高,另一方面是需求的强劲,这就是为什么哪怕在新冠疫情之前,美国的房地产库存(即待售的房屋数量)就在下降的原因。而在新冠疫情期间,大量买家涌入市场,让库存房源变得更加抢手。从2020年4月至2021年4月,美国的房地产库存下降了50%以上。尽管此后有所回升,但仍然接近近40年来的最低水平。

以上我们用了一些篇幅,说明短期之内美国为什么不太可能出现房源供给过剩的问题。这也是为什么房地产市场不太可能崩盘的首要原因。当然,虽然目前不存在供给过剩的问题,但房价增长放缓甚至下跌的可能性都是有的——不过但凡不出现供给过剩的问题,就不太可能出现2008年的那种大崩盘。

据房地产研究公司CoreLogic预测,未来12个月,美国房价的平均增幅将仅为3.2%。假设该公司的预测是错的,房价不光没有涨,反而下降了一点点。在这种情况下,那些今年反复看房又没有买到房的买家很可能会迅速重返市场。同时,房价下降也会阻止供给的进一步提高。

房地产市场研究公司Zonda的首席经济学家阿里·沃尔夫在接受《财富》杂志采访时称:“消费者已经看到了房价上涨的幅度和速度,他们不愿意在今天的房价水平上买房。一旦房地产市场出现松动,这些购房者将扮演重要的角色。如果其中一些人在市场放缓时入市,那么他们就将决定市场下行的底线。目前持观望态度的这些消费者,实际上能够帮助房市延长这一轮生命周期。”

尽管房地产市场最近有所降温,但是市场仍然有很大的回旋空间。正如《财富》杂志之前报道的那样,最近五年,美国“千禧一代”中人数最多的一批人,也就是1989年至1993年出生的这批年轻人,将集体步入而立之年——这也是大多数人真正开始考虑买房的年纪。

美国房地产不会崩的另一个原因是,如果考虑收入水平的话,美国现在的住房成本实际上要低于2008年前。在经济危机前,美国有7.2%的个人收入被用来偿还按揭贷款,而现在这个数字仅为3.4%。另外,“房奴”们还应该感谢新冠疫情——疫情刺激了美国的低利率政策,也导致了抵押贷款和PMI(私人抵押贷款保险)的降低。

不过,目前美国房地产市场仍然有两大不确定性因素。首先,如果美联储(Federal Reserve)由于担心通胀影响而选择提前加息,这将对房市产生立竿见影的负面影响。第二个风险到是今年9月底,抵押贷款延期计划即将结束。目前仍然有170多万人按照该计划可以缓交贷款。当然,如果到时候其中的一部分人出现了断供的情况,而且选择了卖房而非续供,那么这有可能会导致库存房源数量的上升。但即便如此,也不太可能造成供应过剩:Home.LLC公司为《财富》杂志所做的一项分析显示,抵押贷款延期计划的结束,只会导致房源库存暂时性增加11%。(财富中文网)

译者:朴成奎

美国疫情带火了房地产市场,自从去年美国新冠疫情爆发以来,美国的中位房价已经创纪录地上涨了24%。但最近几周,购房者开始面对飙升的房价望而却步,美国的这一波房市有了冷却的势头。简而言之,美国房地产市场正在放缓。

目前已经有越来越多的悲观主义者指出,美国的房地产泡沫又到了快要被戳破的时候。在他们看来,美国近期房价的上涨速度太快了,现在必然面临回落。知名投资人彼得·布克瓦上周在接受美国消费者新闻与商业频道(CNBC)采访时说:“我为那些在过去一年里买房的人感到难过,因为他们就是在房价高位接盘的人。”

那么,数据怎么说?如果你深入研究的话,你就会发现,2008年的房地产泡沫,和2021年的房地产牛市是截然不同的。有几个原因可以解释为什么美国房市不会马上崩盘,其中有一个原因尤其重要。

在回答这个问题之前,让我们先看看上次房市的崩盘。

在金融危机爆发之前的那几年,美国房地产市场陷入了彻底的疯狂。为了捞钱,房地产商开始了疯狂的建设。因此,一旦房地产市场在2006年开始放缓,新建设项目的过剩就会迅速对房价施加负面压力。加上大量购房者因为断贷而被收房,房市供大于求的局面愈发突出。美国花了很多年才消化了这些过剩的房源。

那么2021年的情况又是如何呢?简而言之,大不相同,甚至截然相反。在2008年经济危机中劫后余生的房地产商们近几年可以说是极其保守的。在经济危机之前的8年里,美国平均每月开工170万套住房。而从2013年到2021年,美国平均每月只开工了120万套住房。看出来问题了吗?近几年美国房地产开工的速度还赶不上人口的增长速度。根据房地美(Freddie Mac)的数据,美国目前的住宅缺口大约达到了380万套。

一方面是房地产的开工率不高,另一方面是需求的强劲,这就是为什么哪怕在新冠疫情之前,美国的房地产库存(即待售的房屋数量)就在下降的原因。而在新冠疫情期间,大量买家涌入市场,让库存房源变得更加抢手。从2020年4月至2021年4月,美国的房地产库存下降了50%以上。尽管此后有所回升,但仍然接近近40年来的最低水平。

以上我们用了一些篇幅,说明短期之内美国为什么不太可能出现房源供给过剩的问题。这也是为什么房地产市场不太可能崩盘的首要原因。当然,虽然目前不存在供给过剩的问题,但房价增长放缓甚至下跌的可能性都是有的——不过但凡不出现供给过剩的问题,就不太可能出现2008年的那种大崩盘。

据房地产研究公司CoreLogic预测,未来12个月,美国房价的平均增幅将仅为3.2%。假设该公司的预测是错的,房价不光没有涨,反而下降了一点点。在这种情况下,那些今年反复看房又没有买到房的买家很可能会迅速重返市场。同时,房价下降也会阻止供给的进一步提高。

房地产市场研究公司Zonda的首席经济学家阿里·沃尔夫在接受《财富》杂志采访时称:“消费者已经看到了房价上涨的幅度和速度,他们不愿意在今天的房价水平上买房。一旦房地产市场出现松动,这些购房者将扮演重要的角色。如果其中一些人在市场放缓时入市,那么他们就将决定市场下行的底线。目前持观望态度的这些消费者,实际上能够帮助房市延长这一轮生命周期。”

尽管房地产市场最近有所降温,但是市场仍然有很大的回旋空间。正如《财富》杂志之前报道的那样,最近五年,美国“千禧一代”中人数最多的一批人,也就是1989年至1993年出生的这批年轻人,将集体步入而立之年——这也是大多数人真正开始考虑买房的年纪。

美国房地产不会崩的另一个原因是,如果考虑收入水平的话,美国现在的住房成本实际上要低于2008年前。在经济危机前,美国有7.2%的个人收入被用来偿还按揭贷款,而现在这个数字仅为3.4%。另外,“房奴”们还应该感谢新冠疫情——疫情刺激了美国的低利率政策,也导致了抵押贷款和PMI(私人抵押贷款保险)的降低。

不过,目前美国房地产市场仍然有两大不确定性因素。首先,如果美联储(Federal Reserve)由于担心通胀影响而选择提前加息,这将对房市产生立竿见影的负面影响。第二个风险到是今年9月底,抵押贷款延期计划即将结束。目前仍然有170多万人按照该计划可以缓交贷款。当然,如果到时候其中的一部分人出现了断供的情况,而且选择了卖房而非续供,那么这有可能会导致库存房源数量的上升。但即便如此,也不太可能造成供应过剩:Home.LLC公司为《财富》杂志所做的一项分析显示,抵押贷款延期计划的结束,只会导致房源库存暂时性增加11%。(财富中文网)

译者:朴成奎

The flaming-hot housing market has seen median home prices soar an unprecedented 24% since the outbreak of the virus last year. But in recent weeks, that fire has lost some of its heat as buyers finally start to push back at sky-high prices. Simply put: The housing market is slowing a bit.

Already, a growing list of doomsayers point to the shifting market as taking us one step closer to a bursting housing bubble. In their minds, housing went up too fast and now must come back down. Investor Peter Boockvar chimed in last week on CNBC: “I feel bad for the people who bought homes over the past year because they’re the ones that paid the very elevated prices.”

But what does the data say? When you look under the hood, the run-up to 2008 housing bubble and the hot 2021 housing market are very different bull markets. While there are several reasons why our latest frenzy won’t result in a bust, there’s one reason in particular that really stands out.

Before we get to the answer, we need to look back at the last crash.

In the years leading up to the financial crisis, a complete and utter frenzy overtook the housing market. Ready to profit, homebuilders went on a building spree. It meant that once the market started to slow in 2006, the surplus of new constructions quickly put negative pressure on prices. The housing supply glut only got worse when underwater borrowers foreclosed. It took years for housing to shake that glut.

How does that compare with 2021? Well, they’re very different—almost polar opposites. Burned by the 2008 crisis, homebuilders have been extremely conservative in recent years. In the eight years leading up to the Great Recession, homebuilders averaged 1.7 million monthly housing starts. Meanwhile, over the past eight years (2013 to 2021) they’ve averaged just 1.2 million per month. The problem? Recent levels of building aren’t growing fast enough to keep up with population growth. Indeed, our nation is under-built by about 3.8 million single-family homes, according to Freddie Mac.

Timid levels of building coupled with strong demand is why housing inventory—the number of homes for sale—was falling even before the pandemic. The rush of buyers into the market during the pandemic only made matters worse. Between April 2020 to April 2021, housing inventory fell over 50%. Though it has since ticked up, we’re still near a 40-year low.

This is a long-winded way of saying a supply glut is unlikely to return anytime soon. That’s the No. 1 reason a housing market crash is unlikely. Sure, price growth could go flat or even fall without a supply glut—but a 2008-style crash is improbable without it.

CoreLogic, a real estate research firm, forecasts just a 3.2% appreciation coming in the next 12 months. But let’s say CoreLogic is wrong, and prices fall a bit. In that scenario, sidelined buyers—who got worn down after losing bidding war after bidding war in 2021—could rush back into the market. Of course, that would halt a big upswing in supply.

“The fed-up shoppers have seen how much prices have risen and how quickly and don’t feel comfortable jumping in at today’s levels,” Ali Wolf, chief economist at Zonda, a housing market research firm, told Fortune. “These shoppers play an important role as the housing market softens a bit. If some of them jump in as the market slows, they could put a floor on how much the market softens. The buyers on the sidelines now can actually help extend the life of the housing cycle.”

Even with the recent cooling, the market still has a lot going for it. As Fortune has previously reported, we’re in the middle of the five-year period during which the largest tranche of millennials, those born between 1989 and 1993, are hitting their thirties—the age when first-time homebuying really kicks into gear.

Another reason a crash is unlikely: When factoring in income levels, housing costs are lower now than heading into 2008. Leading up to the foreclosure crisis, 7.2% of U.S. personal income was going toward mortgage payments. In 2021, that figure is just 3.4%. In part, homebuyers have the pandemic to thank: It spurred low interest rates and lowered mortgage and PMI (private mortgage insurance) payments.

That said, there are two big wild cards. If inflation fears cause the Federal Reserve to move up its timeline on higher rates, it would have an instant negative effect on the market. The second risk is posed by the wind down at the end of September of the mortgage forbearance program, which allows some borrowers to pause their payments. The program still protects 1.7 million borrowers. Of course, if those buyers face foreclosure or simply opt to sell rather than restart payments, then it could cause the number of homes for sale to rise. But even that is unlikely to create a supply glut: An analysis done by Home.LLC for Fortune forecasts the end of mortgage forbearance would only cause a temporary 11% rise in inventory.

请打开财富Plus APP