为什么这是“一款英雄的应用程序”?

方绘香(Erika Fry)

2021-05-11

美国每个月有上万人因买不起药而死亡。

文本设置

文本设置

Plus(0条)

Plus(0条)

布拉德·怀特有胃酸反流的老毛病,所以需要长年服用埃索美拉唑,这种药物是阿斯利康公司的专利药物耐信的非专利版本。怀特是得克萨斯州南湖市的一名退休的学校行政人员,可以享受医保。不过今年年初,他开车到当地的CVS药店取药时,还是被吓了一跳——药店的工作人员告诉他,要想购买三个月的药量,他还得自付490美元。

他也不记得自己以前在买药上花了多少钱——以前的处方药都是邮寄来的,买药的钱都是通过自动扣款。不过他知道,在达到3000美元的自付额之前,他自己还是得在买药上多花不少钱。一想到吃几个月的非专利药,就得花将近500美元的高价,他实在难以接受。所以他没有拿药就走了,打算“重新部署”一下自己的用药计划。

回到家后,怀特开始在谷歌上搜索“低药价”等关键词。很快,他发现了一家名叫GoodRx的药品折扣公司。凭借该公司赠送给他的优惠券,他能够在不动用医保的前提下,以17美元的超低价,从附近的一家克罗格药店拿到一个月的药量。

他说:“我当时觉得:‘这肯定不可行!’但没有想到,它竟然真的可行。”

他最近又利用这款应用程序购买了另外一种处方药。如果使用医保的话,购买一个月的药量,需要自付36美元。而在GoodRx上,只需要花费16.6美元。所以他当然选择了这个花钱更少的渠道。怀特也知道,买药不用医保,相当于有便宜不占,但他并不介意。

“当药价存在这么大的差距时,只要做个简单的计算,你就会知道,最好不使用医保。老实说,我也觉得这很奇怪。”

在和药店的药剂师聊天时,怀特惊讶地发现,药店不仅接受GoodRx的优惠券,连这位药剂师自己,也会使用GoodRx的优惠券,以更低的价格购买他的哮喘药。

今年早些时候,我跟怀特谈到这件事情时,他还处在一种既开心又将信将疑的状态,因为他觉得这里似乎有一个“悖论”。

“我疑惑的是,这种情况到底可以持续多久?因为如果有人在赚钱的话,就肯定有人在亏钱,只不过我不知道谁亏谁赚。”

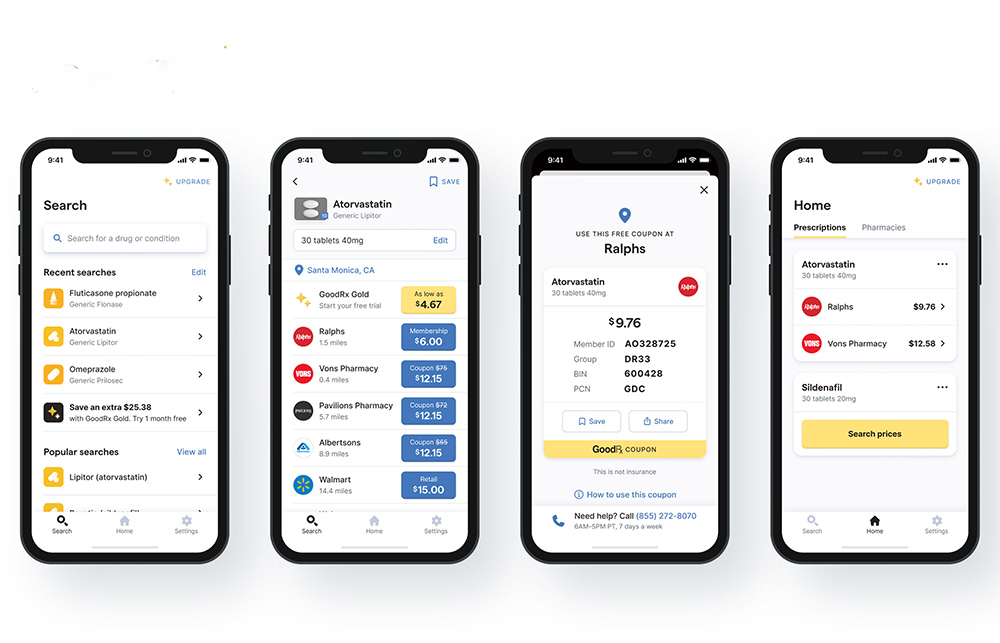

你大概也能够理解怀特的困惑吧?如今在美国,每个月都有560万人通过GoodRx购买打折的处方药。GoodRx有一个免费的应用程序,它会显示多家零售药店的处方药价格,并且提供相应的优惠券。

目前,它已经是苹果的iTunes和谷歌的GooglePlay上下载次数最多的医疗类应用程序之一。该公司官网的月访问量达到了1800万次以上。该公司的服务深受消费者的喜爱,并且也被医生们大力推荐。

ProPublica、《纽约时报》和《财富》等媒体也对它赞誉有加。

《财富》杂志甚至将它列入2019年的“改变世界”排行榜。该公司的“净推广分数”——或者说忠诚度评分,几乎超过了90分。相比之下,苹果最新的忠诚度得分只有47分,沃尔格林(Walgreens)是25分,Facebook是负21分。

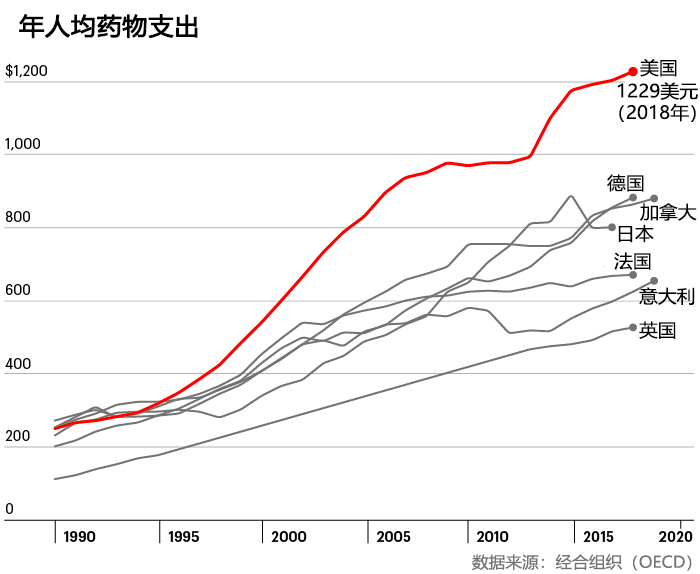

GoodRx何以受到热捧?理由很明显:该公司称,从2011年以来,它已经为广大消费者节省了合计超过250亿美元的买药成本。而从2019年以来,它几乎每天都可以为消费者节省2000万美元的买药支出。考虑到美国有5800万人存在买不起药的问题,每个月估计有上万人因为买不起药物而死亡,它已经堪称是一款英雄的应用程序了。

当然,GoodRx是一家商业企业,不是慈善机构。事实证明,帮助大家节省买药钱,这本身就是一笔好生意。

去年该公司的营收为5.507亿美元,较2019年增长42%。要知道,受新冠疫情影响,去年美国医疗保健服务的消费量实际上是受到抑制的,医生开出的处方数也要低于往年。(根据医疗数据公司IQVIA的数据,2010年美国开具的处方量下降了3%。)另外,GoodRx已经实现了盈利。2020年上半年,它的净利润同比增长了75%,达到5500万美元。(不过由于IPO的相关成本,GoodRx的全年亏损额仍然达到2.94亿美元。)

华尔街也看好GoodRx这种貌似违反直觉的商业模式。去年9月,GoodRx通过IPO实现上市,这也是去年规模最大的20宗IPO之一,其交易规模达到11.4亿美元。目前该公司的市值约为158亿美元。

GoodRx常说,有了GoodRx,所有人都成为了赢家。消费者买得起药、存得下钱,从而提高了健康水平。医疗服务供应商和医保公司也是赢家,因为病人更有能力按照处方用药了。制药商、药店和药品福利管理公司(主要负责为医保公司管理用药需求)同样也是赢家,因为有些高价药本来有可能一直在药店里被放到过期,但现在却通过打折的方式处理了出去。(另外,由于客流量提高了,药店也会带来更高的非药物销量。)当然,最大的赢家还是GoodRx。只用了短短10年时间,它就把自己打造成了一个英雄的形象,在盘根错节的美国医疗保健行业里站稳了脚根——虽然其本质还是一家中间商。

****

如果美国的药价体系不是如此复杂的话,GoodRx可能根本不会存在。约翰斯·霍普金斯大学(Johns Hopkins University)的流行病学和医学教授凯莱布·亚历山大说:“美国的药品定价体系可以说是不正常的,而它们找到了在这样一个体系里做生意的好方法。”

亚当·费恩是一名药品经济学家和药品分销专家,也是药物渠道研究所的首席执行官。他在推特上这样评价GoodRx去年的惊人业绩:“哇,药品福利公司的格局被打破了。”

对此,GoodRx的联合创始人、联合首席执行官道格·赫希也并不否认。去年秋天,他告诉我:“我们的成功,恰恰说明美国的医疗体系已经烂到了什么样子。”

GoodRx的联合创始人、联合首席执行官道格·赫希。图片来源:Courtesy of GoodRx

GoodRx的联合创始人、联合首席执行官道格·赫希。图片来源:Courtesy of GoodRx

正是这种市场失灵,才造就了最初的GoodRx。

2010年的一天,赫希到当地的一家药店去买一种药,结果发现他要自付500美元的药费。赫希也是有医保的,他本来以为药费只是这个数字的一个零头。于是他又去了马路对面的另一家药店,结果发现,同样的药品,这里只需要300美元。而到另一个地区,用药成本变成了400美元。赫希愤然离开了药店,但药剂师却追了上来,表示愿意跟赫希谈判。

谈到这次经历时,赫希回忆道:“我的脑子有点崩溃。”赫希曾经是雅虎和Facebook的员工,他也是照片标签功能的创造者之一。作为一名科技从业者,他亲自见证了数字化革命给航空业和房地产等行业带来的透明度和便利性。而处方药市场的水既浑且深,有中间商层层盘剥,价格极不统一,这也恰恰是一个能够颠覆的市场。因此,他和GoodRx的另一位创始人特雷弗·贝兹德克启动了这个耗时10年的创业项目。

赫希表示,这个创业项目起初纯粹是出于好奇,只是想弄清楚药价背后的猫腻。

“坦率地说,刚开始创业的时候,我并不知道药品福利管理公司是干什么的。”他和其他几位创始人开始收集药价信息。

开市客会在其官网上发布药品价格,沃尔玛会以最低4美元的价格销售部分处方药,还有一些州制定了法律,要求药价必须在网上或在药店里公示。这些措施都旨在提高药价的透明度,但它们并未起到应有的效果。

去年秋天他对我说:“这简直是一团糟。”

于是赫希和他的团队开始打电话给各个药店的药剂师,并且面向整个医疗界寻求帮助。

在《平价医疗法案》刚出台的日子里,很多人都觉得他们的努力是划不来的。大家要么认为美国医疗体系的漏洞已经被弥补了,要么认为现有体系不可能被颠覆。不过还是有足够的人支持他们,包括药品福利管理公司MedImpact的一名员工。MedImpact最终也成了GoodRx的首批合作伙伴之一。赫希称:“大门总是向我们敞开的。”

随着时间的累积,赫希的团队已经收集了足够的药价信息,足以让该公司的数据团队发现药品福利管理公司与药店之间无比复杂的合同里隐藏的猫腻。他们发现,不同地方的药价,往往相差巨大,特别是那些低成本的常用非专利药品。要想理解处方药市场的运行机制,首先要解决一个巨大且复杂的数据工程问题。不过GoodRx已经解决了这个问题。

到2011年,该公司已经建立了一个网站和一个产品——这是一个简单的数字化工具,它可以清晰地展示不同销售点的处方药价格,然而引导消费者到价格最低的地方去购买。随着时间的推移,该公司的数据库也变得愈发复杂和完整。

赫希表示,GoodRx现在几乎能够从所有的药品福利管理公司渠道获得药价信息,此外它还有其他的信息来源,所以它的系统每天都可以收集2000多亿条价格信息。

德意志银行的医疗保健技术与服务证券研究部总经理乔治·希尔认为,虽然GoodRx只是简单地对药价进行了比较,让消费者可以去低价的地方买药,但这已经是行业一个了不起的突破了。他指出,一个美国人平均每年要购买11种处方药。“GoodRx确实是医疗保健行业第一个被广泛接受和采用的价格透明度工具。”

****

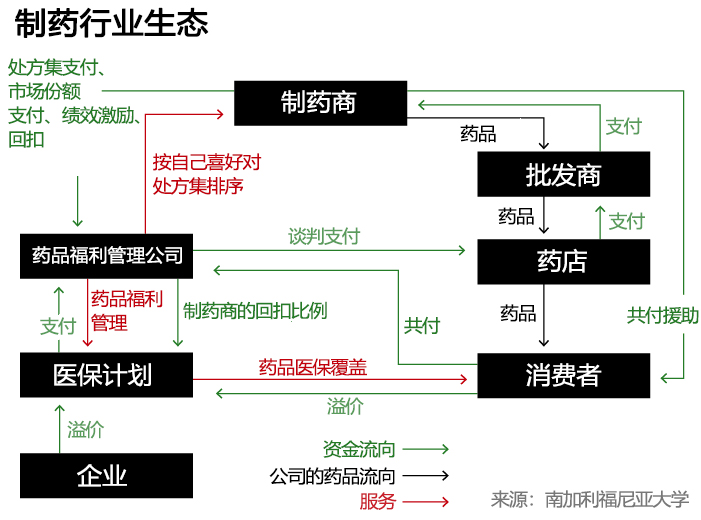

那么,GoodRx的运行机制到底是什么?或者更准确地说,它到底是怎样赚钱的?要理解它错综复杂的商业模式,你必须首先了解药店行业的经济生态。不过就像美国医疗行业的许多其他角落一样,药店这个行业的业态,是很难三言两语解释得清的。

这个行业有很多参与者,都在争抢这个5090亿美元的大蛋糕,其中大多数人都是中间商。大家都在通过各种复杂操作试图分一杯羹,比如所谓的回扣、返点、共付等等。对于外行来说,要想知道你用来买药的钱都流向了哪里,其难度简直复杂到无法想象。

在这些参与者中,对GoodRx的成功影响最大的,就是所谓的药品福利管理公司(简称PBM)。PBM最早出现在20世纪60年代,它主要扮演了一个为医保公司管理消费者的处方药需求的角色。这现在仍然是它们的主要业务,不过随着时间的推移,PBM在美国处方药市场上的地位越来越强大,成了一个攫取了大量利益的中间商群体。

PBM是医保公司、制药公司和药店之间的中间商,它可以通过谈判来决定医保公司要向制药公司支付多少钱、消费者要付给药店多少钱,以及药店能够报销多少钱。它们还可以制定处方集,它直接决定了你的医保能够报销哪些药品。它们还可以部署所谓的“医疗服务使用管理工具”,比如预授权机制,以确保你的处方药在医疗上确实具有必要性。有的PBM公司还经营着自己的药店,能够通过邮寄方式来向消费者配送药物,等等。所有这些活动的目的,以及PBM公司自我标榜的目标,表面上就是为了控制购买药品的医保支出。

至于这些PBM公司到底起了多大的作用,这是一个非常有争议的问题。近年来,这个规模高达4020亿美元的庞大产业经常因为不透明的中间商行为而受到诟病。

在过去的10年里,美国最大的三家PBM公司都被大型保险公司吞并,比如信诺旗下的Express Scripts、CVS旗下的Caremark、联合健康旗下的Optum,而且创造了相当可观的收益。可以说,它们赚的每一分钱,都是消费者在药店花出去的钱。而GoodRx瞄准的就是这个问题。

在本文中,我们主要探讨低成本的非专利药市场,因为它是GoodRx为消费者节省最多、同时也是该公司盈利最多的地方。

一般来说,当你去药店购买处方药的时候,你要付给药店多少钱,取决于以下几个因素:一是你医保计划;二是你的医保公司请来管理药品成本的PBM公司;三是你去买药的那家药店。你支付给药店多少钱,取决于你的药店与PBM公司之间的协议价。如果你没有医保,就要按照药店的零售价用现金购买,而这个价格通常是非常昂贵的。

这就是为什么同一款药品,不同的人去买,或者在不同的药店购买,价格相差会如此巨大。

佐治亚州埃尔伯顿的独立药店Madden’s的老板兼药剂师小唐恩·皮拉说:“如果有10个人在麦当劳排队买同样的快乐儿童餐,那么所有人支付的金额都是一样的,不管你是用现金还是刷信用卡,也不管你是什么人。但是在医疗行业,特别是在药品行业,如果有10个人排队,想购买30片降压药,那么10个人掏的钱都不一样,或者说他们的医保支付的钱都不一样。”他也认为这个体系“很荒唐”,更糟糕的是“没有透明度”。

GoodRx的应用程序正是围绕医药行业的这一漏洞打造的。它展示了PBM公司和各大药店谈判达成的所有价格,而消费者可以持GoodRx提供的优惠券,到任意一家药店去购买。

不过,具有讽刺意味的是,通过与多家PBM公司的合作,这种优惠本身也成了一种赚钱的门路。

例如据赫希介绍,当一名消费者拿着GoodRx的优惠券,在当地的某家药店购买了某种低价药品时,PBM公司也会给GoodRx一笔“介绍费”。(这笔费用贡献了GoodRx收入的90%。)这种交易对PBM公司来说也是很划算的,因为它们由此进入了一个全新的收入领域。

南加利福尼亚大学谢弗中心的医疗政策主任、医疗经济学家杰弗里·乔伊斯称:“对那些没有医保的消费者来说,他们相当于扮演了一个PBM公司的角色。”这一部分利润是相当可观的。“没有医保的消费者是药店的现金大户。他们为非专利药支付了高得离谱的价格。”

GoodRx并不是第一家奉行这个战略的公司。在美国,药品折扣卡这个东西已经存在几十年了,它能够让消费者以更便宜的价格,从PBM公司指定的药店网络购买处方药。只不过GoodRx的网络更加复杂和强大,它的PBM合作伙伴已经超过了12家,所以它不仅掌握了他们所有药店网络的零售价,也可以提供更大范围的折扣。(另外,GoodRx还开发了一个先进的技术网络,用来帮消费者省钱。同时它在市场推广上也不惜血本。)

“所以通常情况下,他们会有一个很好的价格。”德意志银行网络证券研究部的总经理劳埃德·沃姆斯利说。

凯蒂·雷·艾利森是怀俄明州吉列市的一家珠宝店的经理兼设计师。她从小就患有甲状腺疾病,每天都需要服药控制,否则健康就会受到影响。她工作的地方并不提供医保。所以今年年初,她第一次接触到GoodRx的应用程序时,她既感到如释重负,但也抱有几分怀疑。

她对我说:“它好得简直难以置信。”她只花了25美元,就买到了90天的药量。而如果没有GoodRx的优惠券的话,她一个月的药费就得达到32美元。“现在,三个月的药量只花了不到以前一个月的钱。按照一年来计算的话,它会给我省下很多钱。”

不过,在GoodRx的用户中,像艾利森这样没有医疗保险的只是少数。据该公司介绍,它75%的用户都有某种形式的医疗保险(包括Medicare等政府医保)。

当这些消费者使用GoodRx的优惠券在一家药店低价购买处方药时,他们就不会动用医保。这样一来,得利就是GoodRx和在那家药店拥有最低协议价格的PBM公司,而不是消费者的医保公司指定的PBM公司。

为什么这么多人宁愿通过GoodRx自付药费,也不动用辛辛苦苦工作换来的医疗保险呢?很多人是出于跟上文的布拉德·怀特相同的考虑——即便我动用了医保,我也得自付一部分高额药费。这也是因为近年来,很多雇主选择了高自付额度的医保方案。在这种医保方案下,用户至少要先自付1400美元,之后才能够启动医保报销。

根据凯撒家族基金会的数据,过去10年间,美国人的平均自付金额从917美元上涨至1644美元,增长率达到111%。雇主的初衷是想让雇员提高医疗保险的成本意识,但在实际上,它并没有起到预期的效果。很多人反而因此而付不起高额的医疗账单。研究表明,在高自付额医保计划下,人们会更倾向于推迟或放弃治疗。

GoodRx可以减轻医保用户的短期经济压力,但这也是有代价的。由于是通过现金支付的,消费者相当于没有动用自己的医保自付额度,这样一来,也就延迟了他们享受医保福利的机会——要知道,消费者和他们的雇主每月可是要在医保上缴纳不少钱的。(根据凯撒家庭基金会的数据,2020年,美国个人的人均保费是7470美元,家庭的平均保费是21342美元。)

哈佛商学院的教授利莫尔·达芙尼也担心,由于GoodRx的支出不计入自付额度,一些医保消费者最终花出去的钱有可能会更多。(GoodRx在其官网上提供了医保消费指引,比如如何提交收据和填写保险报销单等,以便让消费者在GoodRx上的消费能够被计入医保自付额度。不过该公司并没有做出太多承诺。该公司的一位发言人表示:“你很可能得不到报销,但你总是可以尝试一下的。”)

不过,一些有医保的消费者之所以使用GoodRx,往往不仅仅是为了省钱,而是因为医保系统的官僚主义严重影响了治疗,而不得不求助于GoodRx。比如马萨诸塞州伍斯特市的中学数学老师亚伊拉·帕金斯。

今年33岁的帕金斯是两个孩子的母亲,她一直过着充实而积极的生活。但2019年年末,她开始出现了系统性硬皮病的奇怪症状,身体日渐衰弱。2020年年初,她才确诊患有这种罕见的自体免疫性疾病。虽然这种病并不危及生命,但像其他自体免疫性疾病一样,它的致病机理尚不为人所知,也无法彻底治愈。

对这种自体免疫性疾病,医生会给他们开一些原本用来治疗其他疾病的药物,这些药物有时候会有效。帕金斯的病每天都会发作几次,医生给了她开了几种免疫抑制剂,几种治疗高血压和痤疮的药物,还有一些面霜、肉毒杆菌素,甚至还有非专利版的伟哥(西地那非),希望这些能够控制住她的病情。

起初,帕金斯的保险公司拒绝报销其中的很多药物,理由是这些药物并不是针对她的病情的指定疗法。为此她和她的医生花了几周甚至几个月的时间去申诉。比如西地那非可以缓解她双手血液循环不畅的问题,而90天的西地那非的费用就高达1363.89美元。不过在用了医生给她的GoodRx优惠券后,她实际只支付了19.37美元。

帕金斯的故事并非个例。美国国家公共电台、罗伯特·伍德·约翰逊基金会和哈佛公共卫生学院去年的一项联合调查显示,美国有超过三分之一的成年人和将近一半的低收入家庭,都曾经被告知,他们的医保计划无法报销医生开具给他们的某一款处方药。

虽然帕金斯很感激GoodRx让她终于负担得起这些药物,但她的心情依然五味杂陈。今年2月,她对我说:“整个体系都出了问题,这些公司——我不知道它们是如何盈利的,但我非常确定,如果你深入研究的话,你会发现,不仅它们在攫取利益,整个私营保险行业也在攫取利益。”

从她和很多人的遭遇看,她说的一点不错。帕金斯的医保公司(以及该医保公司指定的PBM公司)虽然收了她缴纳的保费,但她却还要自己掏钱给GoodRx和另一家PBM公司。

****

那么,我们应该如何看待GoodRx,以及它在美国医疗体系中扮演的角色呢?这是一个很复杂的问题。

约翰斯·霍普金斯大学的卡莱布·亚历山大深入研究了“药价抵消”的问题——比如GoodRx的优惠券。他发现,消费者节省下来的钱,主要集中在相对少量的非专利药上。抵消的费用相对来说也并不高——大约是每笔交易16美元,但它平均为用户节省了约40%的自付费用。虽然他担心这种价格采购可能会营造一种碎片化的环境,让慢性病患者难以持续、稳定地获得药品,但还是要肯定它的优点。

他表示:“这些类型的折扣,最终会给消费者带来很大的转变。”

就连密歇根大学的价值型保险设计中心的主任、内科医生马克·芬德里克,也在自己办公室的电脑旁边放了一叠GoodRx的优惠券,以便那些付不起基本药品费用的病人使用。他对美国的医保体系有清醒的认识,他指出,GoodRx“是一个证明了整个定价、报销、分配系统有多混乱的经典案例。”在这个体系得到修正前,他支持病人通过GoodRx或其他形式的辅助手段(例如众筹捐款等等)获得必需的药物。

最近,他就通过这款应用程序为他生病的宠物犬贝拉购买了60片西地那非,GoodRx让省下了整整720美元,他自己只支付了33美元——折扣高达95%。他还表示,如果他肯去城市另一边的另一家药店,他还可以再省一些钱。

南加州大学的乔伊斯也认为,GoodRx为那些负担不起基本药品的人提供了一条活路。不过对于那些已经购买了医保的消费者,GoodRx的作用比较难以评估,它对美国消费者总体医疗出支出的影响也同样难以评估。

乔伊斯说:“它们不是圣人,它们这样做是为了赚钱,而且它们的生意也是非常有利可图的。”

虽然GoodRx为人们提供了大量的药价数据,但乔伊斯认为,GoodRx并未让整个医疗体系变得更加透明。“它们没有带来更高的透明度,它们的价格仍然高于采购成本,它们并没有把价格压低到边际成本。”

此外,乔伊斯等人也不相信GoodRx真的像它声称的那样为消费者节省了那么多钱。

马里兰大学药学院的副教授乔伊·马丁利认为,在宣传替消费者省钱上,GoodRx用了和PBM公司相同的数学花招——即假定一名消费者如果没有使用GoodRx的优惠券,他就会按照最高的价格买药。(从GoodRx公司对相关数据的解释看,马丁利的怀疑很有可能是正确的。)

尽管如此,马丁利还是认为,GoodRx能够给消费者带来很有意义的转变,尤其是对那些没有医保的人。

不过站在GoodRx的角度,赫希认为,为消费者节省250亿美元还是一种保守的说法。

“我认为在确保病人按时用药、使病人尽量少去急诊等方面,我们的实际影响还要大得多。有了GoodRx,消费者可以支付全部的处方药费用,所以保险公司、付款人和政府的负担都会有所减轻。”根据该公司的分析,它已经让2200多万美国人买得起药了。

乔伊斯并未把“不透明”的帽子扣在GoodRx头上。他说:“它突显了药品供应链的浪费和低效,以及药价的低透明度。而PBM公司才是真正的罪魁祸首。”

2018年,《美国医学会杂志》发表了乔伊斯和他的同事的一篇研究。研究发现,在22%的情况下,消费者对处方药的共付费用超过了药品本身的成本。换句话说,患者并非是“共付”,而是“过度支付”了药价。从中得利的恰恰是PBM和保险公司。

更过分的是,直到最近,很多药店还在以合同的形式,禁止药剂师提醒医保病人他们支付的金额可能超过了药品的现金价格(也就是没有医保的病人支付的价格)。

从一些独立药剂师(比如独立药店Madden’s的老板小唐恩·皮拉)的角度看,GoodRx的优惠券,只是PBM公司从药店割肉的另一种方式。

他表示,Madden’s药店的现金价格往往比GoodRx上的价格更加优惠,不过它不会出现在GoodRx的应用程序上。但当消费者使用优惠券时,PBM公司会收取一笔“高额费用”,然后向药店报销一个较低的金额,有时甚至会低于药品的成本。不过即使赔钱卖药,它也必须兑换GoodRx的优惠券,因为它跟相关的PBM公司有协议。

作为一家小药店,和其他独立药房一样,当与强大的PBM公司谈判的时候,Madden’s是没有什么话语权的。而不与PBM打交道则根本不现实。

皮拉也认为,GoodRx提供的折扣,确实可以帮助消费者买得起他们所需的药品。只不过,GoodRx提供给消费者的只是一个“更好”的价格,而并非“最好”的价格。(不过赫希表示,GoodRx“专注于为消费者提供最好的价格。”)

皮拉说:“它们其实什么也没有做。它们没有实际销售一种产品,也没有给病人打电话,给他们提供咨询服务,也没有告诉病人如何用药。它只是做了一个算法,就能够净赚几亿美元,这意味着什么?”

赫希认为,GoodRx不仅仅是一种算法——该公司也一直在扩展其他业务,包括远程医疗,和所谓的“制药商解决方案”。这也是一项高增长、高利润的业务。GoodRx会让各大药物品牌的制药商与在其平台上搜索药品的消费者建立联系。该公司还提供了GoodRx Gold和Kroger Rx省钱俱乐部等会员服务,会员可以享受到比应用程序更优惠的药价。该公司还发布了药品价格研究报告,并就改善药品行业生态,提供了一些最清晰的、最有利于消费者的见解。

去年11月,在亚马逊宣布启动自己的药品优惠计划后,GoodRx的股价出现了短暂的下跌。不过GoodRx的高管表示,从业务上看,GoodRx对亚马逊的进入并没有什么可以担忧的。(另外,消费者还能够在亚马逊的药店使用GoodRx的优惠券。)

德意志银行网络证券研究部的总经理劳埃德·沃姆斯利和瑞士信贷的分析师杰伦德拉·辛格等分析师也认为,GoodRx的业务当前面临的威胁是被夸大了的。

赫希表示,他认为公司业务面临的最大障碍,是很多老百姓仍然不了解药价背后的猫腻,不了解自己本可以享受到更优惠的价格,仍然像以前一样购买处方药。

赫希对我说:“我们最大的竞争对手,就是那些不知道本来能够获得更优惠的药价的美国人。”他希望GoodRx品牌可以成为美国消费者最信赖的伙伴。

很多第一次使用GoodRx的人——比如上文提到的怀特和艾利森,都给出了几乎不可思议的评价,认为GoodRx“好得难以置信”。他们能够相对轻松、简单地在药店完成购买,而且药价还很便宜。在买药的过程中,人们没有医保卡也可以享受同样的服务,而且不用考虑共付、自付、PBM和医保这些糟心事。

当然,美国医疗行业的这些糟心事和种种深层问题仍然存在。GoodRx只是一家让你忘了这些问题的中间商。(财富中文网)

译者:朴成奎

布拉德·怀特有胃酸反流的老毛病,所以需要长年服用埃索美拉唑,这种药物是阿斯利康公司的专利药物耐信的非专利版本。怀特是得克萨斯州南湖市的一名退休的学校行政人员,可以享受医保。不过今年年初,他开车到当地的CVS药店取药时,还是被吓了一跳——药店的工作人员告诉他,要想购买三个月的药量,他还得自付490美元。

他也不记得自己以前在买药上花了多少钱——以前的处方药都是邮寄来的,买药的钱都是通过自动扣款。不过他知道,在达到3000美元的自付额之前,他自己还是得在买药上多花不少钱。一想到吃几个月的非专利药,就得花将近500美元的高价,他实在难以接受。所以他没有拿药就走了,打算“重新部署”一下自己的用药计划。

回到家后,怀特开始在谷歌上搜索“低药价”等关键词。很快,他发现了一家名叫GoodRx的药品折扣公司。凭借该公司赠送给他的优惠券,他能够在不动用医保的前提下,以17美元的超低价,从附近的一家克罗格药店拿到一个月的药量。

他说:“我当时觉得:‘这肯定不可行!’但没有想到,它竟然真的可行。”

他最近又利用这款应用程序购买了另外一种处方药。如果使用医保的话,购买一个月的药量,需要自付36美元。而在GoodRx上,只需要花费16.6美元。所以他当然选择了这个花钱更少的渠道。怀特也知道,买药不用医保,相当于有便宜不占,但他并不介意。

“当药价存在这么大的差距时,只要做个简单的计算,你就会知道,最好不使用医保。老实说,我也觉得这很奇怪。”

在和药店的药剂师聊天时,怀特惊讶地发现,药店不仅接受GoodRx的优惠券,连这位药剂师自己,也会使用GoodRx的优惠券,以更低的价格购买他的哮喘药。

今年早些时候,我跟怀特谈到这件事情时,他还处在一种既开心又将信将疑的状态,因为他觉得这里似乎有一个“悖论”。

“我疑惑的是,这种情况到底可以持续多久?因为如果有人在赚钱的话,就肯定有人在亏钱,只不过我不知道谁亏谁赚。”

你大概也能够理解怀特的困惑吧?如今在美国,每个月都有560万人通过GoodRx购买打折的处方药。GoodRx有一个免费的应用程序,它会显示多家零售药店的处方药价格,并且提供相应的优惠券。

目前,它已经是苹果的iTunes和谷歌的GooglePlay上下载次数最多的医疗类应用程序之一。该公司官网的月访问量达到了1800万次以上。该公司的服务深受消费者的喜爱,并且也被医生们大力推荐。

ProPublica、《纽约时报》和《财富》等媒体也对它赞誉有加。

《财富》杂志甚至将它列入2019年的“改变世界”排行榜。该公司的“净推广分数”——或者说忠诚度评分,几乎超过了90分。相比之下,苹果最新的忠诚度得分只有47分,沃尔格林(Walgreens)是25分,Facebook是负21分。

GoodRx何以受到热捧?理由很明显:该公司称,从2011年以来,它已经为广大消费者节省了合计超过250亿美元的买药成本。而从2019年以来,它几乎每天都可以为消费者节省2000万美元的买药支出。考虑到美国有5800万人存在买不起药的问题,每个月估计有上万人因为买不起药物而死亡,它已经堪称是一款英雄的应用程序了。

当然,GoodRx是一家商业企业,不是慈善机构。事实证明,帮助大家节省买药钱,这本身就是一笔好生意。

去年该公司的营收为5.507亿美元,较2019年增长42%。要知道,受新冠疫情影响,去年美国医疗保健服务的消费量实际上是受到抑制的,医生开出的处方数也要低于往年。(根据医疗数据公司IQVIA的数据,2010年美国开具的处方量下降了3%。)另外,GoodRx已经实现了盈利。2020年上半年,它的净利润同比增长了75%,达到5500万美元。(不过由于IPO的相关成本,GoodRx的全年亏损额仍然达到2.94亿美元。)

华尔街也看好GoodRx这种貌似违反直觉的商业模式。去年9月,GoodRx通过IPO实现上市,这也是去年规模最大的20宗IPO之一,其交易规模达到11.4亿美元。目前该公司的市值约为158亿美元。

GoodRx常说,有了GoodRx,所有人都成为了赢家。消费者买得起药、存得下钱,从而提高了健康水平。医疗服务供应商和医保公司也是赢家,因为病人更有能力按照处方用药了。制药商、药店和药品福利管理公司(主要负责为医保公司管理用药需求)同样也是赢家,因为有些高价药本来有可能一直在药店里被放到过期,但现在却通过打折的方式处理了出去。(另外,由于客流量提高了,药店也会带来更高的非药物销量。)当然,最大的赢家还是GoodRx。只用了短短10年时间,它就把自己打造成了一个英雄的形象,在盘根错节的美国医疗保健行业里站稳了脚根——虽然其本质还是一家中间商。

****

如果美国的药价体系不是如此复杂的话,GoodRx可能根本不会存在。约翰斯·霍普金斯大学(Johns Hopkins University)的流行病学和医学教授凯莱布·亚历山大说:“美国的药品定价体系可以说是不正常的,而它们找到了在这样一个体系里做生意的好方法。”

亚当·费恩是一名药品经济学家和药品分销专家,也是药物渠道研究所的首席执行官。他在推特上这样评价GoodRx去年的惊人业绩:“哇,药品福利公司的格局被打破了。”

对此,GoodRx的联合创始人、联合首席执行官道格·赫希也并不否认。去年秋天,他告诉我:“我们的成功,恰恰说明美国的医疗体系已经烂到了什么样子。”

正是这种市场失灵,才造就了最初的GoodRx。

2010年的一天,赫希到当地的一家药店去买一种药,结果发现他要自付500美元的药费。赫希也是有医保的,他本来以为药费只是这个数字的一个零头。于是他又去了马路对面的另一家药店,结果发现,同样的药品,这里只需要300美元。而到另一个地区,用药成本变成了400美元。赫希愤然离开了药店,但药剂师却追了上来,表示愿意跟赫希谈判。

谈到这次经历时,赫希回忆道:“我的脑子有点崩溃。”赫希曾经是雅虎和Facebook的员工,他也是照片标签功能的创造者之一。作为一名科技从业者,他亲自见证了数字化革命给航空业和房地产等行业带来的透明度和便利性。而处方药市场的水既浑且深,有中间商层层盘剥,价格极不统一,这也恰恰是一个能够颠覆的市场。因此,他和GoodRx的另一位创始人特雷弗·贝兹德克启动了这个耗时10年的创业项目。

赫希表示,这个创业项目起初纯粹是出于好奇,只是想弄清楚药价背后的猫腻。

“坦率地说,刚开始创业的时候,我并不知道药品福利管理公司是干什么的。”他和其他几位创始人开始收集药价信息。

开市客会在其官网上发布药品价格,沃尔玛会以最低4美元的价格销售部分处方药,还有一些州制定了法律,要求药价必须在网上或在药店里公示。这些措施都旨在提高药价的透明度,但它们并未起到应有的效果。

去年秋天他对我说:“这简直是一团糟。”

于是赫希和他的团队开始打电话给各个药店的药剂师,并且面向整个医疗界寻求帮助。

在《平价医疗法案》刚出台的日子里,很多人都觉得他们的努力是划不来的。大家要么认为美国医疗体系的漏洞已经被弥补了,要么认为现有体系不可能被颠覆。不过还是有足够的人支持他们,包括药品福利管理公司MedImpact的一名员工。MedImpact最终也成了GoodRx的首批合作伙伴之一。赫希称:“大门总是向我们敞开的。”

随着时间的累积,赫希的团队已经收集了足够的药价信息,足以让该公司的数据团队发现药品福利管理公司与药店之间无比复杂的合同里隐藏的猫腻。他们发现,不同地方的药价,往往相差巨大,特别是那些低成本的常用非专利药品。要想理解处方药市场的运行机制,首先要解决一个巨大且复杂的数据工程问题。不过GoodRx已经解决了这个问题。

到2011年,该公司已经建立了一个网站和一个产品——这是一个简单的数字化工具,它可以清晰地展示不同销售点的处方药价格,然而引导消费者到价格最低的地方去购买。随着时间的推移,该公司的数据库也变得愈发复杂和完整。

赫希表示,GoodRx现在几乎能够从所有的药品福利管理公司渠道获得药价信息,此外它还有其他的信息来源,所以它的系统每天都可以收集2000多亿条价格信息。

德意志银行的医疗保健技术与服务证券研究部总经理乔治·希尔认为,虽然GoodRx只是简单地对药价进行了比较,让消费者可以去低价的地方买药,但这已经是行业一个了不起的突破了。他指出,一个美国人平均每年要购买11种处方药。“GoodRx确实是医疗保健行业第一个被广泛接受和采用的价格透明度工具。”

****

那么,GoodRx的运行机制到底是什么?或者更准确地说,它到底是怎样赚钱的?要理解它错综复杂的商业模式,你必须首先了解药店行业的经济生态。不过就像美国医疗行业的许多其他角落一样,药店这个行业的业态,是很难三言两语解释得清的。

这个行业有很多参与者,都在争抢这个5090亿美元的大蛋糕,其中大多数人都是中间商。大家都在通过各种复杂操作试图分一杯羹,比如所谓的回扣、返点、共付等等。对于外行来说,要想知道你用来买药的钱都流向了哪里,其难度简直复杂到无法想象。

在这些参与者中,对GoodRx的成功影响最大的,就是所谓的药品福利管理公司(简称PBM)。PBM最早出现在20世纪60年代,它主要扮演了一个为医保公司管理消费者的处方药需求的角色。这现在仍然是它们的主要业务,不过随着时间的推移,PBM在美国处方药市场上的地位越来越强大,成了一个攫取了大量利益的中间商群体。

PBM是医保公司、制药公司和药店之间的中间商,它可以通过谈判来决定医保公司要向制药公司支付多少钱、消费者要付给药店多少钱,以及药店能够报销多少钱。它们还可以制定处方集,它直接决定了你的医保能够报销哪些药品。它们还可以部署所谓的“医疗服务使用管理工具”,比如预授权机制,以确保你的处方药在医疗上确实具有必要性。有的PBM公司还经营着自己的药店,能够通过邮寄方式来向消费者配送药物,等等。所有这些活动的目的,以及PBM公司自我标榜的目标,表面上就是为了控制购买药品的医保支出。

至于这些PBM公司到底起了多大的作用,这是一个非常有争议的问题。近年来,这个规模高达4020亿美元的庞大产业经常因为不透明的中间商行为而受到诟病。

在过去的10年里,美国最大的三家PBM公司都被大型保险公司吞并,比如信诺旗下的Express Scripts、CVS旗下的Caremark、联合健康旗下的Optum,而且创造了相当可观的收益。可以说,它们赚的每一分钱,都是消费者在药店花出去的钱。而GoodRx瞄准的就是这个问题。

在本文中,我们主要探讨低成本的非专利药市场,因为它是GoodRx为消费者节省最多、同时也是该公司盈利最多的地方。

一般来说,当你去药店购买处方药的时候,你要付给药店多少钱,取决于以下几个因素:一是你医保计划;二是你的医保公司请来管理药品成本的PBM公司;三是你去买药的那家药店。你支付给药店多少钱,取决于你的药店与PBM公司之间的协议价。如果你没有医保,就要按照药店的零售价用现金购买,而这个价格通常是非常昂贵的。

这就是为什么同一款药品,不同的人去买,或者在不同的药店购买,价格相差会如此巨大。

佐治亚州埃尔伯顿的独立药店Madden’s的老板兼药剂师小唐恩·皮拉说:“如果有10个人在麦当劳排队买同样的快乐儿童餐,那么所有人支付的金额都是一样的,不管你是用现金还是刷信用卡,也不管你是什么人。但是在医疗行业,特别是在药品行业,如果有10个人排队,想购买30片降压药,那么10个人掏的钱都不一样,或者说他们的医保支付的钱都不一样。”他也认为这个体系“很荒唐”,更糟糕的是“没有透明度”。

GoodRx的应用程序正是围绕医药行业的这一漏洞打造的。它展示了PBM公司和各大药店谈判达成的所有价格,而消费者可以持GoodRx提供的优惠券,到任意一家药店去购买。

不过,具有讽刺意味的是,通过与多家PBM公司的合作,这种优惠本身也成了一种赚钱的门路。

例如据赫希介绍,当一名消费者拿着GoodRx的优惠券,在当地的某家药店购买了某种低价药品时,PBM公司也会给GoodRx一笔“介绍费”。(这笔费用贡献了GoodRx收入的90%。)这种交易对PBM公司来说也是很划算的,因为它们由此进入了一个全新的收入领域。

南加利福尼亚大学谢弗中心的医疗政策主任、医疗经济学家杰弗里·乔伊斯称:“对那些没有医保的消费者来说,他们相当于扮演了一个PBM公司的角色。”这一部分利润是相当可观的。“没有医保的消费者是药店的现金大户。他们为非专利药支付了高得离谱的价格。”

GoodRx并不是第一家奉行这个战略的公司。在美国,药品折扣卡这个东西已经存在几十年了,它能够让消费者以更便宜的价格,从PBM公司指定的药店网络购买处方药。只不过GoodRx的网络更加复杂和强大,它的PBM合作伙伴已经超过了12家,所以它不仅掌握了他们所有药店网络的零售价,也可以提供更大范围的折扣。(另外,GoodRx还开发了一个先进的技术网络,用来帮消费者省钱。同时它在市场推广上也不惜血本。)

“所以通常情况下,他们会有一个很好的价格。”德意志银行网络证券研究部的总经理劳埃德·沃姆斯利说。

凯蒂·雷·艾利森是怀俄明州吉列市的一家珠宝店的经理兼设计师。她从小就患有甲状腺疾病,每天都需要服药控制,否则健康就会受到影响。她工作的地方并不提供医保。所以今年年初,她第一次接触到GoodRx的应用程序时,她既感到如释重负,但也抱有几分怀疑。

她对我说:“它好得简直难以置信。”她只花了25美元,就买到了90天的药量。而如果没有GoodRx的优惠券的话,她一个月的药费就得达到32美元。“现在,三个月的药量只花了不到以前一个月的钱。按照一年来计算的话,它会给我省下很多钱。”

不过,在GoodRx的用户中,像艾利森这样没有医疗保险的只是少数。据该公司介绍,它75%的用户都有某种形式的医疗保险(包括Medicare等政府医保)。

当这些消费者使用GoodRx的优惠券在一家药店低价购买处方药时,他们就不会动用医保。这样一来,得利就是GoodRx和在那家药店拥有最低协议价格的PBM公司,而不是消费者的医保公司指定的PBM公司。

为什么这么多人宁愿通过GoodRx自付药费,也不动用辛辛苦苦工作换来的医疗保险呢?很多人是出于跟上文的布拉德·怀特相同的考虑——即便我动用了医保,我也得自付一部分高额药费。这也是因为近年来,很多雇主选择了高自付额度的医保方案。在这种医保方案下,用户至少要先自付1400美元,之后才能够启动医保报销。

根据凯撒家族基金会的数据,过去10年间,美国人的平均自付金额从917美元上涨至1644美元,增长率达到111%。雇主的初衷是想让雇员提高医疗保险的成本意识,但在实际上,它并没有起到预期的效果。很多人反而因此而付不起高额的医疗账单。研究表明,在高自付额医保计划下,人们会更倾向于推迟或放弃治疗。

GoodRx可以减轻医保用户的短期经济压力,但这也是有代价的。由于是通过现金支付的,消费者相当于没有动用自己的医保自付额度,这样一来,也就延迟了他们享受医保福利的机会——要知道,消费者和他们的雇主每月可是要在医保上缴纳不少钱的。(根据凯撒家庭基金会的数据,2020年,美国个人的人均保费是7470美元,家庭的平均保费是21342美元。)

哈佛商学院的教授利莫尔·达芙尼也担心,由于GoodRx的支出不计入自付额度,一些医保消费者最终花出去的钱有可能会更多。(GoodRx在其官网上提供了医保消费指引,比如如何提交收据和填写保险报销单等,以便让消费者在GoodRx上的消费能够被计入医保自付额度。不过该公司并没有做出太多承诺。该公司的一位发言人表示:“你很可能得不到报销,但你总是可以尝试一下的。”)

不过,一些有医保的消费者之所以使用GoodRx,往往不仅仅是为了省钱,而是因为医保系统的官僚主义严重影响了治疗,而不得不求助于GoodRx。比如马萨诸塞州伍斯特市的中学数学老师亚伊拉·帕金斯。

今年33岁的帕金斯是两个孩子的母亲,她一直过着充实而积极的生活。但2019年年末,她开始出现了系统性硬皮病的奇怪症状,身体日渐衰弱。2020年年初,她才确诊患有这种罕见的自体免疫性疾病。虽然这种病并不危及生命,但像其他自体免疫性疾病一样,它的致病机理尚不为人所知,也无法彻底治愈。

对这种自体免疫性疾病,医生会给他们开一些原本用来治疗其他疾病的药物,这些药物有时候会有效。帕金斯的病每天都会发作几次,医生给了她开了几种免疫抑制剂,几种治疗高血压和痤疮的药物,还有一些面霜、肉毒杆菌素,甚至还有非专利版的伟哥(西地那非),希望这些能够控制住她的病情。

起初,帕金斯的保险公司拒绝报销其中的很多药物,理由是这些药物并不是针对她的病情的指定疗法。为此她和她的医生花了几周甚至几个月的时间去申诉。比如西地那非可以缓解她双手血液循环不畅的问题,而90天的西地那非的费用就高达1363.89美元。不过在用了医生给她的GoodRx优惠券后,她实际只支付了19.37美元。

帕金斯的故事并非个例。美国国家公共电台、罗伯特·伍德·约翰逊基金会和哈佛公共卫生学院去年的一项联合调查显示,美国有超过三分之一的成年人和将近一半的低收入家庭,都曾经被告知,他们的医保计划无法报销医生开具给他们的某一款处方药。

虽然帕金斯很感激GoodRx让她终于负担得起这些药物,但她的心情依然五味杂陈。今年2月,她对我说:“整个体系都出了问题,这些公司——我不知道它们是如何盈利的,但我非常确定,如果你深入研究的话,你会发现,不仅它们在攫取利益,整个私营保险行业也在攫取利益。”

从她和很多人的遭遇看,她说的一点不错。帕金斯的医保公司(以及该医保公司指定的PBM公司)虽然收了她缴纳的保费,但她却还要自己掏钱给GoodRx和另一家PBM公司。

****

那么,我们应该如何看待GoodRx,以及它在美国医疗体系中扮演的角色呢?这是一个很复杂的问题。

约翰斯·霍普金斯大学的卡莱布·亚历山大深入研究了“药价抵消”的问题——比如GoodRx的优惠券。他发现,消费者节省下来的钱,主要集中在相对少量的非专利药上。抵消的费用相对来说也并不高——大约是每笔交易16美元,但它平均为用户节省了约40%的自付费用。虽然他担心这种价格采购可能会营造一种碎片化的环境,让慢性病患者难以持续、稳定地获得药品,但还是要肯定它的优点。

他表示:“这些类型的折扣,最终会给消费者带来很大的转变。”

就连密歇根大学的价值型保险设计中心的主任、内科医生马克·芬德里克,也在自己办公室的电脑旁边放了一叠GoodRx的优惠券,以便那些付不起基本药品费用的病人使用。他对美国的医保体系有清醒的认识,他指出,GoodRx“是一个证明了整个定价、报销、分配系统有多混乱的经典案例。”在这个体系得到修正前,他支持病人通过GoodRx或其他形式的辅助手段(例如众筹捐款等等)获得必需的药物。

最近,他就通过这款应用程序为他生病的宠物犬贝拉购买了60片西地那非,GoodRx让省下了整整720美元,他自己只支付了33美元——折扣高达95%。他还表示,如果他肯去城市另一边的另一家药店,他还可以再省一些钱。

南加州大学的乔伊斯也认为,GoodRx为那些负担不起基本药品的人提供了一条活路。不过对于那些已经购买了医保的消费者,GoodRx的作用比较难以评估,它对美国消费者总体医疗出支出的影响也同样难以评估。

乔伊斯说:“它们不是圣人,它们这样做是为了赚钱,而且它们的生意也是非常有利可图的。”

虽然GoodRx为人们提供了大量的药价数据,但乔伊斯认为,GoodRx并未让整个医疗体系变得更加透明。“它们没有带来更高的透明度,它们的价格仍然高于采购成本,它们并没有把价格压低到边际成本。”

此外,乔伊斯等人也不相信GoodRx真的像它声称的那样为消费者节省了那么多钱。

马里兰大学药学院的副教授乔伊·马丁利认为,在宣传替消费者省钱上,GoodRx用了和PBM公司相同的数学花招——即假定一名消费者如果没有使用GoodRx的优惠券,他就会按照最高的价格买药。(从GoodRx公司对相关数据的解释看,马丁利的怀疑很有可能是正确的。)

尽管如此,马丁利还是认为,GoodRx能够给消费者带来很有意义的转变,尤其是对那些没有医保的人。

不过站在GoodRx的角度,赫希认为,为消费者节省250亿美元还是一种保守的说法。

“我认为在确保病人按时用药、使病人尽量少去急诊等方面,我们的实际影响还要大得多。有了GoodRx,消费者可以支付全部的处方药费用,所以保险公司、付款人和政府的负担都会有所减轻。”根据该公司的分析,它已经让2200多万美国人买得起药了。

乔伊斯并未把“不透明”的帽子扣在GoodRx头上。他说:“它突显了药品供应链的浪费和低效,以及药价的低透明度。而PBM公司才是真正的罪魁祸首。”

2018年,《美国医学会杂志》发表了乔伊斯和他的同事的一篇研究。研究发现,在22%的情况下,消费者对处方药的共付费用超过了药品本身的成本。换句话说,患者并非是“共付”,而是“过度支付”了药价。从中得利的恰恰是PBM和保险公司。

更过分的是,直到最近,很多药店还在以合同的形式,禁止药剂师提醒医保病人他们支付的金额可能超过了药品的现金价格(也就是没有医保的病人支付的价格)。

从一些独立药剂师(比如独立药店Madden’s的老板小唐恩·皮拉)的角度看,GoodRx的优惠券,只是PBM公司从药店割肉的另一种方式。

他表示,Madden’s药店的现金价格往往比GoodRx上的价格更加优惠,不过它不会出现在GoodRx的应用程序上。但当消费者使用优惠券时,PBM公司会收取一笔“高额费用”,然后向药店报销一个较低的金额,有时甚至会低于药品的成本。不过即使赔钱卖药,它也必须兑换GoodRx的优惠券,因为它跟相关的PBM公司有协议。

作为一家小药店,和其他独立药房一样,当与强大的PBM公司谈判的时候,Madden’s是没有什么话语权的。而不与PBM打交道则根本不现实。

皮拉也认为,GoodRx提供的折扣,确实可以帮助消费者买得起他们所需的药品。只不过,GoodRx提供给消费者的只是一个“更好”的价格,而并非“最好”的价格。(不过赫希表示,GoodRx“专注于为消费者提供最好的价格。”)

皮拉说:“它们其实什么也没有做。它们没有实际销售一种产品,也没有给病人打电话,给他们提供咨询服务,也没有告诉病人如何用药。它只是做了一个算法,就能够净赚几亿美元,这意味着什么?”

赫希认为,GoodRx不仅仅是一种算法——该公司也一直在扩展其他业务,包括远程医疗,和所谓的“制药商解决方案”。这也是一项高增长、高利润的业务。GoodRx会让各大药物品牌的制药商与在其平台上搜索药品的消费者建立联系。该公司还提供了GoodRx Gold和Kroger Rx省钱俱乐部等会员服务,会员可以享受到比应用程序更优惠的药价。该公司还发布了药品价格研究报告,并就改善药品行业生态,提供了一些最清晰的、最有利于消费者的见解。

去年11月,在亚马逊宣布启动自己的药品优惠计划后,GoodRx的股价出现了短暂的下跌。不过GoodRx的高管表示,从业务上看,GoodRx对亚马逊的进入并没有什么可以担忧的。(另外,消费者还能够在亚马逊的药店使用GoodRx的优惠券。)

德意志银行网络证券研究部的总经理劳埃德·沃姆斯利和瑞士信贷的分析师杰伦德拉·辛格等分析师也认为,GoodRx的业务当前面临的威胁是被夸大了的。

赫希表示,他认为公司业务面临的最大障碍,是很多老百姓仍然不了解药价背后的猫腻,不了解自己本可以享受到更优惠的价格,仍然像以前一样购买处方药。

赫希对我说:“我们最大的竞争对手,就是那些不知道本来能够获得更优惠的药价的美国人。”他希望GoodRx品牌可以成为美国消费者最信赖的伙伴。

很多第一次使用GoodRx的人——比如上文提到的怀特和艾利森,都给出了几乎不可思议的评价,认为GoodRx“好得难以置信”。他们能够相对轻松、简单地在药店完成购买,而且药价还很便宜。在买药的过程中,人们没有医保卡也可以享受同样的服务,而且不用考虑共付、自付、PBM和医保这些糟心事。

当然,美国医疗行业的这些糟心事和种种深层问题仍然存在。GoodRx只是一家让你忘了这些问题的中间商。(财富中文网)

译者:朴成奎

Brad White has taken esomeprazole, the generic version of Nexium, to treat his acid reflux, for years. A retired school administrator living in Southlake, Texas, White has insurance, and so when he drove through his local CVS to pick up the prescription earlier this year, he was shocked when the clerk told him he owed $490 for a three-month supply.

He wasn’t quite sure what he had paid before—he’d been receiving the prescription by mail and had set up automated payments—and he knew the pills would cost him more until he met his $3,000 deductible. But paying nearly $500 for a few months of a generic drug just struck him as outrageous. He drove off without his prescription, to “regroup.”

White went home and started googling terms like “cheaper drug prices.” He soon came across GoodRx, the drug discount company, and a coupon that entitled him to get a one-month supply of the medication, without his insurance, for $17 at a nearby Kroger. “I thought, ‘This is not going to work,’” he recalls. “It absolutely worked.”

He recently used the app for another prescription, which with his insurance would have cost him $36 for a month’s supply. Using GoodRx, he could buy it for $16.60, and so he did. White knows that spending the money out-of-pocket means he’s not contributing toward his deductible and that in the long run he’s losing out on the full benefit of his insurance. But he’s okay with that tradeoff. “When it's such a huge gap, the math tells you don't use your insurance for this. I think it's pretty bizarre, honestly.” In chatting up his CVS pharmacist, White was surprised to learn that not only does the chain accept GoodRx coupons, but the pharmacist himself uses them to get his own asthma medications for a more affordable price.

When I spoke to White earlier this year, he was in a happy state of disbelief over his GoodRx discounts—if mystified by how the whole thing works. “My question becomes, How long is this going to last?” says White. “Because somebody is making money and somebody is losing money, and I can't figure out who’s who.”

You can understand the confusion. White is just one of the roughly 5.6 million Americans who use a GoodRx discount to purchase their prescription medications every month. The company’s free app, which shows what prescription drugs cost at various retailers and provides coupons for those rates, is one of the most downloaded medical apps in the iTunes and GooglePlay stores; its website has more than 18 million monthly visitors. The company’s service is beloved by consumers, widely promoted by physicians, and even touted by outlets like ProPublica, the New York Times, and yes, Fortune, which in 2019 put GoodRx on our Change the World list.The company enjoys a “net promoter score,” or loyalty rating, that is practically off the charts at 90. (By comparison, Apple’s last known NPS is 47, Walgreens's is 25, and Facebook’s, –21.)

The reason for the enthusiasm is clear: The company claims to have saved Americans more than $25 billion on prescription drugs since 2011—and, since 2019, at a rate of more than $20 million every day. That’s heroic in a country where about 58 million people go without the medications they need because of cost—and an estimated 10,000 die every month for lack of them.

Of course, GoodRx is a business, and it turns out saving Americans bundles of money on their medications is a darned good business. The company took in $550.7 million in revenue last year. That’s 42% more than in 2019—recorded, even more strikingly, in a year when a global pandemic depressed use of health care services and, as a result, the number of prescriptions written. (According to IQVIA, the health data firm, prescriptions declined 3% in 2020.) The company has proved profitable too; net income in the first half of 2020 increased 75%, to $55 million, from the previous year. (GoodRx recorded a $294 million loss for the whole year, because of the costs of its IPO.)

The Street believes in GoodRx’s counterintuitive business model too. The company’s IPO in September was one of the 20 largest last year, with a deal size of $1.14 billion, and the business currently enjoys a market value of $15.8 billion.

The company—and some analysts, too—like to say, with GoodRx, everyone wins: Consumers can afford their medications, saving money and bettering their health; providers and insurers gain patients who are more likely and able to take their meds as prescribed; and manufacturers, drugstores, and the pharmacy benefit managers (which manage drug claims for insurers), gain revenue on prescriptions that, at a higher price, may have been abandoned at the checkout. (Pharmacies pick up nondrug sales that come with foot traffic too.) But the biggest winner of all, of course, is GoodRx, which in just over a decade has managed to carve out this benign-seeming role and insinuate itself—as yet another middleman—into this deeply entrenched, thickly padded corner of American health care.

*****

GoodRx would not exist without the byzantine structure that currently dictates how much Americans pay for their prescription medications. “They found a good way to build a business in a fairly dysfunctional drug pricing ecosystem,” says Caleb Alexander, a professor of epidemiology and medicine at Johns Hopkins.

Adam Fein, an expert in pharmaceutical economics and drug distribution and the CEO of the Drug Channels Institute, put it more bluntly in a tweet reacting to GoodRx’s striking 2020 results: “Wow. #Pharmacy benefits are broken.”

GoodRx co-CEO and cofounder Doug Hirsch doesn’t entirely disagree. “To some extent,” he told me last fall, “our success is a barometer of how broken the health care system is.”

That market dysfunction is key to GoodRx’s origin story, which dates back to 2010 when Hirsch experienced his own round of sticker shock at a local pharmacy after learning that he owed $500 for a prescription. Hirsch had insurance and expected the cost to be a tiny fraction of that. So he went to a pharmacy across the street, where he was surprised to learn that there, the price was $300. At yet another area pharmacy, the cost was $400. At that point Hirsch too walked away, only to be chased down by the pharmacist, who was willing to negotiate.

“It kind of broke my brain,” Hirsch has said of the experience. An early employee at Yahoo and Facebook, where he was one of the conceivers of photo tagging, Hirsch had a front-row view as the digital revolution brought transparency and ease to industries from air travel to homebuying. He regarded the opaque and bewildering marketplace of prescription drugs—with its many middlemen and prices—as a worthy and overdue target for disruption, and so he and his co-founder Trevor Bezdek began the decade-long project that is GoodRx.

By Hirsch’s telling, it began as a curiosity-driven journey simply to make sense of drug prices. “To be honest, I didn’t know what a PBM [pharmacy benefit manager] was when we started this process,” says Hirsch. He and cofounders began collecting information: Costco published its drug prices on its website, and Walmart sold a handful of prescription meds for $4. Some states had laws on the books—requiring prices be disclosed online, or at the pharmacy—aimed at providing transparency, but those tools didn’t work well. “It was just a total mess,” he told me last fall.

Hirsch and his team started calling up pharmacists and reaching out across the health care landscape for help. In those early days of the Affordable Care Act, there were plenty of people who didn’t think the effort would be worth the time. They thought the system was either fixed or impossible to disrupt. But enough of them did, including an employee at the PBM MedImpact, which eventually became one of GoodRx’s first partners. “Doors always opened for us,” Hirsch says.

In time, the team had cobbled together enough price information for its data scientists to unravel the complex contracts—between PBMs and pharmacies—that set those rates. They found (as have plenty of researchers) that prices varied widely, particularly on low-cost, frequently prescribed generic drugs. Understanding the inner workings of the prescription med marketplace was a big, hairy data engineering problem, and GoodRx had cracked it.

By 2011, the company had a website and a product: a simple digital tool that in clearly displaying the cost of prescription meds at various outlets, could guide consumers to the most affordable purchase. Over time, the company’s data set has gotten more sophisticated and complete. GoodRx now gets information from virtually every PBM, among other sources, and aggregates over 200 billion price points per day in its system, says Hirsch.

Simply making price comparison and price shopping possible was something of a breakthrough in the industry, says George Hill, managing director of health care technology and services equity research at Deutsche Bank, who notes that Americans, on average, fill 11 prescriptions a year. “[GoodRx] is really the first broadly accepted and broadly used price transparency tool that exists in health care.”

*****

So how exactly does GoodRx work—and perhaps more importantly, how does it make money? To grasp the intricacies of the company's business model, you must understand the economic ecosystem in which pharmacies operate. Unfortunately, like so many aspects of American health care, it's a landscape that defies easy or rational explanation. It consists of many players, mostly middlemen, all vying for a piece of a $509 billion pie, which gets sliced and diced according to obscuring jargon and business practices like rebates, clawbacks, and co-pays. For the uninitiated, trying to track where the money spent on prescription drugs goes is like an especially mind-numbing and complicated follow-the-ball trick.

Chief among these players, and key to GoodRx’s story and success, are pharmacy benefit managers, or PBMs, a class of companies that originated in the 1960s to process prescription drug claims for insurers. They still do that, but over time these entities have assumed an ever-more-powerful and lucrative intermediary role in America’s prescription drug marketplace. As the go-between for insurers, manufacturers, and pharmacies, PBMs negotiate how much insurers will pay drug manufacturers, what consumers owe at the pharmacy, and how much pharmacies will be reimbursed. They also develop the formularies that determine which medications your insurance will cover; deploy “utilization management” tools, like prior authorizations, to ensure your prescription is medically necessary; and operate mail-order pharmacies, among other things. The aim of all these activities and the PBM’s stated reason for being these days is, ostensibly, to keep drug spending in check for health plans.

How well they’ve done that is a matter of intense debate. In recent years, the $402 billion industry has just as often been accused of doing the opposite through its opaque, middleman business practices. PBMs, the three largest of which have all been absorbed by major insurers in the past decade (Cigna’s Express Scripts, CVS’s Caremark, and UnitedHealth’s Optum), have cultivated a number of revenue streams over the years. But for this story, suffice it to say, they make money when they process a claim at the pharmacy. This is where GoodRx enters the picture.

For the sake of this story, we’re focusing on the market of low-cost generic drugs, which is where GoodRx provides consumers the most savings and where it makes most of its money.

Normally, when you go to the pharmacy to pick up a prescription, what you owe depends on a few factors: (1) your health plan or insurance, (2) the pharmacy benefit manager, or PBM, that your health plan has hired to manage drug costs, and (3) the pharmacy where you have chosen to fill the prescription. What you will pay is determined by the rate negotiated between that pharmacy or chain of pharmacies and your health plan’s PBM. If you don’t have insurance, you will be charged that pharmacy’s cash price, which is often very steep.

This is why, as Hirsch discovered, the price of a medication can vary so widely, pharmacy to pharmacy, and person to person. “If you have 10 people that stand in line at a McDonald's, all 10 people pay the same price for a Happy Meal. It doesn't matter if you pay cash, or with a credit card. It doesn’t matter who you are. But in health care, and also in pharmacy, if you have 10 people that stand in line to get their blood pressure medication filled, 30 tablets, all 10 people are going to either pay a different price, or their insurance is going to pay a different price,” says Don Piela Jr., the head pharmacist and owner of Madden’s, an independent pharmacy in Elberton, Ga., who calls the system “ridiculous.” Worse, he adds, “there’s no transparency.”

Indeed. Those are the very bugs in the system around which GoodRx has astutely built its product—illuminating a whole range of prices that have been negotiated between PBMs and pharmacies and allowing consumers to access any of them through GoodRx coupons.

GoodRxis able to monetize the discounts, somewhat ironically, through its partnership with the various PBMs. When a consumer seeks out a lower-price medication at a particular pharmacy with a GoodRx coupon, the PBM with that contracted price processes the claim and rewards GoodRx with a sort of “referral fee,” explains Hirsch. (These fees account for 90% of GoodRx’s revenues.) It can be a sweet deal for PBMs in that they’re able to elbow their way in and pick up revenue on transactions that they previously had no part in.

“[GoodRx] is kind of a front for PBMs,” explains Geoffrey Joyce, a health economist and director of health policy at the University of Southern California’s Schaeffer Center. “They provide the benefits a PBM might provide for uninsured consumers.” Those benefits can be substantial. “Uninsured consumers, they’re a big cash cow for pharmacies,” says Joyce. “They pay ridiculously high prices [for generic drugs].”

GoodRx is not the first company to pursue this strategy. Drug discount cards, offering consumers a more affordable PBM-network rate for their meds, have been around for decades. But GoodRx’s offering is both far more robust and sophisticated than predecessors. Rather than working with just a single PBM, GoodRx partners withmore than 12 of them, accessing all their network rates and so, a much broader range of discounts. (The company also offers a slick tech platform to search out those savings and a sizable marketing budget to promote them.) “More often than not, they’ll have a very good price,” says Lloyd Walmsley, managing director of Internet equity research at Deutsche Bank.

For people like Katie Rae Allison, a jewelry store manager and designer in Gillette, Wyo., that’s a real service. She was diagnosed with thyroid disease as a child and takes medication daily to manage her condition; without it, her health suffers. She doesn’t have insurance through her job and so was relieved—but also skeptical—when she discovered GoodRx’s app earlier this year. “It seemed too good to be true,” she told me. But she tried it and got a 90-day supply of medication for $25; without the coupon, she would have been charged $32 for a month’s worth. “That’s three months’ worth for less than what I would have paid for a month,” she says. “In a year’s time, that saves me a lot of money.”

Uninsured individuals like Allison make up just a fraction of consumers using GoodRx discounts to save on prescriptions, though. According to the company, 75% of their users have some form of insurance (that includes through a government program like Medicare).

When these customers use a GoodRx coupon to get a prescription at a more affordable rate, they’re not using their insurance—and so the PBM with the lowest contracted price at the pharmacy and GoodRx captures the revenue from the transaction, rather than the PBM that works with that individual’s health plan.

Why are so many people choosing to pay out-of-pocket with GoodRx, instead of using their hard-earned health benefits? Many are in a situation like the one faced by Brad White—even with insurance, they’re paying a hefty price for prescriptions. That has a lot to do with a recent shift by many employers to high-deductible health plans, which require users to pay at least $1,400 out-of-pocket before their coverage kicks in. (Over the past decade, the average deductible for an individual has increased 111% from $917 to $1,644, according to the Kaiser Family Foundation.) The thinking behind these plans was that they would make employees more careful, cost-conscious consumers of health care. In reality, that’s hard to do, and many people get stuck with big health bills they can’t afford. Studies show that people on high-deductible plans are more likely to delay or forgo care.

GoodRx can save insured consumers from this short-term financial stress, but it comes with a tradeoff: By paying out-of-pocket, they’re not paying toward their deductible, which will delay or possibly prevent them from ever realizing the benefits of their insurance—on which they and their employers are paying considerable monthly premiums. (According to the Kaiser Family Foundation, the average insurance premium for single coverage was $7,470 in 2020; for a family, it was $21,342.) GoodRx payments also don’t count toward an individual’s out-of-pocket maximum, another reason why LeemoreDafny, a professor at Harvard Business School, worries that people with insurance who use GoodRx may, in some cases, end up spending more overall. (On its site, GoodRx offers instructions—including how to submit receipts and fill out insurance forms—for people who want to attempt to have their out-of-pocket GoodRx payments count toward their deductible, but the company doesn’t many any promises. Says a spokesperson, “You most likely won’t be reimbursed, but you can always try.”)

But insured consumers aren’t always just looking for a better deal. Some, like Yayra Perkins, a middle school math teacher in Worcester, Mass., turn to GoodRx when insurance bureaucracy impedes care.

Perkins, a 33-year-old mother of two, enjoyed a full and active life until late 2019, when she began to experience the odd and debilitating symptoms of systemic scleroderma, the rare autoimmune condition she was diagnosed with in early 2020. While not life-threatening, systemic scleroderma, like other autoimmune disorders, is not well understood, and it’s not curable.

Doctors do their best to treat those who suffer from it with a battery of sometimes-effective medications that were originally developed for other conditions. Perkins’s doctors prescribed her a handful of things they hoped might work to tame the disruptive and painful flare-ups she experiences multiple times per day: immunosuppressants, blood pressure and acne medications, face creams, Botox, and even generic Viagra (sildenafil).

Perkins’s insurer initially denied coverage of many of these medications, presumably because they’re not designated as treatments for her condition, leaving her to pick up the tab of her treatment while she and her physician pursued the weeks- or months-long appeals process. The cost for a 90-day supply of sildenafil, which helps alleviate debilitating circulation issues she suffers in her hands, was $1,363.89; with the GoodRx coupon her doctor pointed her to, she paid $19.37.

Perkins is not alone. A survey by NPR, the Robert Wood Johnson Foundation, and the Harvard School of Public Health last year found that more than a third of American adults, and nearly half of low-income adults, had been told their health plan would not cover a drug prescribed to them, or a family member, by a doctor.

Though grateful that GoodRx’s discount made that medication affordable for her, she doesn’t feel good about it. It feels like a racket. “The whole system—it’s not right,” she told me in February. “The fact that these companies—I don't know how they're making their profit, but I'm pretty sure that when you dig underneath their process…somehow not only they are benefiting, but the private insurance industry is benefiting as well.”

In her case, and many others, she’s not wrong. Perkins’s health plan (and the PBM it hired to manage pharmacy benefits) are collecting her premium payments; meanwhile she’s spending her own money on a prescription to the benefit of GoodRx and another PBM.

*****

So how should one think about GoodRx and the role it plays in American health care? Well, it’s complicated.

Caleb Alexander of Johns Hopkins has studied drug price “offsets,” including the ones provided by discount coupons like those from GoodRx. He found the savings were concentrated on a relatively small number of generic drugs, and that the offsets, while relatively small—about $16 per transaction—save the average customer about 40% of the out-of-pocket cost. While he worries a bit that price-shopping for medications could create a piecemeal environment that makes it hard, especially for patients with chronic illness, to have consistent access to medication, he sees the benefit. “These types of discounts can ultimately make a big difference for consumers,” he says.

That’s why Mark Fendrick, an internist and director of the Center for Value-Based Insurance Design at the University of Michigan, keeps a stack of GoodRx coupons next to his office computer for patients who can’t afford their essential medications. He’s not wild about the system it serves; he calls GoodRx a “classic example of how chaotic the whole pricing, reimbursement, and dispensing system is.” But until the system is fixed, he’s in favor of patients using GoodRx or other forms of assistance (better than bake sales or Kickstarter campaigns, he says)to get clinically necessary medications. He recently used the app himself to fill a prescription of sildenafil—generic Viagra—for his ailing dog, Bella. GoodRx saved him from spending $720 on 60 tablets of the drug. Instead, Fendrick paid $33—a 95% discount—and notes he could have gotten the medication for even less at a pharmacy across town.

USC’s Joyce agrees GoodRx is providing an important, potentially even lifesaving service for people who can’t afford medications, but he says the benefits are harder to parse for the insured, and that the company’s effect on overall spending is hard to know. “They're not saints,” says Joyce. “They're doing this to make money, and they are very profitable given what they do.”

Though GoodRx has made drug price data more available, Joyce dismisses the idea that the company has made the system more transparent. “They’re not bringing transparency. They’re still charging a price that’s above the acquisition cost,” he says. “It’s not as if they’re driving the price down to the marginal cost.”

He and many others also don’t believe GoodRx has saved people as much as it claims. Joey Mattingly, an associate professor with the University of Maryland School of Pharmacy, suspects GoodRx uses the same fantastical math that PBMs do in making savings claims—assuming that everyone who doesn’t use a GoodRx coupon would pay the highest possible cash price rate. (The company's own explanation of how it arrives at its savings figures suggests he's likely correct.) Still, Mattingly thinks GoodRx can make a meaningful difference, especially for uninsured customers.

For GoodRx’s part, Hirsch thinks its $25 billion savings calculation is an understatement. “I think our actual impact is much bigger in terms of improvements to adherence, ER visits, etc. With GoodRx, consumers pay the entire cost of their prescription, so there is a decreased burden on insurance companies, payers, and government.” According to the company’s analysis, GoodRx has helped more than 22 million Americans afford their drugs.

Joyce doesn’t blame GoodRx for getting in the game, though. “It highlights the waste and inefficiency in the pharmaceutical supply chain and the lack of transparency of prices,” he says. “The PBMs, they’re the real culprits in this.”

In 2018, The Journal of the American Medical Association published research from Joyce and colleagues that found that in 22% of cases, consumers’ co-payments for prescription medications exceeded the drug’s costs. In other words, patients aren’t “co-paying” for these drugs, they’re overpaying, and PBMs and insurers—which are increasingly one and the same—are profiting from it. Adding further insult, pharmacists until recently were contractually prohibited from alerting insured consumers in situations where they were paying more than the cash price (i.e., what an uninsured person would pay).

From the perspective of some independent pharmacists, including Madden’s Piela, GoodRx coupons are just another way PBMs profit off the back of pharmacies like his own. He says Madden’s cash price (which does not appear on the GoodRx app) usually beats GoodRx pricing, but when a customer does use a coupon, the PBM takes a “hefty fee” and reimburses his pharmacy a smaller amount than it would otherwise, sometimes less than the drug’s cost. Even when it's a losing proposition, he’s contractually bound to honor GoodRx coupons because he has agreements with the PBMs that process the claims.

Madden’s, like other independent pharmacies, has little clout when it comes to negotiating with powerful PBMs—and walking away from them is not an option. He acknowledges that discounts, including those provided by GoodRx, can help his customers afford drugs they need. But he takes offense to the portion of the pharmacy pie GoodRx is getting for providing consumers a better—but not always the best—price. (Hirsch says GoodRx is “focused on getting the consumer the best price, period.”)

“They’re not doing anything. They're not dispensing a product, they're not calling a patient and giving them counseling, they're not telling them how to use their medication,” Piela says. "I mean, if you're getting hundreds of millions of dollars for just being an algorithm? What does that mean?”

Hirsch sees GoodRx as more than an algorithm—the company has been expanding into other businesses including telehealth and “manufacturer solutions,” a high-growth, high-margin business that connects makers of branded pharmaceuticals with consumers searching for the drugs on the GoodRx platform. The company offers GoodRx Gold and Kroger Rx Savings Club, subscription services that promise members even better deals on drugs than they’d get with the app. It alsopublishes research on drug prices, and some of clearest, most-consumer friendly explainers on the dysfunctional pharmaceutical ecosystem.

While the company’s stock briefly plummeted in November after Amazon announced it was starting its own pharmacy discount program, GoodRx’s executives argue that when it comes to their business, the Everything Store is nothing to worry about. (Among other reasons: You can use a GoodRx coupon at the Amazon pharmacy.) Analysts like Walmsley and Credit Suisse’s Jailendra Singh also think that the current threat to the company’s business is overblown.

Instead, Hirsch says he considers his bigger obstacle to be the uninformed public, who, oblivious to price variation and the better deals they could be getting, continue to purchase their prescriptions like they always have. “Our biggest competitors are Americans who don’t know any better,” Hirsch told me. He aspires for the brand to become the American consumer’s most trusted partner.

It’s true that many who use GoodRx for the first time, like White and Allison, describe the experience in almost magical terms. “It’s too good to be true,” they think, before being completely delighted by a relatively pleasant, easy, inexpensive interaction at the pharmacy. In the exchange, they don’t have to dig out an insurance card, or think about co-pays, deductibles, PBMs, or health plans—all the things that make American health care so miserable. Of course, that stuff and all the dysfunction are still there in the background. GoodRx is just the middleman that lets you forget it.

请打开财富Plus APP