科尔氏百货押宝这一行业摆脱停滞不前

王波非(Phil Wahba)

2020-10-23

这家公司的首席执行官表示,科尔氏百货的门店及品牌将焕然一新,运动休闲将成为核心业务。

文本设置

文本设置

Plus(0条)

Plus(0条)

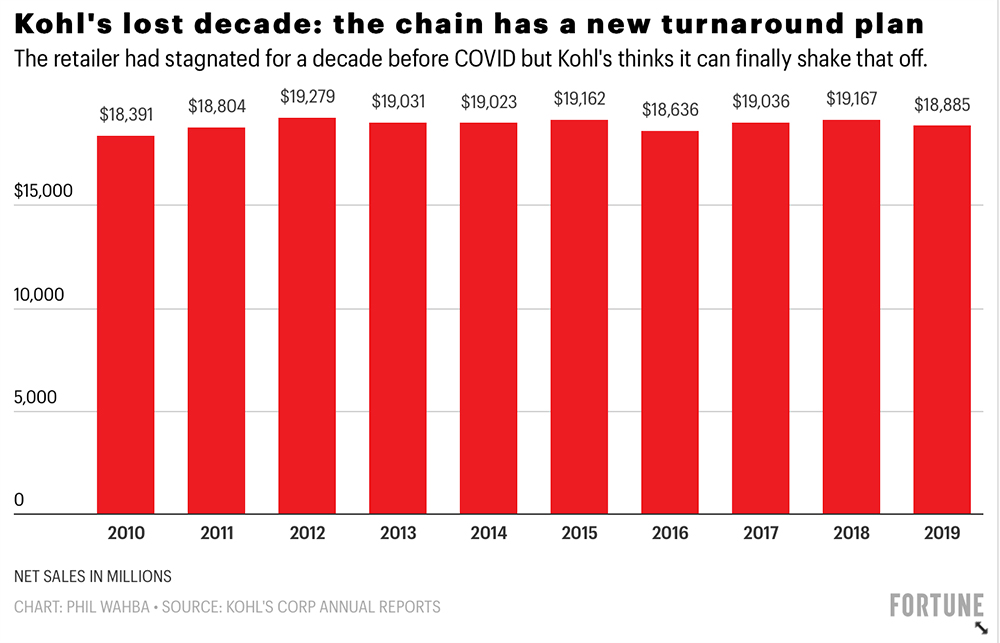

多年来,科尔氏百货(Kohl’s)的业务成长一直停滞不前,为了解决这一问题,该公司重新准备了一份面向华尔街的重整方案,孰料不久之后就碰上了新冠肺炎疫情大爆发。

受3月中旬爆发的疫情影响,科尔氏百货门店被迫停业数周之久,不但令其增长提振方案化为泡影,上半财年销售额更是下降了33%,瞬间陷入经营危机之中。

当前,虽然该公司的业务远未恢复到疫情爆发前的水平,不过也已经逐渐企稳,科尔氏百货也随之公布了自己的重整方案,即将业务重心从发展不利的时尚领域转向运动服装。根据该方案,科尔氏百货将加大耐克、TOMS等国民品牌及Lands’ End、Cole Hann等新进合作伙伴在其业务矩阵中的分量,并剥离多个自有品牌。

科尔氏百货的首席执行官米歇尔•加斯在接受《财富》杂志采访时说:“科尔氏百货的门店及品牌将焕然一新,运动休闲将成为我们的核心业务。”

服装零售是本次疫情中受影响最大的行业之一。而在其它百货公司、服装专卖店饱受冲击之时,耐克、安德玛、阿迪达斯等运动品牌让科尔氏百货的业绩得到了一定保障。2013年加斯加入科尔氏之后,十分明智地加大了对运动品牌的投入。目前,科尔氏百货有20%的收入来自运动服饰,加斯认为这一比例可能还会进一步提高到30%。

新冠疫情对科尔氏百货的部分竞争对手造成了沉重打击,比如门店主要集中在购物中心中的彭尼百货(J.C. Penney)已经申请破产保护,梅西百货(Macy’s)也同样损失惨重,不过其它竞争对手的情况要好得多,这也增加了科尔氏百货恢复增长的压力。

由于95%的门店都开在购物中心之外,科尔氏百货的损失不像彭尼和梅西百货那么大,不过作为一家主要布局商业街区的连锁百货,科尔氏百货也面临着来自塔吉特(Target)、Ulta Beauty、Dick’s Sporting Goods和T.J. Maxx等强大对手的激烈竞争。

以Gap Inc旗下的Old Navy为例,该服装品牌在美国年轻母亲及其它消费群体中与科尔氏有直接竞争关系,其销售额下降幅度便远小于科尔氏百货,塔吉特的服饰及家居用品销售额甚至还有所增长。

面对这种局面,科尔氏百货不得不重新思考自己的商品策略,想办法吸引消费者。虽然科尔氏并非唯一一家销售运动休闲产品的企业,但其所提供的产品除着眼于女性消费者,还能够满足全家人的需要,这也让其开辟出了一个新的细分市场。加斯表示:“我们有能力占领这个市场。”科尔氏百货也在尝试一些新思路,比如在50家门店销售个人护理产品。加斯补充道:“新的思路可能行得通,也可能行不通,我们在通过推广运动休闲的生活方式来拓展自己的业务边界。”

多年以来,科尔氏百货一直大力发展自有品牌,原因是自有品牌更容易控制,利润率更高,理想情况下也能够满足顾客的需求,不过缺点则是无法推向更多的销售渠道。科尔氏百货的问题在于有太多的自有品牌已经过时,尤其是在服装领域。与其形成鲜明对比的塔吉特,总能迅速推出对消费者充满吸引力的全新品牌。

截至目前,科尔氏百货已经放弃了JLO、Rock&Republic、Dana Buchman等8个自有品牌,虽然该公司还在引入更多像Lands’ End、Cole Haan这样国民品牌,但未来还会有更多的自有品牌退出市场。现在,科尔氏百货有37%的销售额来自服装等品类的自有品牌,而就在几年之前,这一数字甚至超过了50%。在谈到品牌线收缩时,加斯说:“我们将会把更多的精力集中到更少的品牌上去。”

美妆行业的呼唤

自从将美妆市场拱手让给梅西百货和彭尼百货(丝芙兰专卖店的所在地)之后,科尔氏百货多年以来一直试图重新成为该领域的重要参与者。实际上,早在2014年的“伟大议程”之中,科尔氏百货就将打造规模化的美妆业务作为自己的核心,希望能借助所谓“美妆看门人”计划在短期内将美妆业务在总销售额中的占比从当时的2%提高到5%。虽然科尔氏百货的香水业务表现不俗,但由于同在购物街区开展业务的塔吉特、Ulta Beauty、CVS、沃尔格林(Walgreens)等公司或激烈或温和的竞争,其美妆业务始终未能达到预期的高度。

现在,科尔氏百货计划将其美妆门店的规模扩大两倍,并为门店配备专业的美妆顾问。多年来,科尔氏百货一直探索着如何让匆匆而过的顾客增加在店逗留时间,而美妆品类恰是解决这一问题的关键。

持续发展电商业务也是该公司计划的重要一环。疫情爆发前,线上购物在总销售额中的占比还不到四分之一,而在疫情高峰期,这一数字达到了40%之多。预计,最终电商业务在销售总额中的占比将会回落到25%至40%之间的某个位置。

店内方面,科尔氏百货将会大幅减少某些品牌的商品品种,幅度可达40%。该公司将会减少手提包、高级珠宝、男士西装等销售下滑的产品,为销量更好的产品腾出库存空间。

加斯说:“这样可以提升我们的灵活性,让我们能够将更多资源投入那些持续成长的品类之中,尝试、学习、迭代,优胜劣汰。”也希望公司可以借此实现长期以来渴望的增长。(财富中文网)

译者:梁宇

审校:夏林

多年来,科尔氏百货(Kohl’s)的业务成长一直停滞不前,为了解决这一问题,该公司重新准备了一份面向华尔街的重整方案,孰料不久之后就碰上了新冠肺炎疫情大爆发。

受3月中旬爆发的疫情影响,科尔氏百货门店被迫停业数周之久,不但令其增长提振方案化为泡影,上半财年销售额更是下降了33%,瞬间陷入经营危机之中。

当前,虽然该公司的业务远未恢复到疫情爆发前的水平,不过也已经逐渐企稳,科尔氏百货也随之公布了自己的重整方案,即将业务重心从发展不利的时尚领域转向运动服装。根据该方案,科尔氏百货将加大耐克、TOMS等国民品牌及Lands’ End、Cole Hann等新进合作伙伴在其业务矩阵中的分量,并剥离多个自有品牌。

科尔氏百货的首席执行官米歇尔•加斯在接受《财富》杂志采访时说:“科尔氏百货的门店及品牌将焕然一新,运动休闲将成为我们的核心业务。”

服装零售是本次疫情中受影响最大的行业之一。而在其它百货公司、服装专卖店饱受冲击之时,耐克、安德玛、阿迪达斯等运动品牌让科尔氏百货的业绩得到了一定保障。2013年加斯加入科尔氏之后,十分明智地加大了对运动品牌的投入。目前,科尔氏百货有20%的收入来自运动服饰,加斯认为这一比例可能还会进一步提高到30%。

新冠疫情对科尔氏百货的部分竞争对手造成了沉重打击,比如门店主要集中在购物中心中的彭尼百货(J.C. Penney)已经申请破产保护,梅西百货(Macy’s)也同样损失惨重,不过其它竞争对手的情况要好得多,这也增加了科尔氏百货恢复增长的压力。

由于95%的门店都开在购物中心之外,科尔氏百货的损失不像彭尼和梅西百货那么大,不过作为一家主要布局商业街区的连锁百货,科尔氏百货也面临着来自塔吉特(Target)、Ulta Beauty、Dick’s Sporting Goods和T.J. Maxx等强大对手的激烈竞争。

以Gap Inc旗下的Old Navy为例,该服装品牌在美国年轻母亲及其它消费群体中与科尔氏有直接竞争关系,其销售额下降幅度便远小于科尔氏百货,塔吉特的服饰及家居用品销售额甚至还有所增长。

面对这种局面,科尔氏百货不得不重新思考自己的商品策略,想办法吸引消费者。虽然科尔氏并非唯一一家销售运动休闲产品的企业,但其所提供的产品除着眼于女性消费者,还能够满足全家人的需要,这也让其开辟出了一个新的细分市场。加斯表示:“我们有能力占领这个市场。”科尔氏百货也在尝试一些新思路,比如在50家门店销售个人护理产品。加斯补充道:“新的思路可能行得通,也可能行不通,我们在通过推广运动休闲的生活方式来拓展自己的业务边界。”

多年以来,科尔氏百货一直大力发展自有品牌,原因是自有品牌更容易控制,利润率更高,理想情况下也能够满足顾客的需求,不过缺点则是无法推向更多的销售渠道。科尔氏百货的问题在于有太多的自有品牌已经过时,尤其是在服装领域。与其形成鲜明对比的塔吉特,总能迅速推出对消费者充满吸引力的全新品牌。

截至目前,科尔氏百货已经放弃了JLO、Rock&Republic、Dana Buchman等8个自有品牌,虽然该公司还在引入更多像Lands’ End、Cole Haan这样国民品牌,但未来还会有更多的自有品牌退出市场。现在,科尔氏百货有37%的销售额来自服装等品类的自有品牌,而就在几年之前,这一数字甚至超过了50%。在谈到品牌线收缩时,加斯说:“我们将会把更多的精力集中到更少的品牌上去。”

科尔氏百货“失去的十年”:零售巨头推出全新重整方案

美妆行业的呼唤

自从将美妆市场拱手让给梅西百货和彭尼百货(丝芙兰专卖店的所在地)之后,科尔氏百货多年以来一直试图重新成为该领域的重要参与者。实际上,早在2014年的“伟大议程”之中,科尔氏百货就将打造规模化的美妆业务作为自己的核心,希望能借助所谓“美妆看门人”计划在短期内将美妆业务在总销售额中的占比从当时的2%提高到5%。虽然科尔氏百货的香水业务表现不俗,但由于同在购物街区开展业务的塔吉特、Ulta Beauty、CVS、沃尔格林(Walgreens)等公司或激烈或温和的竞争,其美妆业务始终未能达到预期的高度。

现在,科尔氏百货计划将其美妆门店的规模扩大两倍,并为门店配备专业的美妆顾问。多年来,科尔氏百货一直探索着如何让匆匆而过的顾客增加在店逗留时间,而美妆品类恰是解决这一问题的关键。

持续发展电商业务也是该公司计划的重要一环。疫情爆发前,线上购物在总销售额中的占比还不到四分之一,而在疫情高峰期,这一数字达到了40%之多。预计,最终电商业务在销售总额中的占比将会回落到25%至40%之间的某个位置。

店内方面,科尔氏百货将会大幅减少某些品牌的商品品种,幅度可达40%。该公司将会减少手提包、高级珠宝、男士西装等销售下滑的产品,为销量更好的产品腾出库存空间。

加斯说:“这样可以提升我们的灵活性,让我们能够将更多资源投入那些持续成长的品类之中,尝试、学习、迭代,优胜劣汰。”也希望公司可以借此实现长期以来渴望的增长。(财富中文网)

译者:梁宇

审校:夏林

On the eve of the pandemic's outbreak in mid-March, Kohl's had a new turnaround plan it wanted to unveil to Wall Street that it hoped would finally shake years of stagnation.

But the COVID-19 outbreak, which forced Kohl's to close its stores for weeks, thwarted those plans, instead putting the retailer in survival mode as sales fell 33% in the first half of the fiscal year.

Now that business has stabilized—though far from returning to pre-pandemic levels—Kohl's is unveiling its plan, which shifts it away from fashion, where it has stumbled, and further into activewear. The plan also calls for Kohl's to lean more heavily on national brands like Nike and TOMS, as well as newer partners like Lands' End and Cole Haan, and shed many of its store brands.

"The Kohl’s store and brand is going to look and feel different," Kohl's CEO Michelle Gass tells Fortune. "Active and casual are going to be at the center of that."

Apparel spending has been one of the biggest victims of the pandemic. Shielding Kohl's from the worst of the clothing armageddon buffeting other department stores and specialty clothing chains is activewear from brands like Nike, Under Armour, and Adidas. Kohl's wisely placed a big bet on sporty apparel after Gass joined Kohl's in 2013. That category now generates 20% of Kohl's sales and Gass thinks that can hit 30%.

While COVID-19 took a hammer to the business of many Kohl's rivals— notably bankrupting mall-based J.C. Penney and decimating Macy's—other competitors have fared much better, adding to the pressure on Kohl's to finally get back to growth.

Having 95% of stores away from malls helped it avoid from much of the ravages felt by Penney and Macy's. Yet as a strip-mall based chain, Kohl's is going up against very strong competitors in Target, Ulta Beauty, Dick's Sporting Goods and T.J. Maxx.

Gap Inc's Old Navy chain, which competes directly with Kohl's for the business of young American mothers, among other demographics, saw a sales decline much smaller than Kohl's, while Target reported an increase in apparel and home goods sales.

And this has forced Kohl's to rethink its merchandise strategy and what makes it appealing to shoppers. While Kohl's isn't alone in selling athleisure, it has carved out a niche by focusing on such items for the whole family and not just women. "We can own that space," says Gass. Kohl's is also testing out new ideas, like personal care products, at 50 stores. "It may or may not work—we’re really stretching the boundaries of where we can go and take this active and casual lifestyle," Gass adds.

For years, Kohl's bet heavily on store brands, which offer higher profit margins, more control, and ideally, something customers want—but can't get elsewhere. Kohl's problem is that too many of its store brands grew stale, particularly in apparel. That weakness stands in stark contrast to Target's remarkable ability to quickly launch new brands that send consumers flocking.

Kohl's has so far ditched eight of its exclusive brands, including JLO, Rock & Republic and Dana Buchman, with more exits to come, even as it has lined up more national brands, like Lands' End and Cole Haan. The retailer now gets 37% of sales from its exclusive brands in apparel and other categories, down from more than half just a few years ago. "We will be more focused," Gass said of the paring of brands.

Beauty call

Kohl's has been trying for years to become a serious player in the beauty sector after having ceded it to Macy's and J.C. Penney, which houses Sephora shops. In fact, building a sizable beauty was a linchpin of Kohl's "Greatness Agenda" in 2014, with the company hoping beauty would grow from 2% of sales then to 5% in short order, helped by so-called "beauty concierges." While Kohl's has shown strength in fragrance, beauty has not yielded the upside the company planned on, as it has faced stiff competition from strip mall neighbors Target and Ulta Beauty, and to a lesser extent CVS and Walgreens.

Kohl's is now planning beauty shops three times the size of its current ones, staffed with beauty advisors. The category is crucial to solving a riddle that has bedeviled Kohl's for years: how to get more shoppers to come to store and indulge, rather than just popping into the store for a quick in-and-out trip.

A big part of its plan is to keep building its e-commerce business. Online shopping, which accounted for nearly a quarter of sales pre-pandemic, spiked to as much as 40% at the peak of the pandemic. Ultimately, it's expected to settle in somewhere in the middle of those two percentages.

In-store, Kohl's will reduce its assortment within some brands as much as 40%. It will shrink its offering of handbags, fine jewelry, and men's suits—areas that have seen sales decline—making space to increase inventory of healthier categories.

"That gives us the flexibility to lean into growth categories, test, learn, iterate—kill what’s not working, scale what is," says Gass. And hopefully finally yield that long elusive growth.

请打开财富Plus APP