五年大涨后,苹果的股票是否依然值得投资?

Shawn Tully

2020-07-02

由于这几年涨幅过大,未来五年,苹果投资者的回报率若能达到5%左右,就已经是吉星高照了。

文本设置

文本设置

Plus(0条)

Plus(0条)

过去五年,苹果公司(Apple)股票的业绩惊人,它就像是一列貌似势不可挡的财富快车。但这给正在考虑要不要现在登上这列快车的投资者带来了一个问题。简单来说,作为美国最伟大的企业,苹果公司的股价过高,因此未来五年,投资者的回报率若能达到普普通通的个位数中段,就已经是吉星高照了。

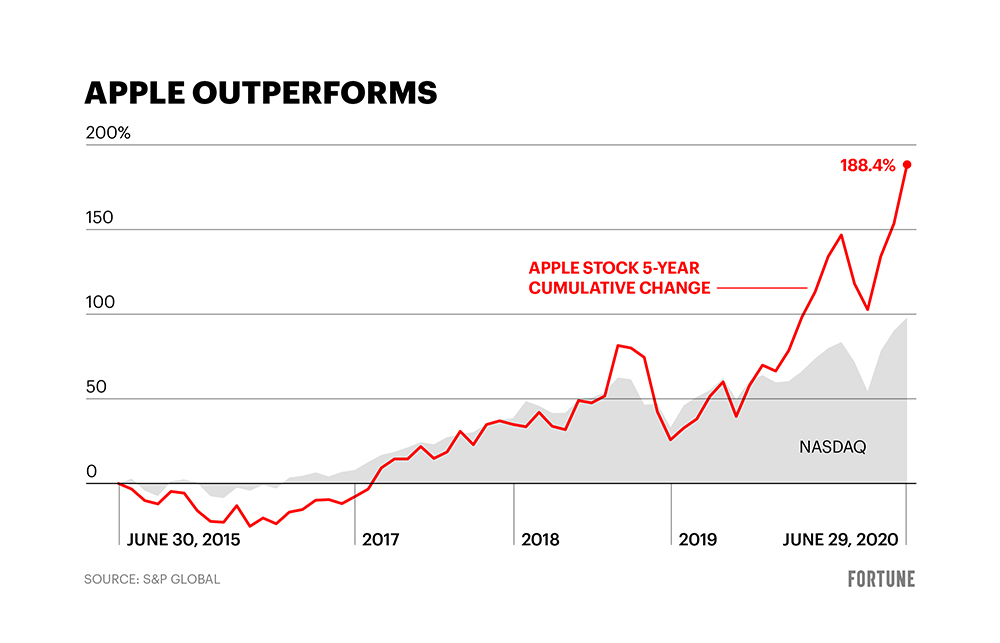

就在三个月前,新冠疫情引发的抛售潮让苹果的股价下跌30%,从历史最高的325美元下跌到2月中旬的224美元,苹果现象似乎已经难以为继。接下来的反弹则让苹果的拥趸们相信,在脱离控制的市场动量的不可抗力下,苹果公司的高股价并非不可撼动。从3月23日到6月20日,苹果股价上涨62%至362美元,打破了之前的纪录,使其市值增长6,000亿美元,相当于奈飞(Netflix)、特斯拉(Tesla)和Adobe的市值总和。此轮上涨创下了全球资本主义史上的最大市值涨幅。

苹果目前的股价远高于其过去五年大部分时间的水平,因此投资者有理由怀疑苹果股票是否仍有投资的价值?要回答这个问题,我们需要研究过去五年苹果能够给投资者带来丰厚回报的因素,以及这些因素未来继续增加回报所面临的障碍。

从2015年3月(其财年的第二季度)至今年3月,苹果的年度总收益率约为20%,其中18%来自资本收益,2%为股息。苹果之所以能给投资者提供如此丰厚的回报,并不是因为其基本面(即营收)迅速增长,而是因为其股价极低,因此进行股票回购收效显著,也为提高市盈率倍数留出了大量空间,投资者愿意通过支付这样的股价来获得收益。

2015年3月,苹果之前四个季度的营收为504亿美元,其市值高达7,580亿美元。所以其市盈率只有15。如此低的市盈率意味着在投资者眼中,该公司的总营收长期持平,甚至在不断下滑。事实上,截至2020年3月,根据最近四个季度的情况,苹果公司的净利润只增长到572.4亿美元,涨幅只有13.6%。这相当于每年只增长2.5%,跑赢通胀约1个百分点。苹果的增长并不强劲。

但苹果有一个强大的工具可以提高其每股收益。作为一台无可匹敌的“提款机”,苹果公司需要的资本投资很少,因此它能够并且依旧在把全部营收用于发放股息和回购股票。到目前为止,股票回购是苹果股价上涨最主要的推动力。在市盈率为15时,苹果用于回购股票的每1美元,可以提高每股收益6.7美分,因为与收益相比,苹果的股价极低。而且按照年平均营收约500亿美元计算,苹果公司的平均市盈率一直维持在15左右,直到2019年年中公司股价开始大幅上涨。

在过去五年的大部分时间里,苹果将四分之三的营收用于股票回购。从2015年至2020年,苹果通过回购将已发行流通股减少了24.5%,从58.34亿股减少到44亿股。流通股的大幅减少让每股收益同期增长了三分之一。所以,仅仅股票回购就能使每股收益每年平均提高5.5%,是营收增长对每股收益增长的贡献率的两倍。

回购和营收增长让每股收益共增长了约48%,从8.60美元增长到12.73美元,相当于每年增长8%。当然,到目前为止,股票回购对每股收益的贡献更大。

但苹果股价的上涨幅度更大,从130美元上涨到362美元,涨幅高达176%。股价大涨的原因是苹果市盈率从15提高近一倍达到28。事实证明,突然之间投资者愿意为每一美元收益投入越来越多资金,这是苹果过去五年能为投资者带来丰厚回报的最大因素。

我们把这些数据加在一起。苹果公司在2015年3月至2020年3月期间的总收益率为20%,其中营收增长贡献了2.5个百分点,股票回购贡献了5.5个百分点,股息贡献了2个百分点,总计10%。估值扩张贡献了10个百分点,与其他三个因素的总和相当。

当然,这四个因素也将决定未来五年苹果股价的走势。只是这次,投资者没有了从低点进场的优势。我们假设苹果的市盈率维持在28。这是乐观的预测,因为这个数字远高于今天已经较高的市盈率22。如此高的估值使得估值扩张不再是一个长期驱动因素,当然出现泡沫的可能性始终存在,在这种情况下市盈率或许会短暂上涨。

假设市盈率维持在28,每股收益增长将主要来自其他三个因素:营收增长、股票回购和股息。我们假设苹果的营收延续过去五年的趋势,每年对每股收益增长的贡献率为2.5%。或许这听起来并不高,但要实现利润增长2.5%,苹果每年的销售额需要增加约70亿美元,并且每年都要保持这样的增长势头。

如果苹果按照以往的做法,将75%的营收用于股票回购,则可以把每股收益再提高2.6%。与过去五年相比,股票回购对每股收益的提振效果减少了超过一半。第三个因素股息的贡献率约为1%。将营收增长(2.5%)、股票回购(2.6%)和股息(1%)增加的每股收益相加,总计可以使每股收益增长6.1%。因此,由于当前的高股价导致市盈率不可能继续升高,并且股票回购的效果减弱,按照新的计算方式,苹果未来的收益率只有过去五年(20%)的三分之一左右。

当然,苹果的利润增长速度可能高于每年2.5%。比如,有支持者提到了苹果可穿戴设备和特许服务业务的强劲增长。但坏消息是,在截至3月的一个季度,苹果旗舰iPhone手机的销量和总利润均出现了下滑。苹果多年前之所以能吸引投资者,是因为它是一个增长缓慢的庞然大物,并且股价极低。现在它依旧是一个增长缓慢的庞然大物,但其股价却已经高不可攀。苹果确实像粉丝们说的那样是一家优秀的公司。但苹果唯一表现平平的方面就是股票的前景。(财富中文网)

译者:Biz

过去五年,苹果公司(Apple)股票的业绩惊人,它就像是一列貌似势不可挡的财富快车。但这给正在考虑要不要现在登上这列快车的投资者带来了一个问题。简单来说,作为美国最伟大的企业,苹果公司的股价过高,因此未来五年,投资者的回报率若能达到普普通通的个位数中段,就已经是吉星高照了。

就在三个月前,新冠疫情引发的抛售潮让苹果的股价下跌30%,从历史最高的325美元下跌到2月中旬的224美元,苹果现象似乎已经难以为继。接下来的反弹则让苹果的拥趸们相信,在脱离控制的市场动量的不可抗力下,苹果公司的高股价并非不可撼动。从3月23日到6月20日,苹果股价上涨62%至362美元,打破了之前的纪录,使其市值增长6,000亿美元,相当于奈飞(Netflix)、特斯拉(Tesla)和Adobe的市值总和。此轮上涨创下了全球资本主义史上的最大市值涨幅。

苹果目前的股价远高于其过去五年大部分时间的水平,因此投资者有理由怀疑苹果股票是否仍有投资的价值?要回答这个问题,我们需要研究过去五年苹果能够给投资者带来丰厚回报的因素,以及这些因素未来继续增加回报所面临的障碍。

从2015年3月(其财年的第二季度)至今年3月,苹果的年度总收益率约为20%,其中18%来自资本收益,2%为股息。苹果之所以能给投资者提供如此丰厚的回报,并不是因为其基本面(即营收)迅速增长,而是因为其股价极低,因此进行股票回购收效显著,也为提高市盈率倍数留出了大量空间,投资者愿意通过支付这样的股价来获得收益。

2015年3月,苹果之前四个季度的营收为504亿美元,其市值高达7,580亿美元。所以其市盈率只有15。如此低的市盈率意味着在投资者眼中,该公司的总营收长期持平,甚至在不断下滑。事实上,截至2020年3月,根据最近四个季度的情况,苹果公司的净利润只增长到572.4亿美元,涨幅只有13.6%。这相当于每年只增长2.5%,跑赢通胀约1个百分点。苹果的增长并不强劲。

但苹果有一个强大的工具可以提高其每股收益。作为一台无可匹敌的“提款机”,苹果公司需要的资本投资很少,因此它能够并且依旧在把全部营收用于发放股息和回购股票。到目前为止,股票回购是苹果股价上涨最主要的推动力。在市盈率为15时,苹果用于回购股票的每1美元,可以提高每股收益6.7美分,因为与收益相比,苹果的股价极低。而且按照年平均营收约500亿美元计算,苹果公司的平均市盈率一直维持在15左右,直到2019年年中公司股价开始大幅上涨。

在过去五年的大部分时间里,苹果将四分之三的营收用于股票回购。从2015年至2020年,苹果通过回购将已发行流通股减少了24.5%,从58.34亿股减少到44亿股。流通股的大幅减少让每股收益同期增长了三分之一。所以,仅仅股票回购就能使每股收益每年平均提高5.5%,是营收增长对每股收益增长的贡献率的两倍。

回购和营收增长让每股收益共增长了约48%,从8.60美元增长到12.73美元,相当于每年增长8%。当然,到目前为止,股票回购对每股收益的贡献更大。

但苹果股价的上涨幅度更大,从130美元上涨到362美元,涨幅高达176%。股价大涨的原因是苹果市盈率从15提高近一倍达到28。事实证明,突然之间投资者愿意为每一美元收益投入越来越多资金,这是苹果过去五年能为投资者带来丰厚回报的最大因素。

我们把这些数据加在一起。苹果公司在2015年3月至2020年3月期间的总收益率为20%,其中营收增长贡献了2.5个百分点,股票回购贡献了5.5个百分点,股息贡献了2个百分点,总计10%。估值扩张贡献了10个百分点,与其他三个因素的总和相当。

当然,这四个因素也将决定未来五年苹果股价的走势。只是这次,投资者没有了从低点进场的优势。我们假设苹果的市盈率维持在28。这是乐观的预测,因为这个数字远高于今天已经较高的市盈率22。如此高的估值使得估值扩张不再是一个长期驱动因素,当然出现泡沫的可能性始终存在,在这种情况下市盈率或许会短暂上涨。

假设市盈率维持在28,每股收益增长将主要来自其他三个因素:营收增长、股票回购和股息。我们假设苹果的营收延续过去五年的趋势,每年对每股收益增长的贡献率为2.5%。或许这听起来并不高,但要实现利润增长2.5%,苹果每年的销售额需要增加约70亿美元,并且每年都要保持这样的增长势头。

如果苹果按照以往的做法,将75%的营收用于股票回购,则可以把每股收益再提高2.6%。与过去五年相比,股票回购对每股收益的提振效果减少了超过一半。第三个因素股息的贡献率约为1%。将营收增长(2.5%)、股票回购(2.6%)和股息(1%)增加的每股收益相加,总计可以使每股收益增长6.1%。因此,由于当前的高股价导致市盈率不可能继续升高,并且股票回购的效果减弱,按照新的计算方式,苹果未来的收益率只有过去五年(20%)的三分之一左右。

当然,苹果的利润增长速度可能高于每年2.5%。比如,有支持者提到了苹果可穿戴设备和特许服务业务的强劲增长。但坏消息是,在截至3月的一个季度,苹果旗舰iPhone手机的销量和总利润均出现了下滑。苹果多年前之所以能吸引投资者,是因为它是一个增长缓慢的庞然大物,并且股价极低。现在它依旧是一个增长缓慢的庞然大物,但其股价却已经高不可攀。苹果确实像粉丝们说的那样是一家优秀的公司。但苹果唯一表现平平的方面就是股票的前景。(财富中文网)

译者:Biz

The spectacular performance of Apple stock over the past half-decade created a problem for folks pondering whether to board this seemingly unstoppable express right now. Put simply, America’s greatest enterprise has gotten so expensive that for the next five years, investors will be lucky to make plodding, mid-single-digit returns.

Just over three months ago, it appeared that the Apple phenomenon was faltering when the COVID-19 selloff drove its shares down 30% from their all-time high of $325 in mid-February to $224. Next came a rebound that had fans believing that Apple’s big price is no immovable object when confronted with the irresistible force of its runaway momentum. From March 23 to June 20, the iPhone maker climbed 62% to $362, beating the previous record and adding $600 billion to its valuation, approximately equal to the combined market caps of Netflix, Tesla, and Adobe. That jump must mark the biggest value spike in the annals of world capitalism.

Given that Apple’s share price now stands far above its levels for most of the past five years, it’s reasonable to ask whether it’s still a bargain. To answer that question, let’s examine the factors that enabled Apple to deliver such stupendous returns over the past half-decade, and handicap whether those levers can conceivably provide the same lift in the years ahead.

From the end of March 2015 (the second quarter of its fiscal year) to March of this year, Apple delivered total annual returns of roughly 20%: 18% from capital gains and 2% from dividends. It was able provide such sumptuous rewards not because the basics––its earnings––expanded rapidly, but because its shares were extremely cheap, giving its stock repurchases lots of bang-for-the-buck and leaving plenty of runway for growth in its P/E multiple, the share price investors are willing to pay for each dollar in profits.

In March of 2015, Apple had earned $50.4 billion over the previous four quarters, and its market cap stood at $758 billion. Hence, its multiple was just 15. A figure that low implies that investors viewed its total dollar earnings as staying flat for a long time, or even declining. In fact, Apple’s net profits only rose to $57.24 billion through March of 2020 based on the most recent four quarters, or 13.6%. That’s a gain of just 2.5% a year, beating inflation by around a point. A growth juggernaut Apple was not.

But Apple had a powerful tool for lifting its earnings per share. This matchless cash machine requires so little capital investment that it can, and still does, plow all of its earnings into dividends and buybacks, the latter being by far its biggest driver. At that P/E of 15, every dollar in repurchases raised Apple’s EPS by 6.7¢ because its shares were so inexpensive in comparison to its profits. And its average P/E remained in the 15 bargain range, based on average earnings of around $50 billion a year, until the moonshot in its stock price started in mid-2019.

During most of those five years, Apple was spending three-quarters of its earnings on buybacks. From 2015 to 2020, that campaign lowered its count 24.5% from 5.834 billion to 4.4 billion shares. The big shrink raised EPS by around one-third over that period. So buybacks alone increased EPS by an average of 5.5% annually, over twice the contribution from earnings.

All told, buybacks and earnings growth combined to swell earnings per share around 48%, or 8% a year, from $8.60 to $12.73. Of course, repurchases packed by far the greater firepower.

But Apple’s share price jumped by far more, by 176% from $130 to $362. The additional juice came from an almost doubling of Apple’s P/E multiple from 15 to 28. It was that explosion in investors’ sudden willingness to pay more and more for each dollar in earnings that proved the biggest factor in delivering those big five-year returns.

Let’s add it up. Of Apple’s total returns from March 2015 through March 2020 of 20%, earnings gains contributed 2.5 points, repurchases 5.5, and dividends 2, for a total of 10%. Multiple expansion alone provided a 10-point boost, matching the other three factors combined.

Of course, those same four drivers will also determine how Apple’s shares perform over the next half-decade. But this time, investors don’t start with the edge of buying in cheap. Let’s posit that Apple’s P/E remains steady at 28. That’s an optimistic projection since that multiple is well above today’s not modest 22. That lofty valuation takes multiple expansion pretty much off the table as a long-run driver, although the P/E could spike temporarily if we enter bubble land, always a possibility.

Assuming the P/E remains flat at 28, all gains need to come from the other three components: earnings growth, buybacks, and dividends. We’ll assume that earnings continue on their five-year trend by advancing 2.5% a year. If that sounds like a low bar, consider that to generate 2.5% profit growth, Apple needs to add around $7 billion in new sales every year, and keep doing it year in and year out.

If Apple spends its usual 75% of earnings on buybacks, repurchases will raise EPS another 2.6%. That’s less than half the kick they supplied for most of the past five years. The third contributor is the dividend of around 1%. Stack the building blocks, and earnings add 2.5%, buybacks 2.6%, and dividends 1%, for a total of 6.1%. Hence, the new Apple math, dictated by its current high price that makes a higher P/E unlikely and buybacks less potent, points to future returns that are about one-third of its 20% gains over the past five years.

Of course, it’s possible that Apple will expand profits a lot faster than 2.5% a year. Its champions cite strong growth in its wearables and services franchises. On the negative side, sales in its flagship iPhones, and total profits, declined in the March quarter. No, Apple was so appealing a few years ago because it was a slow-growth stalwart that was dirt cheap. It’s still a slow-growth stalwart, but now it’s premium priced. As an enterprise, Apple'’s as superb as its fans claim. The only thing mediocre about Apple is the outlook for its stock.

请打开财富Plus APP