熊市过后美股迅速反弹,竟然几乎收复了失地

Ben Carlson

2020-06-08

从今年的经济形势看,行情的大起大落从许多方面来看都是合情合理的。

文本设置

文本设置

Plus(0条)

Plus(0条)

今年2月和3月,美股下跌的速度和混乱程度让人抓狂。3月是自大萧条以来股市波动性最大的一个月。

但由于新冠疫情导致的痛苦和困扰,出现这种行情从许多方面来看都是合情合理的。

从3月末以来市场反弹的速度和爆发力,让许多市场参与者难以理解。股市反弹的主要原因是几乎在市场进入熊市的同时,美国政府出台了财政和货币响应措施。

但即便在政府的干预下,也不会有投资者能想到,股市在3月23日才刚刚触底,能够反弹到当前的水平。

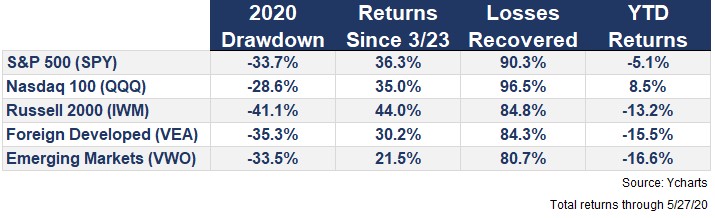

3月23日,标普500指数暴跌近34%,之后反弹了36%,但距离其最高点依旧下跌了9.7%:

你很难相信经历过一场崩盘之后,标普500指数的同比下跌幅度只有个位数。

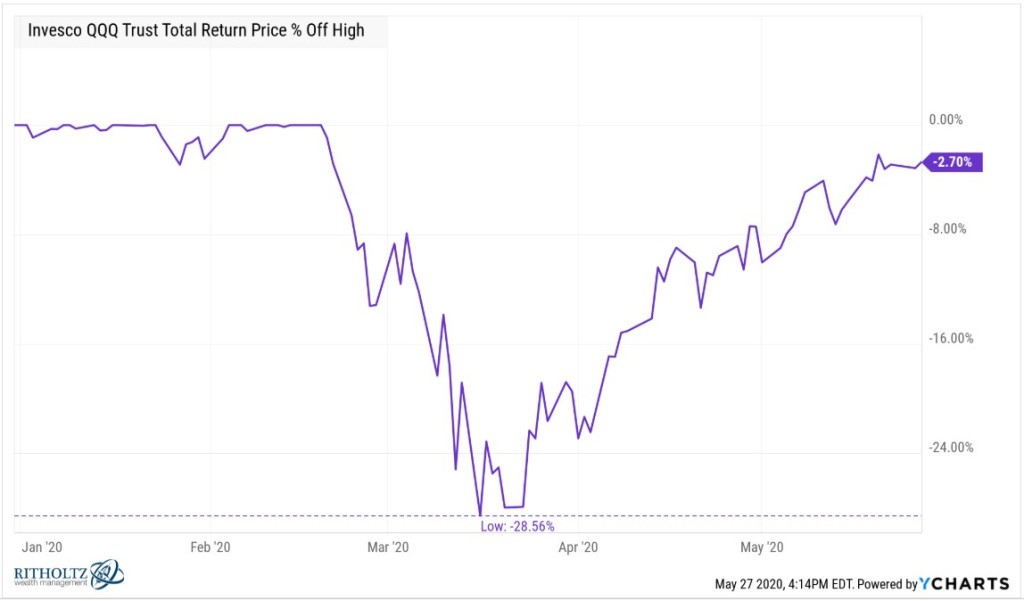

在危机期间,最大科技股始终保持良好的势头。由于纳斯达克100指数以大型科技公司为主,因此该指数是今年表现最好的指数之一。尽管亚马逊(Amazon)、苹果(Apple)、微软(Microsoft)和谷歌(Google)等公司的股票依旧坚挺,但在股市崩盘期间,纳斯达克100指数依旧下跌了近30%:

现在,该指数已经收复了大部分失地,并且同比上涨了近9%,距离最高点只相差不足3%。

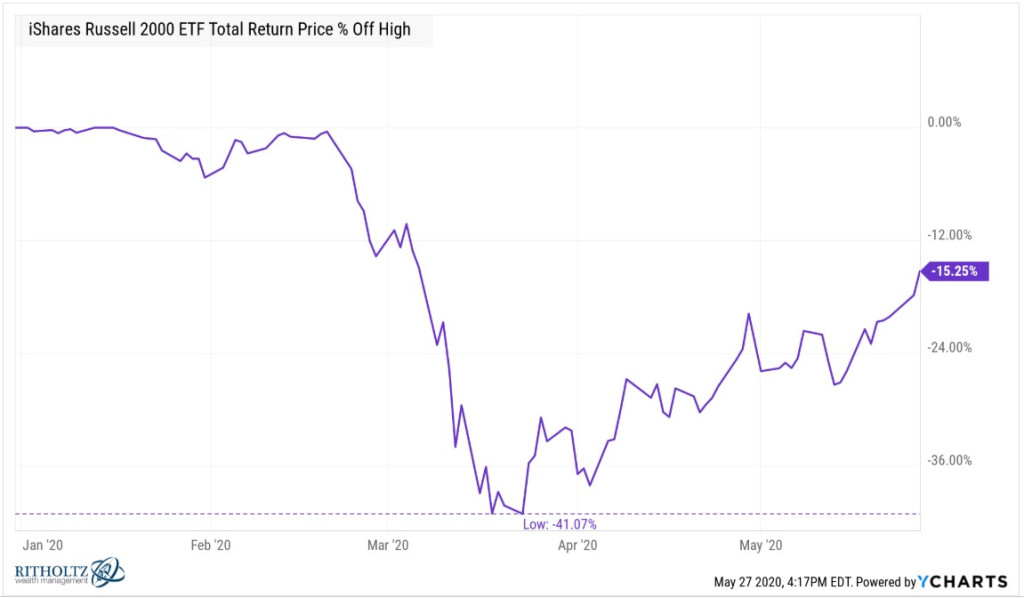

此轮下跌对小盘股的冲击更大:

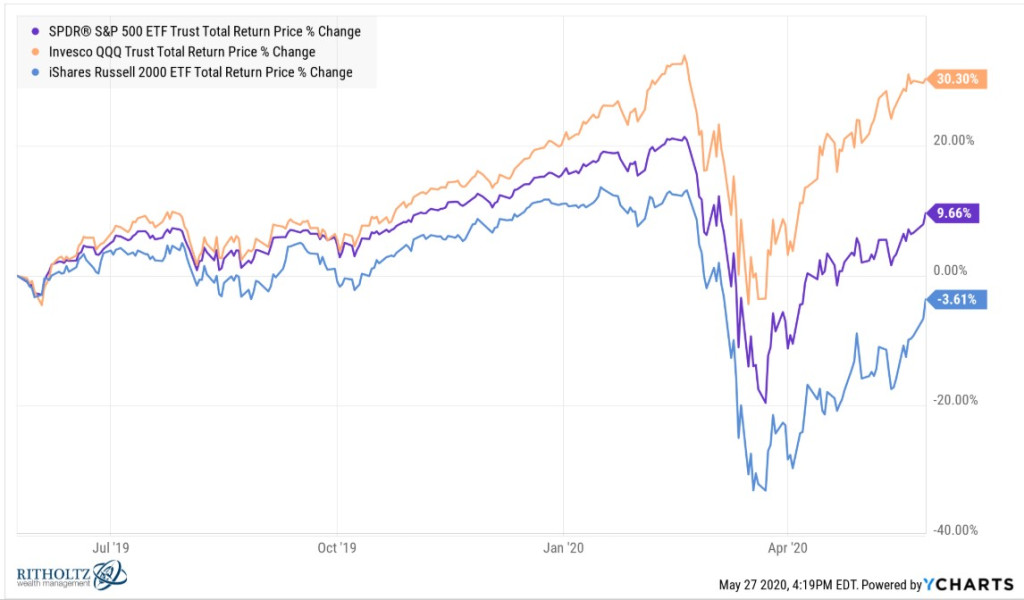

小盘股虽然也有大幅反弹,但美国三个股票市场过去一年的反弹幅度各有不同:

纳斯达克100指数虽然暴跌了29%,但过去12个月上涨超过30%,而小盘股却下跌近4%。

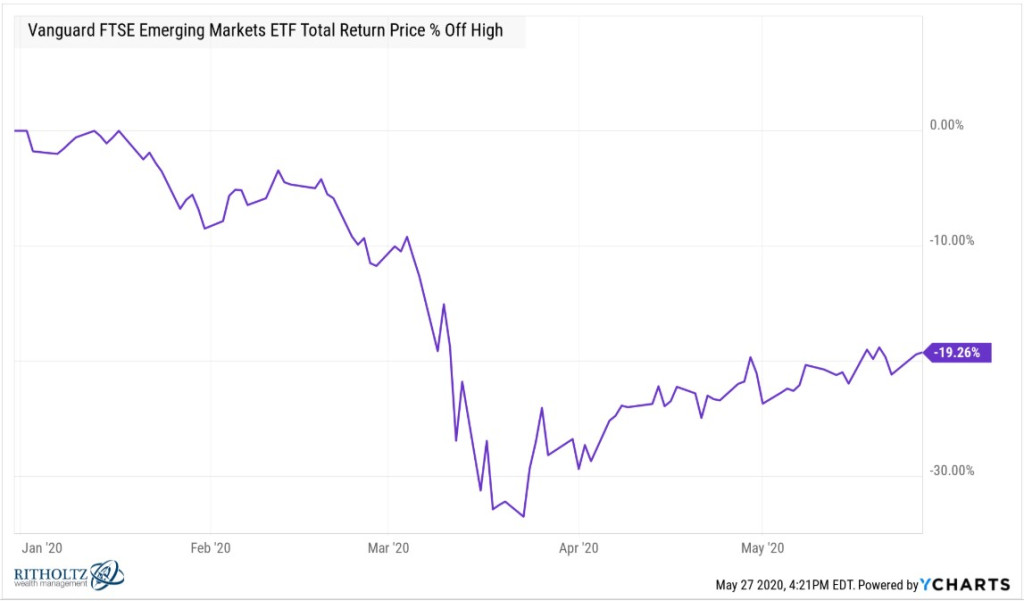

在2008年金融危机期间,新兴市场的股市跌幅接近70%(标普500指数跌幅为56%),但让人意外的事,在此轮熊市中,发展中国家的股市竟然与美国大盘股的跌幅相当:

但新兴市场没有出现相同幅度的反弹,所以今年这些地区的股市跌幅依旧接近20%。

在此轮股市崩盘中,其他发达市场的跌幅实际上大于新兴市场,但发达市场的反弹更加明显。

下文总结了自3月23日至5月27日收盘每个市场的反弹情况:

排在首位的是谁?小盘股,上涨超过43%。在熊市过后,小公司往往会领涨,因为:

(1)它们在市场崩盘情境中遭到严重冲击,并且

(2)市场中风险更高的要素通常会引领市场走出危机

综合这些数据,你会发现全球股市都已经收回了自3月末以来的大部分损失:

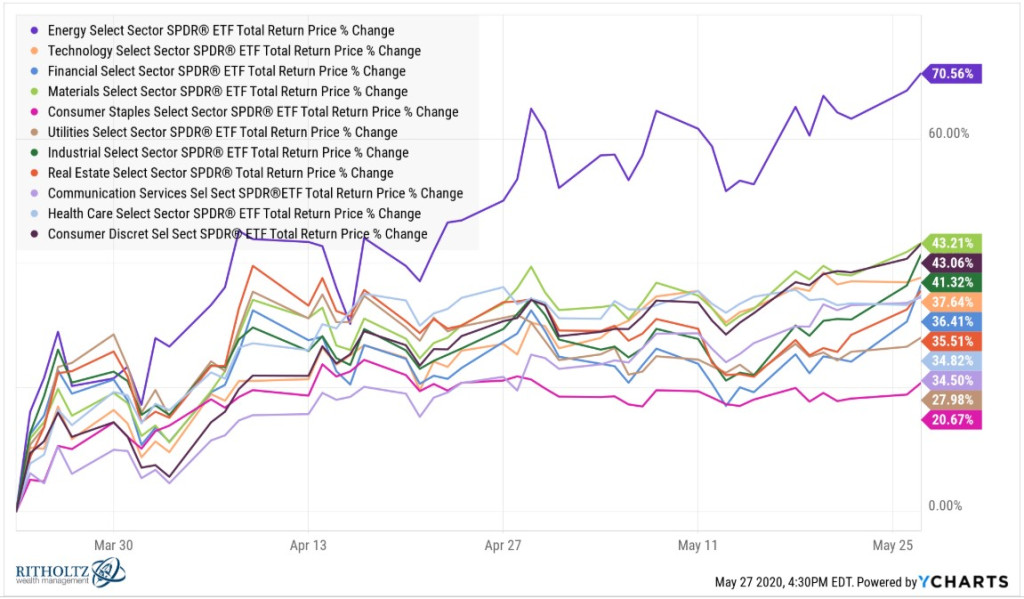

标普500指数不同行业从本轮熊市的低谷反弹的趋势,也给我们一些启示:

多年来,能源股始终低迷,但在此次危机期间,能源股的跌幅高达59.86%,远超过其他行业。

科技股经过初期的稳定和后期上涨之后,年初至今的反弹幅度为6.37%,领先于其他行业,消费者服务和非必需消费品行业也大幅反弹,而排在最后的是医疗保健与能源股,分别下跌20.97%和31.55%,

2020年只过去了不到一半,但我们似乎已经走完了正常情况下需要几年时间才能走完的3个不同周期。

真是疯狂的一年! (财富中文网)

本文作者是注册金融分析师本•卡尔森(Ben Carlson),他是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。作者可能持有文中提及的证券或资产。

译者:Biz

今年2月和3月,美股下跌的速度和混乱程度让人抓狂。3月是自大萧条以来股市波动性最大的一个月。

但由于新冠疫情导致的痛苦和困扰,出现这种行情从许多方面来看都是合情合理的。

从3月末以来市场反弹的速度和爆发力,让许多市场参与者难以理解。股市反弹的主要原因是几乎在市场进入熊市的同时,美国政府出台了财政和货币响应措施。

但即便在政府的干预下,也不会有投资者能想到,股市在3月23日才刚刚触底,能够反弹到当前的水平。

3月23日,标普500指数暴跌近34%,之后反弹了36%,但距离其最高点依旧下跌了9.7%:

你很难相信经历过一场崩盘之后,标普500指数的同比下跌幅度只有个位数。

在危机期间,最大科技股始终保持良好的势头。由于纳斯达克100指数以大型科技公司为主,因此该指数是今年表现最好的指数之一。尽管亚马逊(Amazon)、苹果(Apple)、微软(Microsoft)和谷歌(Google)等公司的股票依旧坚挺,但在股市崩盘期间,纳斯达克100指数依旧下跌了近30%:

现在,该指数已经收复了大部分失地,并且同比上涨了近9%,距离最高点只相差不足3%。

此轮下跌对小盘股的冲击更大:

小盘股虽然也有大幅反弹,但美国三个股票市场过去一年的反弹幅度各有不同:

纳斯达克100指数虽然暴跌了29%,但过去12个月上涨超过30%,而小盘股却下跌近4%。

在2008年金融危机期间,新兴市场的股市跌幅接近70%(标普500指数跌幅为56%),但让人意外的事,在此轮熊市中,发展中国家的股市竟然与美国大盘股的跌幅相当:

但新兴市场没有出现相同幅度的反弹,所以今年这些地区的股市跌幅依旧接近20%。

在此轮股市崩盘中,其他发达市场的跌幅实际上大于新兴市场,但发达市场的反弹更加明显。

下文总结了自3月23日至5月27日收盘每个市场的反弹情况:

排在首位的是谁?小盘股,上涨超过43%。在熊市过后,小公司往往会领涨,因为:

(1)它们在市场崩盘情境中遭到严重冲击,并且

(2)市场中风险更高的要素通常会引领市场走出危机

综合这些数据,你会发现全球股市都已经收回了自3月末以来的大部分损失:

标普500指数不同行业从本轮熊市的低谷反弹的趋势,也给我们一些启示:

多年来,能源股始终低迷,但在此次危机期间,能源股的跌幅高达59.86%,远超过其他行业。

科技股经过初期的稳定和后期上涨之后,年初至今的反弹幅度为6.37%,领先于其他行业,消费者服务和非必需消费品行业也大幅反弹,而排在最后的是医疗保健与能源股,分别下跌20.97%和31.55%,

2020年只过去了不到一半,但我们似乎已经走完了正常情况下需要几年时间才能走完的3个不同周期。

真是疯狂的一年! (财富中文网)

本文作者是注册金融分析师本•卡尔森(Ben Carlson),他是里萨兹财富管理公司(Ritholtz Wealth Management)机构资产管理部门的主任。作者可能持有文中提及的证券或资产。

译者:Biz

The speed and turbulence of the stock market’s downturn in February and March was insane. March was the most volatile month since the Great Depression.

The move made sense in many ways, though, because of the pain and confusion caused by the pandemic.

The speed and explosiveness of the market’s rally since late-March is more of a head-scratcher to many market participants. Much of this recovery can be attributed to the fact that the fiscal and monetary response occurred nearly as fast as the bear market itself.

Even with government interventions, I’m not sure any investors would have assumed stocks would be at current levels when they bottomed on March 23.

The S&P 500 was down close to 34% that day and remains in a 9.7% drawdown following a 36% rally ever since:

•

It’s hard to believe after the crash we experienced that the S&P 500 is now showing just single-digit losses on the year.

The biggest tech stocks have held up extremely well throughout the crisis. Since they make up the majority of the Nasdaq 100, that remains one of the best performing indexes this year. Despite the strength in stocks like Amazon, Apple, Microsoft and Google, the Nasdaq 100 did fall nearly 30% in the crash:

•

It’s now less than 3% off the highs after recovering most of those losses and up almost 9% on the year.

Small-cap stocks were hit much harder than large-cap stocks in the downturn:

•

Small caps have experienced a nice bounce but it really is a tale of 3 markets when you look at the returns of these 3 subsets of the U.S. stock market over the past year:

•

Even with a 29% nose-dive, the Nasdaq 100 is up more than 30% over the past 12 months while small-cap stocks are down nearly 4%.

In the 2008 crisis, emerging markets fell close to 70% (against a 56% fall for the S&P 500) so it may come as a surprise to learn developing country stocks had roughly the same drawdown as large U.S. corporations in this bear market:

•

Emerging markets haven’t had the same level of recovery so it remains down nearly 20% this year.

Foreign developed markets actually fell more than emerging markets in this slump but have seen a more pronounced rally:

•

Here is the summary of the rebounds in each of these markets since the bottom on March 23rd through the close on May 27th:

•

At the head of the pack? Small-cap stocks, which have have surged more than 43%. Smaller companies tend to lead the way following a bear market because:

(1) they get hit so hard during a market crash scenario and

(2) the riskier elements of the market typically lead the way coming out of a crisis

Putting this all together you can see stock markets around the world have made up a majority of their losses since late-March:

•

The S&P 500 sector returns from the bottom of this bear market are also telling:

•

Energy stocks have been getting crushed for a number of years now but they got pummeled more than any sector during the crisis, down 59.86%.

After the initial flush and subsequent advance, tech stocks have been leading the way with a YTD return of 6.37%, consumer services and consumer discretionary are also in the green, while Health Care and Energy are pulling up the rear at -20.97 and -31.55 respectively.

It feels like we’ve already lived through 3 different cycles that would normally take place over the course of a number of years and 2020 hasn’t even reached the halfway point yet.

What a wild year.

Ben Carlson, CFA, is the director of institutional asset management at Ritholtz Wealth Management. He may own securities or assets discussed in this piece.

请打开财富Plus APP