Tiktok网红数了1万粒大米,来教授青少年理财知识

POLINA MARINOVA

2020-03-26

金融知识的缺乏,不光会影响到个人财富积累,更严重的是,如果不懂得自我防范,可能会带来灾难性的后果。

文本设置

文本设置

Plus(0条)

Plus(0条)

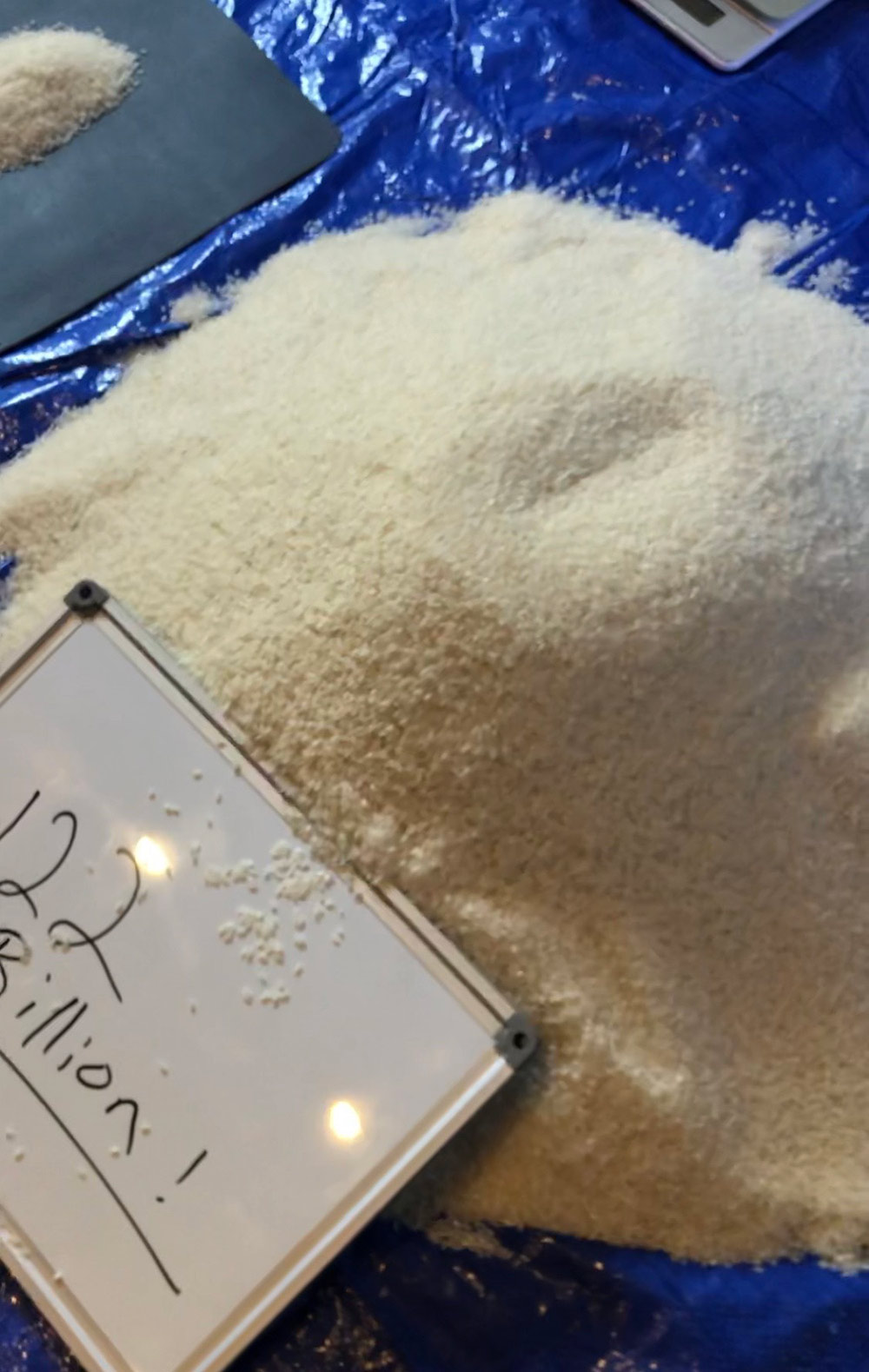

“贝佐斯的大米有26公斤!”

最近的一个周六晚上,32岁的电子商务企业家汉弗莱·杨花了一整晚数了1万粒大米,他这是为了向Tiktok的青少年用户解释钱的规模。

他想让青少年们知道,坐拥10亿美元是个什么样的概念,他以全球最富有的人之一,亚马逊首席执行官杰夫•贝佐斯为例,贝佐斯净资产估计为1220亿美元。

“如果每粒大米代表10万美元,贝佐斯的大米有26公斤。各位,看看这有多大一摊。太疯狂了,”杨在短视频中说,边说边把键盘插在代表贝佐斯财富的米堆里。

和国内抖音一样,Tiktok也广受青少年欢迎。杨制作的系列节目里,有两段60秒视频在Tiktok上疯狂走红,播放达220万次。他告诉《财富》杂志,视频之所以受欢迎,部分原因是“令人震惊的视觉效果”。

这并不是杨第一次来解释和钱有关的话题,他其它的短视频里,介绍过社保税、股市和信用评分等。他的视频得到了210多万个点赞,而现在像他这样的个人理财网红越来越多。

Tiktok的大多数内容是青少年搞笑跳舞之类的段子,尽管这样,杨还是努力在60秒短视频内,向30多万关注粉丝介绍预算、储蓄和投资方面的知识。

“我只是为了吸引观众,抛出一些信息激发兴趣,这样你就能自己去研究了,”杨说。“我经常收到私信说,‘真希望学校也能这么教我。’”

“金融素养”远未普及

杨说的话不无道理。如今在美国,有21个州要求学校在现有课程中纳入数学、经济学等个人理财内容,但只有六个州规定高中生必须参加单独的个人理财课程。在中国国内,也只有北上广少数中小学校有添加一些创新性金融理财课程,但是此类课程也仅局限于试点教育,并未纳入基础教育框架。

2012年,国际学生评估项目(PISA)开展了全球金融素养研究,主要衡量15岁儿童应用理财知识的能力。中国上海市学生的金融素养领先比利时,位列全球第一,其它得高分的有来自澳洲、爱沙尼亚、新西兰等地的学生。不过,其它一些通常在PISA测试中表现优异的国家,如芬兰、日本、韩国、新加坡、及中国港澳台地区等并没有参加这次全球财经素养测评。

美国普通学生的表现则并不好,协调负责PISA研究的理财素养专家卢萨尔迪说,成年人的知识更加令人担心。她曾经提出过五个问题来判断参与者的金融素养。其中一个问题问的是:“假设一个储蓄账户里有100美元,利率是每年2%。如果钱一直放在账户里涨利息,五年后会有多少钱?” 结果,只有三分之一的美国人能准确回答。

“在理财领域,无知并不是福,”卢萨尔迪说。

“金融素养”又称为“财经素养”,对应英文词汇是“Financial Literacy”。目前,它已成为一个教育领域,规模正逐步扩大,有超过50多个国家发布并实施了相应的教育计划。但是,落实到现实中,距离金融素养真正的全民普及,除芬兰等少数国家外,各国都还有很长的路要走。在中国国内,金融素养教育也是一个新兴领域,直到2018年,中国才拥有了第一份领域内规范性文件《中国财经素养教育标准》,但目前也仅仅只是一个框架而已,远远没到实施普及的程度。

2010年,卢萨尔迪就年轻人对金融知识的掌握开展了一项研究,她发现,回答体现金融素养的问题时,女性更容易答错。只有一小部分人的金融素养较高,他们大多是年轻男性,家人都受过高等教育。

金融知识的缺乏,不光会影响到个人财富积累,更严重的是,如果不懂得自我防范,可能会带来灾难性的后果。2008年金融危机夺取了很多人的未来,至今,美国人中还有相当一大部分比例手中流动性应急现金不足400美元。在中国,频频发生的大学生校园贷受骗事件也说明了年轻人严重缺乏金融常识。

“如果在学校里不教金融知识,有些群体就更难学到了,”卢萨尔迪说,“他们能去哪学呢?”

买股票要学学泰勒·斯威夫特

在海莉·萨克斯看来,可以通过网络搜索理财知识。她刚找到第一份全职工作时,单位问她计划缴多少养老金(注:美国养老金上缴比例由个人决定,单位给予相应匹配),“我装作知道,然后努力去搜索,但是我能找到的内容实在是太少了,”她说。

搜索知识时,她才发现看似微不足道的决定对未来个人财务多么重要。所以她问自己:为什么没人跟我说过这些?

萨克斯开始大量学习,继而开始用她和她朋友都能弄懂的语言来解释复杂的话题。她在YouTube网络上开设了频道,把华尔街行话转为通俗语言,用流行文化来解释金融概念。

比如,她拿乡村歌手泰勒·斯威夫特的职业生涯来解释股票,用名人卡戴珊家族来说明养老金提前缴税跟退休后缴税的区别,用约会类真人秀节目《单身汉》来解释投资银行。

萨克斯在YouTube上粉丝约3000人,在Instagram上粉丝有12万。她说:“我想帮助年轻人轻松过渡到成年期,开启自己的理财之旅。”

最近,萨克斯更专注于个人理财内容,她说她正学习成为合格的理财规划师,之后就可以向粉丝提供个人理财建议。

“互联网这代年轻人,可能是企业家最多的一代人,”她说。“这意味着所有人都要学会如何赚钱,如何管理资金,如何纳税等。我们一定要给他们知识的武装。”

凯蒂·斯旺森是两个孩子的母亲,和其它各年龄层很多人一样,她也热衷于收集打折券,但她最近却因此成为网红,被人称为“打折券凯蒂”,在Tiktok上,她的粉丝已达130万,她巧用打折券来省钱的短视频收到了超过3600万点赞。

“很多人告诉我,感觉研究优惠券是妈妈辈或奶奶辈做的事,从来没想过可以用优惠券填补收入,”她说。

斯旺森承认,抖音上大部分内容都是娱乐,所以她制作的大部分视频搞笑的同时再带点信息量。教育和娱乐之间的界限有时很难分清,尤其是在视频最长只有60秒的平台上。

内容质量则正是研究者卢萨尔迪最担心的部分。“我们要小心可能忽略了很多实质内容,”她说,“不能让抖音上的人来教我们个人理财,应该让学校来教。”

网红们的理财妙招

1.计算开销:“真人秀《XX的奢华生活》里,我们可以看到过碧昂丝的生活要花多少钱。我们也应该搞清楚我们自己的生活要花多少钱。统计下过去三个月的支出,算出我们日常生活要花多少钱,然后为自己准备相应的应急资金。”——海莉·萨克斯

2. 长远打算:“不考虑长远打算,只满足短期消费,这通常不值得。从长远来看,200美元买一件衬衫真的值吗?我的回答是很可能不值。大多数年轻人都很短视,结果就是,可能欠下一屁股信用卡债务。”——汉弗莱·杨

3.多多学习:“要做出各种理财决定,我们必须有相应的知识。理财是很个人的,并非所有大众化建议都适用。我们需要了解理财的基本知识,它真的会给你带来收益。如果你是在学校上学的年轻人,好好读书。别错过学习的机会。”——安娜马利亚·卢萨尔迪(财富中文网)

译者:梁宇

审校:夏林

责编:雨晨

你以为抖音现在还只是一些让青少年傻乎乎大笑的段子吗?错了!针对如此众多的青少年受众,无论是国内抖音还是Tiktok(Tiktok),都开始走知识路线。国内的抖音有了各种各样的教育类账号,其中有一些网络红人拥有千万粉丝。而在Tiktok里,目前最火的账号是教青少年如何理财的。

“贝佐斯的大米有26公斤!”

最近的一个周六晚上,32岁的电子商务企业家汉弗莱·杨花了一整晚数了1万粒大米,他这是为了向Tiktok的青少年用户解释钱的规模。

他想让青少年们知道,坐拥10亿美元是个什么样的概念,他以全球最富有的人之一,亚马逊首席执行官杰夫•贝佐斯为例,贝佐斯净资产估计为1220亿美元。

“如果每粒大米代表10万美元,贝佐斯的大米有26公斤。各位,看看这有多大一摊。太疯狂了,”杨在短视频中说,边说边把键盘插在代表贝佐斯财富的米堆里。

和国内抖音一样,Tiktok也广受青少年欢迎。杨制作的系列节目里,有两段60秒视频在Tiktok上疯狂走红,播放达220万次。他告诉《财富》杂志,视频之所以受欢迎,部分原因是“令人震惊的视觉效果”。

这并不是杨第一次来解释和钱有关的话题,他其它的短视频里,介绍过社保税、股市和信用评分等。他的视频得到了210多万个点赞,而现在像他这样的个人理财网红越来越多。

Tiktok的大多数内容是青少年搞笑跳舞之类的段子,尽管这样,杨还是努力在60秒短视频内,向30多万关注粉丝介绍预算、储蓄和投资方面的知识。

“我只是为了吸引观众,抛出一些信息激发兴趣,这样你就能自己去研究了,”杨说。“我经常收到私信说,‘真希望学校也能这么教我。’”

“金融素养”远未普及

杨说的话不无道理。如今在美国,有21个州要求学校在现有课程中纳入数学、经济学等个人理财内容,但只有六个州规定高中生必须参加单独的个人理财课程。在中国国内,也只有北上广少数中小学校有添加一些创新性金融理财课程,但是此类课程也仅局限于试点教育,并未纳入基础教育框架。

2012年,国际学生评估项目(PISA)开展了全球金融素养研究,主要衡量15岁儿童应用理财知识的能力。中国上海市学生的金融素养领先比利时,位列全球第一,其它得高分的有来自澳洲、爱沙尼亚、新西兰等地的学生。不过,其它一些通常在PISA测试中表现优异的国家,如芬兰、日本、韩国、新加坡、及中国港澳台地区等并没有参加这次全球财经素养测评。

美国普通学生的表现则并不好,协调负责PISA研究的理财素养专家卢萨尔迪说,成年人的知识更加令人担心。她曾经提出过五个问题来判断参与者的金融素养。其中一个问题问的是:“假设一个储蓄账户里有100美元,利率是每年2%。如果钱一直放在账户里涨利息,五年后会有多少钱?” 结果,只有三分之一的美国人能准确回答。

“在理财领域,无知并不是福,”卢萨尔迪说。

“金融素养”又称为“财经素养”,对应英文词汇是“Financial Literacy”。目前,它已成为一个教育领域,规模正逐步扩大,有超过50多个国家发布并实施了相应的教育计划。但是,落实到现实中,距离金融素养真正的全民普及,除芬兰等少数国家外,各国都还有很长的路要走。在中国国内,金融素养教育也是一个新兴领域,直到2018年,中国才拥有了第一份领域内规范性文件《中国财经素养教育标准》,但目前也仅仅只是一个框架而已,远远没到实施普及的程度。

2010年,卢萨尔迪就年轻人对金融知识的掌握开展了一项研究,她发现,回答体现金融素养的问题时,女性更容易答错。只有一小部分人的金融素养较高,他们大多是年轻男性,家人都受过高等教育。

金融知识的缺乏,不光会影响到个人财富积累,更严重的是,如果不懂得自我防范,可能会带来灾难性的后果。2008年金融危机夺取了很多人的未来,至今,美国人中还有相当一大部分比例手中流动性应急现金不足400美元。在中国,频频发生的大学生校园贷受骗事件也说明了年轻人严重缺乏金融常识。

“如果在学校里不教金融知识,有些群体就更难学到了,”卢萨尔迪说,“他们能去哪学呢?”

买股票要学学泰勒·斯威夫特

在海莉·萨克斯看来,可以通过网络搜索理财知识。她刚找到第一份全职工作时,单位问她计划缴多少养老金(注:美国养老金上缴比例由个人决定,单位给予相应匹配),“我装作知道,然后努力去搜索,但是我能找到的内容实在是太少了,”她说。

搜索知识时,她才发现看似微不足道的决定对未来个人财务多么重要。所以她问自己:为什么没人跟我说过这些?

萨克斯开始大量学习,继而开始用她和她朋友都能弄懂的语言来解释复杂的话题。她在YouTube网络上开设了频道,把华尔街行话转为通俗语言,用流行文化来解释金融概念。

比如,她拿乡村歌手泰勒·斯威夫特的职业生涯来解释股票,用名人卡戴珊家族来说明养老金提前缴税跟退休后缴税的区别,用约会类真人秀节目《单身汉》来解释投资银行。

萨克斯在YouTube上粉丝约3000人,在Instagram上粉丝有12万。她说:“我想帮助年轻人轻松过渡到成年期,开启自己的理财之旅。”

最近,萨克斯更专注于个人理财内容,她说她正学习成为合格的理财规划师,之后就可以向粉丝提供个人理财建议。

“互联网这代年轻人,可能是企业家最多的一代人,”她说。“这意味着所有人都要学会如何赚钱,如何管理资金,如何纳税等。我们一定要给他们知识的武装。”

凯蒂·斯旺森是两个孩子的母亲,和其它各年龄层很多人一样,她也热衷于收集打折券,但她最近却因此成为网红,被人称为“打折券凯蒂”,在Tiktok上,她的粉丝已达130万,她巧用打折券来省钱的短视频收到了超过3600万点赞。

“很多人告诉我,感觉研究优惠券是妈妈辈或奶奶辈做的事,从来没想过可以用优惠券填补收入,”她说。

斯旺森承认,抖音上大部分内容都是娱乐,所以她制作的大部分视频搞笑的同时再带点信息量。教育和娱乐之间的界限有时很难分清,尤其是在视频最长只有60秒的平台上。

内容质量则正是研究者卢萨尔迪最担心的部分。“我们要小心可能忽略了很多实质内容,”她说,“不能让抖音上的人来教我们个人理财,应该让学校来教。”

网红们的理财妙招

1.计算开销:“真人秀《XX的奢华生活》里,我们可以看到过碧昂丝的生活要花多少钱。我们也应该搞清楚我们自己的生活要花多少钱。统计下过去三个月的支出,算出我们日常生活要花多少钱,然后为自己准备相应的应急资金。”——海莉·萨克斯

2. 长远打算:“不考虑长远打算,只满足短期消费,这通常不值得。从长远来看,200美元买一件衬衫真的值吗?我的回答是很可能不值。大多数年轻人都很短视,结果就是,可能欠下一屁股信用卡债务。”——汉弗莱·杨

3.多多学习:“要做出各种理财决定,我们必须有相应的知识。理财是很个人的,并非所有大众化建议都适用。我们需要了解理财的基本知识,它真的会给你带来收益。如果你是在学校上学的年轻人,好好读书。别错过学习的机会。”——安娜马利亚·卢萨尔迪(财富中文网)

译者:梁宇

审校:夏林

责编:雨晨

Humphrey Yang, a 32-year-old e-commerce entrepreneur, spent a recent Saturday night counting 10,000 individual grains of rice to explain the scale of money to teenagers on TikTok.

He wanted to help them visualize $1 billion and provide context about what it means to have that kind of money. His example: Amazon’s billionaire CEO Jeff Bezos, whose net worth was estimated to be $122 billion at the time of Yang’s video.

“Jeff Bezos has 58 pounds of rice if each grain of rice is $100,000. Look at how big that is, guys. That’s insane,” Yang says in the video, as he sticks a keyboard in the pile of rice meant to represent Bezos’s riches.

The project culminated in two viral 60-second videos that garnered a combined 2.2 million views on TikTok, a short-form video app popular with teens. He told Fortune that part of the reason he thinks it resonated with viewers is that it provided “a shocking visual representation.”

This isn’t the first time Yang has posted an explainer on the topic of money. He has videos about Social Security taxes, the stock market, and credit scores. With more than 2.1 million video likes on TikTok, he’s one of a growing number of personal finance influencers gaining prominence and clout on the platform.

Even though TikTok is a platform largely used by teens to post silly dance videos, Yang uses his channel to impart lessons on budgeting, saving, and investing to his 305,000 followers—all in under 60 seconds.

“I’m just trying to capture your attention and give you some information to pique your interest so that you go do the research yourself,” Yang said. “It’s pretty often that I get messages saying, ‘I wish my school taught this.’”

Yang has a point. Twenty-one states mandate that schools integrate personal finance content into existing classes, such as math, economics, and technology courses. But only six states require that high school students take a stand-alone personal finance course to graduate.

The statistics paint an even bleaker picture. In 2012, the Programme for International Student Assessment (PISA) conducted a worldwide financial literacy study that measured the proficiency of 15-year-olds in applying financial knowledge.

How did American teens perform?

“The average American student doesn’t fare very well compared to the countries and economies that participated in [the global financial literacy study],” says Annamaria Lusardi, an expert on financial literacy and financial education who helped lead the PISA study. “And then when we look at the adult population, the numbers are really frightening.”

Lusardi, who teaches at George Washington University, teamed up with Olivia Mitchell, a professor at the Wharton School, to develop five questions that indicate a person’s financial literacy. For example, one of the questions posits: “Suppose you had $100 in a savings account and the interest rate was 2% per year. After five years, how much do you think you would have in the account if you left the money to grow?”

Only one-third of the U.S. population was able to answer these questions accurately.

“In finance, ignorance is not bliss,” Lusardi says.

Lusardi conducted a study on financial knowledge among young people in 2010, and she found that women were less likely to respond correctly to each of the “Big Three” questions that indicate financial literacy. The small group of young people who were deemed to be financially literate was disproportionately young males from college-educated families.

“If we don’t have financial literacy in schools, some groups will have a lot of difficulty in learning it,” Lusardi says, “because where are they going to learn it?”

To Haley Sacks, the answer to that question was Google. Sacks had just secured her first full-time job when she was asked how much she wanted to contribute to her 401(k). “I sort of faked that I understood it, and then I tried to learn about it and felt really underserved by the content that was available to me,” she said.

In doing research, she realized just how important these seemingly small decisions were to her financial future. So she asked herself the question: Why hasn’t anyone told me about this?

She began learning about it, and to hold herself accountable, she began making content about complicated topics in a way that she and her friends could grasp. Sacks started a YouTube channel called Mrs. Dow Jones where she uses pop culture to explain thorny financial concepts to an audience that doesn’t understand Wall Street jargon.

Sacks has used Taylor Swift’s career arc to explain stocks, the Kardashians to show the difference between a 401(k) and a Roth IRA, and The Bachelor to liken finding love on TV to investment banking.

Sacks, who has roughly 3,000 followers on YouTube and 120,000 on Instagram, says, “I want to help ease the transition for young people into adulthood and onwards for their own financial journey.”

Lately, Sacks has leaned heavier on the personal finance content, adding that she’s currently studying to become a certified financial planner so she can go a step further and give her followers actionable advice.

“With Gen Z, we’re going to see the biggest generation of entrepreneurs,” she says. “That means that all those people are going to have to learn how to pay themselves, manage their money, and pay their taxes. We just have to arm them with information.”

Katie Swanson, a mother of two, has become a full-blown celebrity on the platform for a hobby that’s been popular across generations: couponing. Known as “Coupon Katie,” Swanson has amassed 1.3 million followers on TikTok, and her coupon-clipping videos have received more than 36 million likes.

“A lot of people tell me that they thought couponing is something their moms or grandmothers did, but they never thought that they can actually supplement an income with it,” she said.

Swanson admits that TikTok is consumed largely for entertainment, so most of her videos are a mix of “silly and informative.” The line between education and entertainment can be a fine one, especially on a platform that only allows videos that last 60 seconds or less.

The quality of the content is precisely what researcher Lusardi worries about. “We have to be careful because you can lose a lot of the substance,” she says. “We cannot leave it to the people on TikTok to teach personal finance. This is a topic that belongs in school.”

Three tips for taking charge of your finances:

Figure out how much it costs to be you: “We all used to watch the show The Fabulous Life of…, and you learned how much it cost to be Beyoncé. You have to do that for yourself. Print out the last three months of your spending, and figure out how much it costs to be you. That will inform how big your emergency fund needs to be.” —Haley Sacks

2. Forgo instant gratification: “Short-term satisfaction is usually not worth the sacrifices you make long-term. Is buying that $200 Supreme shirt really worth it in the long run? My answer would probably be no. The majority of young people are too shortsighted. As a result, they might get themselves into credit card debt.” —Humphrey Yang

3. Invest in knowledge: “Knowledge is that essential ingredient that allows people to navigate all sorts of financial decisions. Finances are personal, so these very generic tips and suggestions sometimes do not apply to our very specific cases. We need to gain that basic knowledge because it really does pay high interest. If you’re a young person in school or college, get educated. Don’t miss that opportunity.” —Annamaria Lusardi

请打开财富Plus APP