“新银行”凭什么抢传统银行的生意?

去银行网点跟出纳员面对面交流的日子,可能已经一去不复返了。在选择把钱放在哪里这个问题上,许多美国人正在转变策略,纷纷拥抱“新银行”(neobank)。

根据金融科技平台United Fintech提供的数据,在美国和全球各地,新银行正在迅速兴起,尤其受到Z世代和千禧一代的青睐。仅仅一年内,在新银行开设主账户的客户比例就从4%飙涨到15%。

但新银行与普通银行究竟有何不同?消费者应该如何选择呢?让我们从基础知识讲起。

什么是新银行?

新银行是一种金融科技公司,通过在线或移动平台向客户提供支票或存款账户等银行服务。这些银行通常不像传统的“大银行”那样受到严格监管。与传统银行或纯网上银行不同,新银行往往不是真正意义上的银行,因此没有州或联邦监管机构颁发的银行牌照。相反,它们经常选择与一家已经接受监管的金融实体合作——唯有如此,新银行吸纳的存款才能够被美国联邦存款保险公司(FDIC)承保。

新银行最早出现在“大衰退”(Great Recession)的末期,旨在招揽那些可以从免费账户和理财服务(比如制定预算、追踪支出和自动储蓄)中受益的客户。从那以后,新银行不断发展壮大,许多颇受欢迎的品牌已经走进千家万户,例如Chime和Acorns。

“与传统银行相比,新银行致力于提供更大的价值和更好的体验。”Upgrade的联合创始人及首席执行官雷诺·拉普朗什说,“它们通过在线平台和手机应用程序为客户提供服务,从而不会承担分支网络和传统技术的运营成本。在此基础上,这些新型银行试图让消费者分享运营成本下降的好处,比如不收取账户费用,有时还给借记卡和信用卡用户提供更大的奖励。”

新银行与传统银行

新银行与传统银行的不同体现在几个关键方面。还应该指出的是,一些传统银行只提供在线服务,但我们不应该将其与新银行混为一谈。例如,Ally Bank是一家拥有特许全面牌照、只提供在线服务的银行,但人们并不认为它是一家新银行(我们将在下面讨论为什么这一点很重要)。

并非所有的新银行在产品和架构方面都完全相同,但它们与传统银行的不同通常体现在以下几点:

· 不像银行那样拥有州或联邦监管机构颁发的特许牌照。一家银行获得特许牌照,意味着它需要接受州或联邦特许章程的监管,要遵守一定的规章制度。特许银行必须向美国联邦存款保险公司投保,以保护客户的存款安全。

· 缺少实体网点。为了削减成本,并迎合那些尤为看重数字体验的消费者,新银行通常不设实体网点。更低的营业成本意味着新银行有能力提供费用更低,甚至免费的产品,以及更具竞争力的存款利率。

· 产品少。为了缓解风险并降低成本,新银行可能不会提供足以媲美大银行的产品品类。

· 绝佳的数字体验。新银行仅在为手机和在线用户量身定制的平台上运营。对于那些希望在线处理所有银行业务的消费者来说,这可能是一大福音。

· 必须与银行合作,才能够给客户存款投保。绝大多数的新银行本身并不像许多传统银行那样由美国联邦存款保险公司承保。如果新银行与一家业已经获得美国联邦存款保险公司承保的金融机构合作,它们就可以提供美国联邦存款保险公司承保的账户(保险金额最高达25万美元)。

新银行的利弊

新银行并不适合每一种消费者。考虑转投新银行之前,你首先应该了解一下它的优缺点。

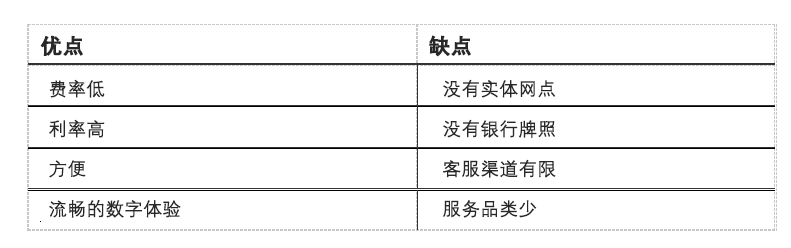

优点:新银行提供流畅的数字体验。与手机银行和网上银行类似,新银行能够在你的手机或电脑上提供更好的用户体验。“新银行的优点通常包括更好的使用体验。这种体验是通过数字原生流程提供的,而不像传统银行那样设法将模拟流程嵌入数字世界。”拉普朗什说。

优点:你可以受惠于较低的运营成本。新银行能够削减开设和维护实体网点的成本。由于省掉了这笔开支,它们往往可以降低服务费率,让广大客户享受实实在在的好处。“在越来越多的美国人面临财务压力之际,新银行不仅让消费者少支付了一笔银行费用,还增加了他们的存款。”君迪公司(J.D. Power)的银行和支付业务高级主管保罗·麦克亚当表示,“Chime和Cash App的增长尤为迅猛,其知名度和市场份额已经能够跟现有的直销银行Capital One、Ally和Discover相媲美。”

缺点:新银行提供的产品品类有限。“新银行从零开始打造自身产品,并不总是可以提供全方位的银行产品和服务,信贷产品尤为匮乏,尽管一些新银行确实在提供贷款和信用卡服务。”拉普朗什指出。

缺点:你可能很难联系到客服代表。亲自去一趟开户行,可能不是你的第一选择,但这总比听到电话那端说“您目前是等待服务热线的第64号客户”好得多。考虑在一家新银行开户前,务必要权衡一下你是否看重面对面的客服体验。

如何选择新银行

评估不同的新银行时,你需要考虑几个不同的因素来确定一个特定的新银行能否满足你的需求:

1. 评级和评论:访问你的手机应用程序商店,阅读用户对这款新银行应用程序的评论——毕竟,这可能会成为你办理银行业务的主要平台。

2. 提供的产品:新银行提供的产品可能仅限于一个标准的储蓄或支票账户,因为大多数的新银行都追求简洁。浏览这家新银行的网站,看看他们提供的产品是否满足你的需求,或者你是否应该另找一家产品更多的银行。

3. 利率和费用:你要根据开设账户的目的,研究每家银行的收费结构和现行利率,以确定哪家新银行能够帮助你达成目标。想增加你的存款,就选择一家提供有竞争力的高收益储蓄账户或存单的新银行。想利用手机应用程序来支付你的日常开支,不妨优先考虑一家提供免费支票账户的新银行。

4. 存款保险:并非所有的银行都是由美国联邦存款保险公司承保的,所以你需要核实这家新银行合作的传统银行是不是美国联邦存款保险公司的成员。美国联邦存款保险公司的BankFind Suite功能可以帮助你确定一家银行是否由美国联邦存款保险公司承保,或者你能够直接致电询问,以确定该行是不是美国联邦存款保险公司的成员。

5. 客服渠道:做一些调查,弄清楚每家新银行提供哪些类型的客户支持——比如聊天、电话、电子邮件或文本支持,以及它们的工作时间。考虑到你将来使用新银行时可能需要一些帮助,或者碰到一些跟账户相关的问题,所以你需要知道哪些客服渠道可以迅速帮助你排忧解难。

总结

在银行领域,新银行仍然是新生事物,但它们所采用的数字优先方式,正在引起许多消费者的共鸣。不过,在转投新银行的怀抱之前,你还是需要谨慎审查你打算使用的平台,看看它能否满足你办理银行业务的所有需求。这一点很重要。(财富中文网)

译者:任文科

去银行网点跟出纳员面对面交流的日子,可能已经一去不复返了。在选择把钱放在哪里这个问题上,许多美国人正在转变策略,纷纷拥抱“新银行”(neobank)。

根据金融科技平台United Fintech提供的数据,在美国和全球各地,新银行正在迅速兴起,尤其受到Z世代和千禧一代的青睐。仅仅一年内,在新银行开设主账户的客户比例就从4%飙涨到15%。

但新银行与普通银行究竟有何不同?消费者应该如何选择呢?让我们从基础知识讲起。

什么是新银行?

新银行是一种金融科技公司,通过在线或移动平台向客户提供支票或存款账户等银行服务。这些银行通常不像传统的“大银行”那样受到严格监管。与传统银行或纯网上银行不同,新银行往往不是真正意义上的银行,因此没有州或联邦监管机构颁发的银行牌照。相反,它们经常选择与一家已经接受监管的金融实体合作——唯有如此,新银行吸纳的存款才能够被美国联邦存款保险公司(FDIC)承保。

新银行最早出现在“大衰退”(Great Recession)的末期,旨在招揽那些可以从免费账户和理财服务(比如制定预算、追踪支出和自动储蓄)中受益的客户。从那以后,新银行不断发展壮大,许多颇受欢迎的品牌已经走进千家万户,例如Chime和Acorns。

“与传统银行相比,新银行致力于提供更大的价值和更好的体验。”Upgrade的联合创始人及首席执行官雷诺·拉普朗什说,“它们通过在线平台和手机应用程序为客户提供服务,从而不会承担分支网络和传统技术的运营成本。在此基础上,这些新型银行试图让消费者分享运营成本下降的好处,比如不收取账户费用,有时还给借记卡和信用卡用户提供更大的奖励。”

新银行与传统银行

新银行与传统银行的不同体现在几个关键方面。还应该指出的是,一些传统银行只提供在线服务,但我们不应该将其与新银行混为一谈。例如,Ally Bank是一家拥有特许全面牌照、只提供在线服务的银行,但人们并不认为它是一家新银行(我们将在下面讨论为什么这一点很重要)。

并非所有的新银行在产品和架构方面都完全相同,但它们与传统银行的不同通常体现在以下几点:

· 不像银行那样拥有州或联邦监管机构颁发的特许牌照。一家银行获得特许牌照,意味着它需要接受州或联邦特许章程的监管,要遵守一定的规章制度。特许银行必须向美国联邦存款保险公司投保,以保护客户的存款安全。

· 缺少实体网点。为了削减成本,并迎合那些尤为看重数字体验的消费者,新银行通常不设实体网点。更低的营业成本意味着新银行有能力提供费用更低,甚至免费的产品,以及更具竞争力的存款利率。

· 产品少。为了缓解风险并降低成本,新银行可能不会提供足以媲美大银行的产品品类。

· 绝佳的数字体验。新银行仅在为手机和在线用户量身定制的平台上运营。对于那些希望在线处理所有银行业务的消费者来说,这可能是一大福音。

· 必须与银行合作,才能够给客户存款投保。绝大多数的新银行本身并不像许多传统银行那样由美国联邦存款保险公司承保。如果新银行与一家业已经获得美国联邦存款保险公司承保的金融机构合作,它们就可以提供美国联邦存款保险公司承保的账户(保险金额最高达25万美元)。

新银行的利弊

新银行并不适合每一种消费者。考虑转投新银行之前,你首先应该了解一下它的优缺点。

优点:新银行提供流畅的数字体验。与手机银行和网上银行类似,新银行能够在你的手机或电脑上提供更好的用户体验。“新银行的优点通常包括更好的使用体验。这种体验是通过数字原生流程提供的,而不像传统银行那样设法将模拟流程嵌入数字世界。”拉普朗什说。

优点:你可以受惠于较低的运营成本。新银行能够削减开设和维护实体网点的成本。由于省掉了这笔开支,它们往往可以降低服务费率,让广大客户享受实实在在的好处。“在越来越多的美国人面临财务压力之际,新银行不仅让消费者少支付了一笔银行费用,还增加了他们的存款。”君迪公司(J.D. Power)的银行和支付业务高级主管保罗·麦克亚当表示,“Chime和Cash App的增长尤为迅猛,其知名度和市场份额已经能够跟现有的直销银行Capital One、Ally和Discover相媲美。”

缺点:新银行提供的产品品类有限。“新银行从零开始打造自身产品,并不总是可以提供全方位的银行产品和服务,信贷产品尤为匮乏,尽管一些新银行确实在提供贷款和信用卡服务。”拉普朗什指出。

缺点:你可能很难联系到客服代表。亲自去一趟开户行,可能不是你的第一选择,但这总比听到电话那端说“您目前是等待服务热线的第64号客户”好得多。考虑在一家新银行开户前,务必要权衡一下你是否看重面对面的客服体验。

如何选择新银行

评估不同的新银行时,你需要考虑几个不同的因素来确定一个特定的新银行能否满足你的需求:

1. 评级和评论:访问你的手机应用程序商店,阅读用户对这款新银行应用程序的评论——毕竟,这可能会成为你办理银行业务的主要平台。

2. 提供的产品:新银行提供的产品可能仅限于一个标准的储蓄或支票账户,因为大多数的新银行都追求简洁。浏览这家新银行的网站,看看他们提供的产品是否满足你的需求,或者你是否应该另找一家产品更多的银行。

3. 利率和费用:你要根据开设账户的目的,研究每家银行的收费结构和现行利率,以确定哪家新银行能够帮助你达成目标。想增加你的存款,就选择一家提供有竞争力的高收益储蓄账户或存单的新银行。想利用手机应用程序来支付你的日常开支,不妨优先考虑一家提供免费支票账户的新银行。

4. 存款保险:并非所有的银行都是由美国联邦存款保险公司承保的,所以你需要核实这家新银行合作的传统银行是不是美国联邦存款保险公司的成员。美国联邦存款保险公司的BankFind Suite功能可以帮助你确定一家银行是否由美国联邦存款保险公司承保,或者你能够直接致电询问,以确定该行是不是美国联邦存款保险公司的成员。

5. 客服渠道:做一些调查,弄清楚每家新银行提供哪些类型的客户支持——比如聊天、电话、电子邮件或文本支持,以及它们的工作时间。考虑到你将来使用新银行时可能需要一些帮助,或者碰到一些跟账户相关的问题,所以你需要知道哪些客服渠道可以迅速帮助你排忧解难。

总结

在银行领域,新银行仍然是新生事物,但它们所采用的数字优先方式,正在引起许多消费者的共鸣。不过,在转投新银行的怀抱之前,你还是需要谨慎审查你打算使用的平台,看看它能否满足你办理银行业务的所有需求。这一点很重要。(财富中文网)

译者:任文科

The days of visiting your bank’s local branch and interacting with a teller face-to-face may be behind us. When it comes to choosing where to put their money, many Americans are switching gears and opting for neobanks.

In the U.S. and across the globe, neobanks are quickly gaining traction, especially among Gen Zers and millennials, according to United Fintech. Within one year, the percentage of these customers with a primary account at a neobank grew from 4% to 15%.

But how are neobanks different from regular banks? And how do you choose one? Let’s start with the basics.

What is a neobank?

A neobank is a fintech company that offers banking services like checking or deposit accounts to its clients through online or mobile platforms. These banks are not typically regulated in the same way traditional “megabanks” are. Unlike traditional banks or online-only banks, neobanks are often not banks and therefore do not have a bank charter with state or federal regulators. Instead, they often partner with an already regulated entity so that their deposits will be insured by the FDIC.

Neobanks first came to the forefront during the tail end of the Great Recession in hopes of appealing to customers who could stand to benefit from fee-free accounts and financial management services such as budgeting, spend tracking, and automated savings. Since then, neobanks have grown and many popular options like Chime or Acorns have become household names.

“Neobanks generally aim at providing more value and a better experience than traditional banks,” says Renaud Laplanche, cofounder and CEO of Upgrade. “They serve their customers online and through a mobile app and therefore do not incur the cost of a branch network and legacy technology, and strive to pass on these lower costs to consumers by charging no account fees and sometimes offering greater rewards on debit and credit cards.”

Neobanks vs. traditional banks

Neobanks differ from traditional banks and online banks in a few key ways. It should also be noted that some traditional banks are online-only, but these should not be confused with neobanks. For example, Ally Bank is a fully chartered online-only bank—but it isn’t considered a neobank (we’ll get into why that matters below).

While not all neobanks are identical in their offerings or structure, they typically differ from traditional banks in that they:

· Aren’t chartered with state or federal regulators like banks. When a bank is chartered, it’s governed by a state or national charter and is expected to adhere to certain rules and regulations. Chartered banks must have FDIC insurance to protect customers’ deposits.

· Lack physical branches. As a way to cut costs and cater to the digital-first consumer, neobanks don’t usually have physical locations. Lower overhead costs mean that neobanks have the ability to offer lower or no-fee products and more competitive rates.

· May offer fewer products. As a way to mitigate risk and reduce costs, neobanks may not offer the same range of products as big banks.

· Have a digital-first interface. Because neobanks operate solely on mobile and online platforms, their platforms are tailor-made for mobile and online usage. This could be a major benefit for the consumer who prefers to do all of their banking virtually.

· Must be partnered with a bank to insure customer deposits. The vast majority of neobanks are not FDIC-insured on their own in the way that many traditional banks are. Neobanks can offer FDIC-insured accounts (insured up to $250,000) if they have a partnership with an already FDIC-insured institution.

Pros and cons of neobanks

Neobanks are not for every kind of consumer. They come with their own set of pros and cons that you should be aware of before switching to a neobank.

Pro: Neobanks offer a smooth digital experience. Similar to mobile- and online-only banks, neobanks may offer a better user experience on your phone or computer. “The pros generally include a better user experience, through digitally native processes rather than analog processes that the traditional banks attempt to retrofit to a digital world,” says Laplanche.

Pro: You may benefit from lower costs. Neobanks are able to cut the cost of opening and maintaining physical locations, and as a result they often pass on those savings in the form of lower costs and fees for customers. “At a time when an increasing portion of U.S. consumers are experiencing financial stress, neobanks have helped consumers reduce banking fees and grow their money,” says Paul McAdam, senior director of banking and payments at J.D. Power. “Chime and Cash App, in particular, have grown rapidly, with awareness and market share rivaling that of incumbent direct banks Capital One, Ally, and Discover.”

Con: You may be limited when it comes to product offerings. “Neobanks build their products from the ground up and do not always offer the full range of banking products and services,” says Laplanche. “Credit products in particular are not always available, although some neobanks do offer loans and credit cards.”

Con: You might have a hard time getting ahold of a customer service representative. While physically going to your bank’s location may not be your first resort, it certainly beats being caller #64 in a customer service queue. Before considering a neobank, weigh whether or not having a face-to-face customer service option is important to you.

How to choose a neobank

When you’re evaluating different neobanks, you’ll want to consider a few different factors to determine if a specific neobank will meet your needs:

1. Ratings and review: Visit your phone’s app store to read reviews on your neobank’s app (which may be the primary platform you’ll use for your banking needs).

2. Product offerings: Your product options may be limited to a standard savings or checking account because most neobanks keep it simple. Explore the bank’s site to figure out if the products they offer will meet your needs or if you should keep digging for a bank that has more to offer.

3. Interest rates and fees: Depending on the purpose of your account, you’ll want to research each bank’s fee structure and current interest rates to determine which neobank will help you meet your goals. If the objective is to boost your savings, opt for a neobank that offers a competitive rate on a high-yield savings account or CD. If the goal is to use this neobank for your everyday expenses, choosing a neobank that offers a no-fee checking account may be more of a priority.

4. Deposit insurance: Not all banks are FDIC-insured, so you’ll want to verify that the bank your neobank is partnered with is a member of the FDIC. The FDIC’s BankFind Suite can help you determine if a bank is FDIC-insured, or you can contact the FDIC by phone to verify that that particular bank is a member.

5. Customer support channels: Do some digging to figure out what kinds of customer support options each neobank offers—like chat, phone, email, or text support, and what their hours are. In case you find yourself in a situation where you need some assistance or have questions related to your account, you’ll want to know what your options are for resolving those issues quickly.

The takeaway

Neobanks are still the new kid on the block when it comes to banking, but their digital-first approach is resonating with many consumers. Still, it’s important to properly vet the platform you plan to use to ensure that it meets all of your banking needs.