美国楼市意外出现回暖迹象

美联储(Federal Reserve)应对通货膨胀的策略很简单。它的基本策略是:持续加息,直到整个经济中的企业和消费者支出减少,通胀回落。

从历史上来看,美联储应对通胀的策略,对美国房地产市场造成了严重冲击。在房地产交易中,月供是关键。美联储着手应对通胀之后,抵押贷款利率随之骤升,导致新贷款人的月供大幅增加。这也解释了为何今年春季抵押贷款利率上涨之后,房地产市场迅速降温。

但由此导致的房地产市场调整可能很快失去动力。

上周,抵押贷款利率快速下降。截至周二,平均30年期固定抵押贷款利率为5.05%,从6月的最高点6.28%有显著下降。抵押贷款利率下降让持币观望的购房者舒了一口气。如果贷款人在6月以6.28%的利率抵押贷款500,000美元,月供本息为3,088美元。如果按5.05%的利率贷款,月供只有2,699美元。在30年贷款期限内可节省140,000美元。

到底发生了什么?随着疲软的经济数据陆续公布,金融市场开始将2023年的经济衰退考虑在内。这给抵押贷款利率带来了下行压力。

穆迪分析(Moody’s Analytics)首席经济学家马克·扎蒂对《财富》杂志表示:“债券市场考虑到明年有较高概率发生经济衰退,而经济下行会迫使美联储改变方向,并降低联邦基金利率。”

虽然美联储并不直接确定抵押贷款利率,但其政策确实会影响金融市场如何确定10年期国债收益率和抵押贷款利率。如果预计联邦基金利率上调且货币政策收紧,金融市场会推高10年期国债收益率和抵押贷款利率。如果预计联邦基金利率下调且货币政策放宽,金融市场会降低10年期国债收益率和抵押贷款利率。目前金融市场出现的正是后一种情况。

今年早些时候,随着抵押贷款利率大幅提高,有数以千万计的美国人失去了抵押贷款资格。然而,随着抵押贷款利率开始下滑,有数百万美国人又有机会申请抵押贷款。因此,许多房地产业从业者对抵押贷款利率下降欢欣鼓舞:利率下降将有助于增加购房业务。

抵押贷款利率下降毫无疑问会刺激更多观望者购房,但不要认为房地产回调已经结束。

经济学博客Calculated Risk的作者比尔·麦克布赖德在周二的一篇通讯稿中写道:“归根结底,最近的抵押贷款利率下降会有少许帮助,但5%的抵押贷款利率意味着房地产市场依旧面临压力(销量减少,房价上涨放缓)。”为什么呢?即使抵押贷款利率下降一个百分点,房地产的可负担性依旧为史上最低。

麦克布赖德写道:“如果我们将房价上涨考虑在内,同一套住房的月供同比上涨了超过50%。”

之所以说看好房地产市场的人过于乐观,还有另外一个原因:如果对经济衰退的担忧(正在帮助降低抵押贷款利率)是正确的,可能导致房地产行业更加疲软。如果人们担心失业,他们就不会进入房地产市场。

扎蒂告诉《财富》杂志:“虽然利率下降本身确实是房地产市场的利好消息,但如果同时出现了经济衰退和失业率快速上升,利率下降无法产生积极效果。”

未来抵押贷款利率将如何变化?

美国银行(Bank of America)的研究人员认为,未来12个月,10年期国债收益率可能从2.7%下降至2.0%。这可能导致抵押贷款利率下降至4%至4.5%。(抵押贷款利率的变化趋势与10年期国债收益率的变化趋势密切相关。)

但有一个重要的未知因素:美联储。

美联储显然希望放缓房地产市场的增长速度。疫情期间的房地产市场繁荣是导致通胀高企的原因之一。在此期间,房价上涨了42%,房屋建设量创16年新高。房屋销量下降和房屋建设量减少,应该能缓解美国严重紧张的房屋供应。我们已经看到住房开工率下降,正在减少对框架木材、橱柜、窗户等材料的需求。

但如果抵押贷款利率下降过快,房地产市场反弹,可能干扰美联储应对通胀的努力。如果出现这种情况,美联储拥有足够多的货币“武器”,再次给抵押贷款利率带来上行压力。

明尼阿波利斯联邦储备银行(Federal Reserve Bank of Minneapolis)主席尼尔·卡什卡利周日对CBS表示:“无论我们从技术上是否陷入经济衰退,并不会改变我的分析结果。我关注的是通胀数据……到目前为止,通货膨胀继续升高,令我们感到意外。我们致力于降低通胀,并将为此竭尽所能。”(财富中文网)

译者:刘进龙

审校:汪皓

美联储(Federal Reserve)应对通货膨胀的策略很简单。它的基本策略是:持续加息,直到整个经济中的企业和消费者支出减少,通胀回落。

从历史上来看,美联储应对通胀的策略,对美国房地产市场造成了严重冲击。在房地产交易中,月供是关键。美联储着手应对通胀之后,抵押贷款利率随之骤升,导致新贷款人的月供大幅增加。这也解释了为何今年春季抵押贷款利率上涨之后,房地产市场迅速降温。

但由此导致的房地产市场调整可能很快失去动力。

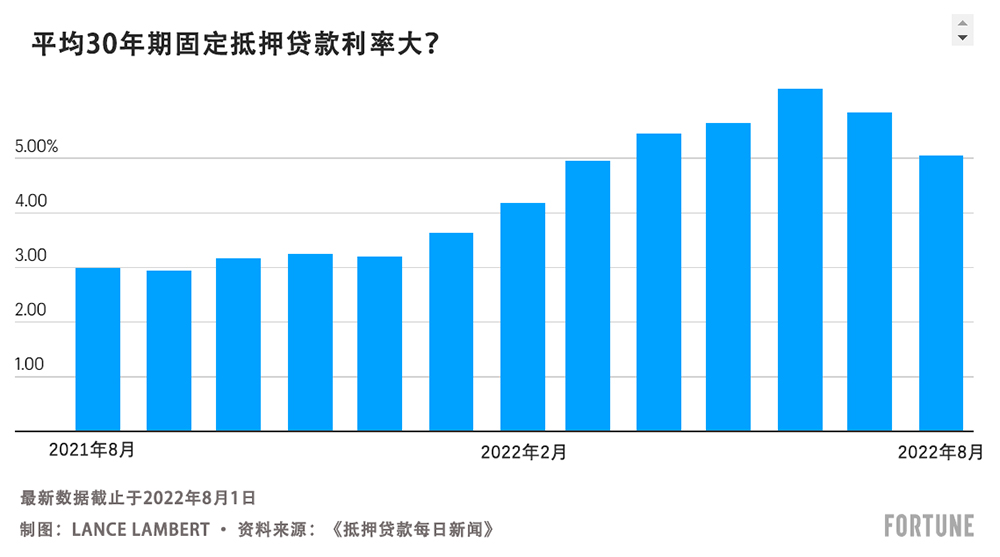

上周,抵押贷款利率快速下降。截至周二,平均30年期固定抵押贷款利率为5.05%,从6月的最高点6.28%有显著下降。抵押贷款利率下降让持币观望的购房者舒了一口气。如果贷款人在6月以6.28%的利率抵押贷款500,000美元,月供本息为3,088美元。如果按5.05%的利率贷款,月供只有2,699美元。在30年贷款期限内可节省140,000美元。

到底发生了什么?随着疲软的经济数据陆续公布,金融市场开始将2023年的经济衰退考虑在内。这给抵押贷款利率带来了下行压力。

穆迪分析(Moody’s Analytics)首席经济学家马克·扎蒂对《财富》杂志表示:“债券市场考虑到明年有较高概率发生经济衰退,而经济下行会迫使美联储改变方向,并降低联邦基金利率。”

虽然美联储并不直接确定抵押贷款利率,但其政策确实会影响金融市场如何确定10年期国债收益率和抵押贷款利率。如果预计联邦基金利率上调且货币政策收紧,金融市场会推高10年期国债收益率和抵押贷款利率。如果预计联邦基金利率下调且货币政策放宽,金融市场会降低10年期国债收益率和抵押贷款利率。目前金融市场出现的正是后一种情况。

平均30年期固定抵押贷款利率

2021年8月

2022年2月

2022年8月

最新数据截止于2022年8月1日

制图:LANCE LAMBERT · 资料来源:《抵押贷款每日新闻》

今年早些时候,随着抵押贷款利率大幅提高,有数以千万计的美国人失去了抵押贷款资格。然而,随着抵押贷款利率开始下滑,有数百万美国人又有机会申请抵押贷款。因此,许多房地产业从业者对抵押贷款利率下降欢欣鼓舞:利率下降将有助于增加购房业务。

抵押贷款利率下降毫无疑问会刺激更多观望者购房,但不要认为房地产回调已经结束。

经济学博客Calculated Risk的作者比尔·麦克布赖德在周二的一篇通讯稿中写道:“归根结底,最近的抵押贷款利率下降会有少许帮助,但5%的抵押贷款利率意味着房地产市场依旧面临压力(销量减少,房价上涨放缓)。”为什么呢?即使抵押贷款利率下降一个百分点,房地产的可负担性依旧为史上最低。

麦克布赖德写道:“如果我们将房价上涨考虑在内,同一套住房的月供同比上涨了超过50%。”

之所以说看好房地产市场的人过于乐观,还有另外一个原因:如果对经济衰退的担忧(正在帮助降低抵押贷款利率)是正确的,可能导致房地产行业更加疲软。如果人们担心失业,他们就不会进入房地产市场。

扎蒂告诉《财富》杂志:“虽然利率下降本身确实是房地产市场的利好消息,但如果同时出现了经济衰退和失业率快速上升,利率下降无法产生积极效果。”

首次抵押贷款500,000美元的本息月供金额

过去两个月,平均30年期固定抵押贷款利率从6.28%下降到5.05%

2021年8月

2022年2月

2022年8月

制图:LANCE LAMBERT · 资料来源:《财富》杂志使用《抵押贷款每日新闻》的抵押贷款数据计算的结果

未来抵押贷款利率将如何变化?

美国银行(Bank of America)的研究人员认为,未来12个月,10年期国债收益率可能从2.7%下降至2.0%。这可能导致抵押贷款利率下降至4%至4.5%。(抵押贷款利率的变化趋势与10年期国债收益率的变化趋势密切相关。)

但有一个重要的未知因素:美联储。

美联储显然希望放缓房地产市场的增长速度。疫情期间的房地产市场繁荣是导致通胀高企的原因之一。在此期间,房价上涨了42%,房屋建设量创16年新高。房屋销量下降和房屋建设量减少,应该能缓解美国严重紧张的房屋供应。我们已经看到住房开工率下降,正在减少对框架木材、橱柜、窗户等材料的需求。

但如果抵押贷款利率下降过快,房地产市场反弹,可能干扰美联储应对通胀的努力。如果出现这种情况,美联储拥有足够多的货币“武器”,再次给抵押贷款利率带来上行压力。

明尼阿波利斯联邦储备银行(Federal Reserve Bank of Minneapolis)主席尼尔·卡什卡利周日对CBS表示:“无论我们从技术上是否陷入经济衰退,并不会改变我的分析结果。我关注的是通胀数据……到目前为止,通货膨胀继续升高,令我们感到意外。我们致力于降低通胀,并将为此竭尽所能。”(财富中文网)

译者:刘进龙

审校:汪皓

The Federal Reserve has a simple inflation-fighting playbook. It goes like this: Keep applying upward pressure on interest rates until business and consumer spending across the economy weakens and inflation recedes.

Historically speaking, the Fed’s inflation-fighting playbook always delivers a particularly hard hit to the U.S. housing market. When it comes to housing transactions, monthly payments are everything. And when mortgage rates spike—which happens as soon as the Fed goes after inflation—those payments spike for new borrowers. That explains why as soon as mortgage rates rose this spring, the housing market slipped into a housing cool down.

But that housing correction could soon lose some steam.

Over the past week, mortgage rates have declined fast. As of Tuesday, the average 30-year fixed mortgage rate sits at 5.05%, down from June, when mortgage rates peaked at 6.28%. Those falling mortgage rates give sidelined homebuyers immediate relief. If a borrower in June took out a $500,000 mortgage at a 6.28% rate, they’d pay $3,088 monthly in principal and interest. At a 5.05% rate, that payment would be just $2,699. Over the course of the 30-year loan that’s a savings of $140,000.

What’s going on? As weakening economic data rolls in, financial markets are pricing in a 2023 recession. That’s putting downward pressure on mortgage rates.

“The bond market is pricing in a high probability of a recession next year, and that the downturn will prompt the Fed to reverse course and cut [Federal Funds] rates,” Mark Zandi, chief economist at Moody’s Analytics, tells Fortune.

While the Fed doesn’t directly set mortgage rates, its policies do impact how financial markets price both the 10-year Treasury yield and mortgage rates. In expectation of a rising Federal Funds rate and monetary tightening, financial markets increase both the 10-year Treasury yield and mortgage rates. In expectation of a reduced Federal Funds rate and monetary easing, financial markets price down both the 10-year Treasury yield and mortgage rates. The latter is what we’re seeing now in financial markets.

The average 30-year fixed mortgage rate

AUG ’21

FEB ’22

AUG ’22

LATEST READING IS FROM AUGUST 1, 2022

CHART: LANCE LAMBERT · SOURCE: MORTGAGE NEWS DAILY

As mortgage rates spiked earlier this year, tens of millions of Americans lost their mortgage eligibility. However, as mortgage rates begin to slide, millions of Americans are regaining access to mortgages. That's why so many real estate professionals are cheering on lower mortgage rates: They should help to increase homebuying activity.

While lower mortgage rates will undoubtedly prompt more sideline buyers return to open houses, don't pencil in the end of the housing correction just yet.

"The bottom line is the recent decline in mortgage rates will help at the margin, but the housing market will remain under pressure with mortgage rates at 5% (fewer sales, slowing house price growth)," wrote Bill McBride, author of the economics blog Calculated Risk, in his Tuesday newsletter. The reason? Even with the one-percentage-point drop in mortgage rates, housing affordability remains historically low.

"If we include the increase in house prices, payments are up more than 50% year over year on the same home," writes McBride.

There's another reason housing bulls shouldn't get too overconfident: If recession fears—which are helping to drive mortgage rates lower—are correct, it would cause some additional weakening in the sector. If someone is afraid of losing their job, they're not going to jump into the housing market.

"While lower rates by themselves are a positive for housing, that isn’t the case when accompanied by a recession and quickly rising unemployment," Zandi tells Fortune.

The monthly principal and interest payment on a new $500,000 mortgage

The average 30-year fixed mortgage rate has fallen from 6.28% to 5.05% over the past two months

AUG ’21

FEB ’22

AUG ’22

CHART: LANCE LAMBERT · SOURCE: CALCULATION BY FORTUNE, USING MORTGAGE DATA FROM MORTGAGE NEWS DAILY

Where will mortgage rates head from here?

Researchers at Bank of America believe there's a chance that the 10-year Treasury yield could slip from 2.7 to 2.0% over the coming 12 months. That could make mortgage rates fall to between 4% and 4.5%. (The trajectory of mortgage rates correlates closely with the trajectory of the 10-year Treasury yield.)

But there's a big wild card: the Federal Reserve.

The Fed clearly wants to slow the housing market. The pandemic housing boom—during which home prices soared 42% and homebuilding hit a 16-year high—has been among the drivers of sky-high inflation. Reduced home sales and a decline in homebuilding should provide relief for the overstressed U.S. supply of housing. We're already seeing it: Plummeting housing starts is translating into reduced demand for everything from framing lumber to cabinets to windows.

But if mortgage rates fall too quickly, a rebounding housing market could mess up the Fed's inflation fight. If that happens, the Fed has more than enough monetary "firepower" to once again put upward pressure on mortgage rates.

“Whether we are technically in a recession or not doesn’t change my analysis. I’m focused on the inflation data...And so far, inflation continues to surprise us to the upside," Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, told CBS on Sunday. "We are committed to bringing inflation down, and we're going to do what we need to do."